- Guangdong Huize Metal Trading Co., Ltd. cordially invites you to the 2026SMM (16th) Tin Industry Chain Conference.

"Tin" Guiding the Future: Industrial Transformation and Value Reshaping in a New Cycle Conference Background Currently, the global tin industry stands at a historic turning point. Traditional cyclical logic has been completely disrupted, and strategic value has become fully prominent. The tin market in 2026 presents unprecedented complexity and profound changes: I. Deep Restructuring of Supply-Demand Patterns, Unprecedented Strategic Significance The global static reserve-to-production ratio for tin resources is only 14 years, making scarcity increasingly evident. The supply side faces "triple pressures": recurring delays in production resumptions in Myanmar, persistently tightening policies in Indonesia, and elevated geopolitical risks in the DRC. Resource constraints have become a new normal. Meanwhile, the demand structure is undergoing a fundamental shift, as tin has become a strategic resource connecting traditional manufacturing with a digital future. II. Price Levels Breaking Historical Records, Industrial Ecosystem Facing Reshaping In early 2026, SHFE tin prices exceeded 470,000 yuan/mt, reaching an all-time high. This price breakthrough not only reflects supply-demand imbalances but also signals a revaluation of the tin industry's worth. Traditional trading models, risk management systems, and supply chain collaboration methods are all in urgent need of innovation and breakthroughs. III. Technology-Driven and Green Transformation Fostering a New Symbiotic Ecosystem Digital and intelligent technologies are deeply empowering the tin industry chain. The global green transition demands that the tin industry upgrade toward low-carbon operations and a circular economy. Recycled tin recovery and green smelting processes have become essential paths. All segments of the industry chain must shift from competition to collaboration, building an open, resilient, and innovative symbiotic system. Against this backdrop, the 2026 SMM (16th) Tin Industry Chain Conference will convene global industry elites for joint discussions on August 19-21, 2026, in Changsha, Hunan. Guangdong Huize Metals Trading Co., Ltd. will attend this grand event, joining industry peers in exploring development trends and jointly propelling the tin industry to new heights. Click the registration form to sign up now and witness and participate in this momentous, far-reaching industry gathering, co-creating a brilliant new chapter! Guangdong Huize Metals Trading Co., Ltd., located in Guangzhou—the core hub of the Guangdong-Hong Kong-Macao Greater Bay Area—is a specialized trader focused on tin ingot trade. Since its establishment, the company has deeply cultivated the tin sector, based in South China while serving the entire nation, committed to providing upstream and downstream clients with high-quality, efficient, stable, and compliant metal trading and supply chain supporting services. We have established long-term, stable partnerships with numerous renowned smelters, tin ingot producers, and traders nationwide, forming a strong partner network and serving as a premium supplier to multiple state-owned enterprises and well-known companies. The company is also a member of the Tin Branch of the China Nonferrous Metals Industry Association (CNIA) and a member of the Electronic Tin Solder Materials Branch of the China Electronic Materials Industry Association. Our company has always adhered to the principles of people-orientation, integrity, pragmatism, and innovation, and is willing to achieve mutual benefits and win-win outcomes with partners and clients across the upstream and downstream sectors of the tin industry chain. Contact Information Xie Zhichao: 13197537999 Wang Yongfu: 18889929433 Address: Room 1601, No. 4, Huitong Third Street, Nansha District, Guangzhou Long press or scan the code to register now 2026 SMM (16th) Tin Industry Chain Conference

Jul 3, 2026 11:30 - Ganzhou Qianshun New Materials Co., Ltd. looks forward to seeing you at the SMM (16th) Tin Industry Chain Conference 2026

"Tin" Leads the Future: Industrial Transformation and Value Reshaping in a New Cycle Conference Background Currently, the global tin industry is at a historic turning point. Traditional cyclical logic has been completely overturned, and its strategic value is fully highlighted. In 2026, the tin market is exhibiting an unprecedentedly complex pattern and profound transformation: 1. Deep Restructuring of Supply-Demand Pattern, Unprecedented Enhancement of Strategic Attributes. The static reserve-production ratio of global tin ore resources is only 14 years, and its scarcity is becoming increasingly pronounced. The supply side faces "triple pressures": repeated reversals in Myanmar's production resumption process, continually tightening policies in Indonesia, and elevated geopolitical risks in the DRC. Resource constraints have become the new normal. At the same time, the demand structure has undergone a fundamental shift. Tin has become a strategic resource bridging traditional manufacturing and the digital future. 2. Price System Breaks Historical Records, Industry Ecosystem Faces Reshaping. In early 2026, SHFE tin prices broke through 470,000 yuan/mt, hitting a record high. This price breakthrough is not only a manifestation of supply-demand imbalance but also a sign of the reassessment of the tin industry's value. Traditional trade models, risk management systems, and supply chain collaboration approaches all urgently need innovative breakthroughs. 3. Technology-Driven and Green Transition Giving Rise to a New Symbiotic Ecosystem. Digital and intelligent technologies are deeply empowering the tin industry chain. The global green transition requires the tin industry to upgrade toward low-carbon and circular economy development. Recycled tin recovery and green smelting processes have become the path forward. Every link in the industry chain must shift from competition to collaboration and build an open, resilient, and innovative symbiotic system. Against this backdrop, August 19-21, 2026 in Changsha, Hunan held 2026 SMM (16th) Tin Industry Chain Conference will gather global industry elites for in-depth discussions. Ganzhou Qianshun New Materials Co., Ltd. will attend this grand event, discuss industry development trends with industry peers, and jointly push the tin industry to new heights. Click to register now and join the conference, witness and participate in this significant and far-reaching industry event, and create a brilliant new chapter together! Ganzhou Qianshun New Materials Co., Ltd. was established in 2018, primarily engaged in the processing and sales of tungsten-tin associated ores, tantalum-niobium associated ores, and other polymetallic complex ores. Contact Information Huang Shaoxin 13617078696 Huang Shaoming 15270620268 Huang Qili 15297821623 Long press to scan the QR code and register now 2026 SMM (16th) Tin Industry Chain Conference

Jul 3, 2026 10:42 - Gejiu Yunxin Nonferrous Electrolysis Co., Ltd. looks forward to meeting you at the 2026 SMM (16th) Tin Industry Chain Conference

"Tin" Leads the Future: Industrial Transformation and Value Reshaping in the New Cycle Conference Background Currently, the global tin industry stands at a historic turning point. Traditional cyclical logic has been completely disrupted, and its strategic value is being fully highlighted. In 2026, the tin market is presenting an unprecedentedly complex pattern and profound transformation: I. Deep Restructuring of Supply-Demand Patterns with Unprecedented Strategic Importance The global static reserve-to-production ratio for tin resources stands at only 14 years, underscoring growing scarcity. The supply side faces "triple pressure": repeated setbacks in Myanmar’s production resumptions, persistently tightening policies in Indonesia, and high geopolitical risks in the DRC—resource constraints have become the new normal. Meanwhile, the demand structure is undergoing a fundamental shift, with tin now a strategic resource bridging traditional manufacturing and the digital future. II. Price Systems Breaking Historical Records and the Industrial Ecosystem Facing Reshaping In early 2026, SHFE tin prices surpassed 470,000 yuan/mt, reaching an all-time high. This price breakthrough not only reflects supply-demand imbalances but also signals a revaluation of the tin industry. Traditional trading models, risk management systems, and supply chain collaboration methods all urgently require innovative breakthroughs. III. Technology-Driven and Green Transition Foster a New Symbiotic Ecosystem Digital and intelligent technologies are deeply empowering the tin industry chain, while the global green transition demands a shift toward low-carbon practices and a circular economy. Recycled tin recovery and green smelting processes have become essential paths. All segments of the industry chain must move from competition to collaboration, building an open, resilient, and innovative symbiotic system. Against this backdrop, August 19-21, 2026, in Changsha, Hunan, the 2026 SMM (16th) Tin Industry Chain Conference will bring together global industry elites for in-depth discussions. Gejiu Yunxin Nonferrous Electrolysis Co., Ltd. will attend this grand event, engaging with industry peers to explore development trends and jointly propel the tin industry to new heights. Click the registration form to sign up now and join us in witnessing and participating in this landmark, far-reaching industry gathering. Together, let us create a brilliant new chapter! Founded in 2005, Gejiu Yunxin Nonferrous Electrolysis Co., Ltd. is located in Huogudu, Zhadian Town, Gejiu City, Honghe Prefecture, Yunnan Province. With a registered capital of 150 million yuan and over 450 employees, its business scope covers nonferrous metal tin smelting, processing, and sales. The company is equipped with electric furnace crude smelting, bimetallic electrolytic wet process, vacuum furnace, and electric heating continuous melting crystallizer pyrometallurgy refining tin processes, with an annual refined tin (Sn99.95%) production capacity of 6,000 mt. Its "Yunxiang" brand tin ingot is a delivery brand on the Shanghai Futures Exchange. The company holds 46 patents and has been honored with titles such as “National Demonstration Base for Employment of Persons with Disabilities,” “Yunnan Province Specialized, Sophisticated, Distinctive, and Innovative Enterprise,” “Yunnan Province High-Tech Enterprise,” “Yunnan Province Innovative Enterprise,” and “Gejiu City Top 50 Enterprise.” Its corporate bank credit rating is AAA, and it is designated as a price submitter for tin ingot prices by SMM and the International Tin Association. The company ranks among the top ten enterprises in China’s tin smelting industry, with high product recognition, strong social credibility, and significant market share. Established in 2005 and located in Huogudu, Zadian Town, Gejiu City, Honghe Prefecture, Yunnan Province, Gejiu Yunxin Nonferrous Electrolysis Co., Ltd. boasts a registered capital of RMB 150 million and has over 450 employees. The company specializes in the smelting, processing, and sales of nonferrous metal tin. Its production facilities include electric furnace smelting, bimetallic electrolysis hydrometallurgical processes, vacuum furnaces, and electrothermal continuous melting and crystallization machines for pyrometallurgical refining of tin. With an annual production capacity of 6,000 mt of refined tin (Sn99.95%), the company’s "Yunxiang" brand tin ingots are listed as a deliverable brand on the Shanghai Futures Exchange. Gejiu Yunxin holds 46 patents and has been recognized with numerous honors, including the "National Demonstration Base for Employment of Persons with Disabilities," "Yunnan Province Specialized, Sophisticated, Distinctive, and Innovative Enterprise," "Yunnan Province High-Tech Enterprise," "Yunnan Province Innovative Enterprise," and "Gejiu City Top 50 Enterprise." Its corporate bank credit rating is AAA, and it is designated as a price submitter for tin ingot prices by SMM and the International Tin Association. The company ranks among the top ten enterprises in the domestic tin smelting industry, with high product recognition, strong social credibility, and significant market share. Contact Shen Yongji 18608779826 Long press to scan and register now 2026 SMM (16th) Tin Industry Chain Conference

Jul 2, 2026 11:28 - Beijing Redec Pneumatic Conveying Technology Co., Ltd. Looks Forward to Your Participation in the 2026 SMM (16th) Tin Industry Chain Conference

"Tin" Leading the Future: Industry Transformation and Value Reshaping in the New Cycle – Meeting Background: Currently, the global tin industry is at a historic turning point, with traditional cycle logic completely shattered and strategic value comprehensively highlighted. The tin market in 2026 presents an unprecedented complex pattern and profound changes: 1. Deep Restructuring of Supply-Demand Pattern, Unprecedented Enhancement of Strategic Attributes The global static reserve-production ratio of tin resources stands at only 14 years, highlighting increasingly prominent scarcity. The supply side faces "triple pressures": repeated production resumptions in Myanmar, continuously tightening policies in Indonesia, and high geopolitical risks in the DRC. Resource constraints have become the new normal. Meanwhile, the demand structure is undergoing a fundamental shift, and tin has become a strategic resource connecting traditional manufacturing with the digital future. 2. Price System Breaks Through History, Industry Ecosystem Faces Reshaping In early 2026, SHFE tin prices surpassed 470,000 yuan/mt, setting a new record high. This price breakthrough reflects not only the supply-demand imbalance but also marks a revaluation of the tin industry's value. Traditional trading models, risk management systems, and supply chain collaboration methods are in urgent need of innovative breakthroughs. 3. Technology-Driven and Green Transition Fosters a Symbiotic New Ecosystem Digital and intelligent technologies are deeply empowering the tin industry chain. The global green transition requires the tin industry to upgrade towards low-carbon and circular economy practices, with recycled tin recovery and green smelting processes becoming essential pathways. All segments of the industry chain must move from competition to collaboration, building an open, resilient, and innovative symbiotic system. Against this backdrop, August 19-21, 2026 in Changsha, Hunan the 2026 SMM (16th) Tin Industry Chain Conference will gather global industry elites for in-depth discussions. Beijing Ruidike Pneumatic Conveying Technology Co., Ltd. will attend this grand event, joining industry peers in exploring industry development trends and jointly promoting the tin industry to new heights. Click to register now and join us in witnessing and participating in this extraordinary and far-reaching industry event, together creating a brilliant new chapter! Ruidike focuses on R&D, production, installation, and after-sales service for solid material pneumatic conveying and injection systems. Its products are applied in industries such as steel, non-ferrous metals, coal chemicals, petrochemicals, food, new energy, and lime kilns. The company is recognized as a National / Zhongguancun High-Tech Enterprise, a Specialized and Sophisticated Enterprise, and an Integration of Informatization and Industrialization Enterprise. It has been awarded titles such as Henan Green Factory, Intelligent Workshop, and Service-Oriented Manufacturing Enterprise, and won provincial-level scientific and technological achievement awards in both 2023 and 2025. In 2018, it established a wholly-owned subsidiary, Henan Ruidike, which specializes in intelligent production and remote operation and maintenance of core components, and houses technical platforms including a powder comprehensive experiment facility, detection center, and digital exhibition hall. It is a provincial-level big data benchmark unit and owns a provincial-level engineering technology research center for gas conveying and injection. Our pulverized coal injection equipment for fuming furnaces, side-blown furnaces, etc., serves numerous leading non-ferrous smelting enterprises including CNGR, Huayou, Jinchuan Group, and Shengtun, with hundreds of complete sets of projects successfully delivered. We sincerely invite clients in and outside China to visit us for field trips and cooperation, for mutual benefit and win-win development! REDC integrates R&D, manufacturing and full lifecycle service of solid material pneumatic conveying & injection systems, serving steel, non-ferrous metals, new energy and other industries. As a national & Zhongguancun high-tech, SRUI enterprise, we hold multiple provincial honors and won major sci-tech awards in 2023 & 2025. Our subsidiary delivers intelligent core parts and remote O&M. We run a provincial-level engineering research center and complete powder testing & R&D platforms, recognized as a Henan big data benchmark. Our coal injection equipment for fuming/side-blown furnaces has hundreds of successful projects with top metallurgical clients including CNGR, Huayou and Jinchuan Group. Welcome global partners for win-win cooperation! Contact Information Address: 8th Floor, Building A2, Zhongguancun No.1, Fengxiu East Road, Yongfeng Industrial Park, Haidian District, Beijing Contact: Mao Qingyang 13811750062 WeChat QR Code Douyin QR Code Long press and scan to register now 2026 SMM (16th) Tin Industry Chain Conference

Jul 2, 2026 11:13 - Greentech Technology International Limited invites you to the 2026 SMM (16th) Tin Industry Chain Conference

"Tin" Leads the Future: Industrial Transformation and Value Reconstruction in a New Cycle Conference Background Currently, the global tin industry stands at a historic turning point, where traditional cyclical logic has been completely shattered and strategic value has become fully prominent. The tin market in 2026 exhibits an unprecedentedly complex landscape and profound changes: I. Profound Reconstruction of Supply-Demand Patterns, Unprecedented Enhancement of Strategic Attributes The global static reserve-to-production ratio of tin resources is only 14 years, with scarcity increasingly evident. The supply side faces "triple pressures": repeated setbacks in Myanmar’s production resumptions, continuously tightening policies in Indonesia, and high geopolitical risks in the DRC, making resource constraints a new normal. Meanwhile, the demand structure has undergone a fundamental shift, and tin has become a strategic resource bridging traditional manufacturing and the digital future. II. Price System Breaks Historical Records, Industry Ecosystem Faces Restructuring In early 2026, SHFE tin price exceeded 470,000 yuan/mt, reaching an all-time high. This price breakthrough is not only a manifestation of supply-demand imbalance but also a marker of the revaluation of the tin industry. Traditional trade models, risk management systems, and supply chain collaboration methods all urgently require innovative breakthroughs. III. Technology-Driven and Green Transition Fostering a New Symbiotic Ecosystem Digital and intelligent technologies are deeply empowering the tin industry chain. The global green transition demands that the tin industry upgrade toward low-carbon and circular economy, with recycled tin recovery and green smelting processes becoming necessary paths. Every link in the industry chain must shift from competition to collaboration, building an open, resilient, and innovative symbiotic system. Against this backdrop, from August 19 to 21, 2026 in Changsha, Hunan the 2026 SMM (16th) Tin Industry Chain Conference will gather global industry elites for in-depth discussions. Greentech Technology International Limited will attend this grand event, discussing industry development trends with peers and jointly promoting the tin industry to new heights. Click to register now, witness and participate in this significant and far-reaching industry event, and together create a brilliant new chapter! Greentech Technology International Limited ("Greentech Technology", stock code: 00195) is a company listed on The Stock Exchange of Hong Kong Limited. On March 4, 2011, the company successfully acquired all equity interests in Baisong Mineral Resources Global Limited ("Baisong Mineral"), becoming a non-ferrous metal resources enterprise primarily engaged in tin ore mining and sales. Since the sale of its insulation materials business on February 29, 2011, the company has focused on the development of non-ferrous metal businesses. Greentech Technology International Limited is listed on The Stock Exchange of Hong Kong Limited. On 4 March 2011, the Company successfully acquired the entire interests of Parksong Mining and Resource Recycling Limited, thereby venturing into the min. Parksong Mining is an investment holding company that conducts tin mining in Tasmania, Australia, through a joint venture, holding a 50% interest in the Renison Mine, the Mount Bischoff open-cut tin project, and the Rentails tailings retreatment project. Among these, the Renison Mine has long been one of the world's major hard-rock tin mines and is also Australia's largest tin-producing mine. Our project partner, Yunnan Tin Group (Holding) Co., Ltd., is China's largest tin producer. With its extensive industry experience, Yunnan Tin Group provides strong support in the sale of tin and the production management of the Tasmania tin mines. Parksong Mining is an investment holding company which launches tin mining through a joint venture in Tasmania, Australia. It holds a 50% interest of the Renison quarry, the Mount Bischoff open cut tin project and the Rentails tailings retreatment project. The Renison tin deposit has always been one of the largest hard rock tin deposits in the world and the largest tin mine in Australia. Our project partner, Yunnan Tin Group (Holding) Co., Ltd., is the largest tin producer in China. With its extensive tin mining experience, Yunnan Tin Group will provide potent support to our metal tin sale and the production management of the Tasmania mines. Upon the acquisition of the tin mine, the company also strengthened its management and technical teams. With the addition of new management, it assembled a group of experts with unique achievements in geological exploration, mining, mineral processing, and smelting, and recruited a number of professionally trained and experienced engineering and technical personnel from Australia and mainland China to enhance frontline production management. The company believes that the experienced management team can provide valuable advice for its future development in the non-ferrous metals industry, helping to lay a solid foundation for long-term growth and seize industry opportunities as they arise. Along the acquisition of the tin mine, our management and technical teams have also been strengthened. In addition to the joining of new management members, the company was set up as a congregation of professionals with unique contributions in geological exploration, mining, processing, smelting and refining. A batch of technical staff with expertise and practical experience has also been recruited from Australia and mainland China to enhance the management of front-line production. The Company believes that an experienced management team can provide valuable advice on its future development in the non-ferrous metal industry, and will be conducive to building a strong foundation for long-term development and to grasping industrial opportunities. Greentech possesses high-quality and promising projects, strong resource advantages, advanced tin mining technology, and an experienced management team. The Company will focus on the non-ferrous metal industry, seize market opportunities, accelerate its development pace, strive to enhance corporate value, achieve steady growth in revenue and profit, and maximize shareholder returns. Greentech has high quality and promising projects, strong resource advantages, advanced tin mining technologies and an experienced management team. Focusing on the non-ferrous metal industry, the Company will seize business opportunities, step up the pace of development and enhance the value of the Company so as to realize stable growths in revenues and profits and maximize returns to shareholders. Contact Yao Huixing +86 13077486850 Liu Yidi +86 16621280621 Long Press to Scan and Register Now 2026 SMM (16th) Tin Industry Chain Conference

Jun 30, 2026 16:43 - Hyundai Motor Achieves RE100 Across All Sites in Europe, North America and India

Hyundai Motor published its 2026 Sustainability Report on June 30, outlining its proactive risk management capabilities and future sustainability management strategy amid tightening global ESG regulations. In the report, Hyundai Motor said it has achieved RE100, or 100% renewable energy use, across all of its business sites in Europe, North America and India.

Jun 30, 2026 16:11 - Rio Tinto Reportedly in Talks with Vitol on Freight and Logistics Joint Venture

Rio Tinto is reportedly in early-stage discussions with commodity trading giant Vitol regarding the formation of a freight and logistics joint venture. According to market sources, the talks include potential cooperation in freight management and freight risk management tools, although the structure and scope of any agreement have yet to be finalized. The discussions reflect Rio Tinto's ongoing efforts to strengthen supply chain efficiency and improve value creation across its commodity portfolio, including copper. The move follows the company's broader strategy of streamlining operations and enhancing commercial capabilities after ending acquisition talks with Glencore earlier this year.

Jun 29, 2026 09:55 - Guangdong Hanhe Nonferrous Metals Co., Ltd. invites you to meet at 2026SMM (16th) Tin Industry Chain Conference.

“Tin” Leads the Future: Industrial Transformation and Value Reshaping in the New Cycle Conference Background At present, the global tin industry is standing at a historic turning point. Traditional cyclical logic has been completely disrupted, and tin’s strategic value has become fully evident. In 2026, the tin market is exhibiting an unprecedentedly complex landscape and profound changes: I. Deep Restructuring of the Supply-Demand Pattern, with Strategic Attributes Reaching an Unprecedented Level The global tin resource static reserve-to-production ratio is only 14 years, and scarcity is becoming increasingly prominent. The supply side is facing “triple pressure”: repeated setbacks in Myanmar’s production resumptions, continued tightening of policies in Indonesia, and elevated geopolitical risks in the DRC—resource constraints have become the new normal. Meanwhile, the demand structure has undergone a fundamental shift, and tin has become a strategic resource linking traditional manufacturing with the digital future. II. The Price System Breaks Through History, and the Industry Ecosystem Faces Reshaping In early 2026, SHFE tin prices broke through 470,000 yuan/mt, reaching a record high. This price breakthrough is not only a reflection of the supply-demand imbalance, but also a sign of value reassessment in the tin industry. Traditional trading models, risk management systems, and supply chain collaboration approaches are all in urgent need of innovative breakthroughs. III. Technology-Driven and Green Transformation Gives Rise to a New Symbiotic Ecosystem Digital and intelligent technologies are deeply empowering the tin industry chain. The global green transition requires the tin industry to upgrade toward low-carbonisation and a circular economy; recycled tin recovery and green smelting processes have become the only way forward. All links of the industry chain must shift from competition to collaboration, building an open, resilient, and innovative symbiotic system. Against this backdrop, on August 19-21, 2026 , held in Changsha, Hunan , the 2026 SMM (16th) Tin Industry Chain Conference will bring together global industry elites for joint discussions. Guangdong Hanhe Nonferrous Metals Co., Ltd. will attend this grand event, joining industry peers to discuss industry development trends and working together to drive the tin industry to new heights. Click the to register for attendance immediately, and jointly witness and participate in this extraordinary and far-reaching industry event, creating a brilliant new chapter together! Guangdong Hanhe Nonferrous Metals Co., Ltd. was established in 2015 and is located in Chaozhou, a port city on the eastern coast of Guangdong Province. It is a smelting and processing enterprise mainly engaged in the production of refined tin. The company is a professional manufacturer of metal tin smelting, recycling, and production, primarily engaged in the recycling and reuse of secondary tin materials, and producing and selling tin ingots that exceed national standards. Our company has always adhered to the mindset of “a sincere heart, treating others with sincerity” in communication and cooperation with clients. With the overarching goals of “innovation,” “environmental protection,” “sincerity,” and “satisfaction,” we continue to innovate and pursue change, contributing our efforts to environmental protection. Adhering to the "circular economy" business philosophy of "limited resources, unlimited circulation", with Guangdong as the base, we have branched out across the globe, treating waste tin materials produced by business units worldwide with the most professional technology, recycling and reusing them, allowing recycled resources to share the output of raw ore, reducing excessive dependence on the Earth's primary resources, and leaving a better future for the next generation. Founded in 2015, Guangdong Hanhe Nonferrous Metals Co., Ltd. is located in Chaozhou, a port city on the eastern coast of Guangdong Province. It is a smelting and processing enterprise mainly producing tin and tin-lead solder. The company is a professional metal tin smelting and recycling manufacturer, mainly engaged in the recycling and reuse of tin secondary materials, producing and selling tin ingots that superior to national standards. Our company has always adhered to the mentality of "pure heart, sincere attitude" to communicate and cooperate with customers. With the big goal of "innovation", "environmental protection", "sincere" and "satisfaction", we will continue to innovate and change, and do our best for environmental protection. Adhering to the "circular economy" business philosophy --"limited resources and unlimited circulation", take Guangdong province as the base, we will open the branches to the rest of the world, and treat the waste tin materials produced by the institutions around the world with the most professional technology. Recycling and reusing, making recycling resources to share the output of raw ore, and reducing the excessive dependence on the earth's natural resources, leaving a better future to the next generation . Contact Information Chen Xiaojie 15919540000 15919555555 Press and hold to scan to register now 2026 SMM (16th) Tin Industry Chain Conference

Jun 25, 2026 16:06 - Baowu Magnesium's business includes magnesium materials and magnesium-aluminum products, etc. Its Anhui Qingyang mine project has reached a capacity of 20 million mt per year.

Asked "Dear Board Secretary, I would like to inquire whether your company, as found online, can stably mass-produce semiconductor-grade ultra-high-purity magnesium metal ingots and is the only publicly listed firm for such products. Also, what has been the sales proportion of such products in the company's total sales in recent years?" Baowu Magnesium Industry responded on the investor interaction platform on June 23: The company's businesses include magnesium material business, magnesium products business, aluminum products business, mineral products business, and building formwork business. Its main products include magnesium alloys, magnesium alloy deep-processed products, aluminum alloys, aluminum alloy deep-processed products, master alloys, and strontium metal. For the revenue breakdown by product, please refer to the 2025 annual report. The company has not publicly disclosed information regarding the specific products and sales proportions you mentioned. Please refer to the company's officially released periodic reports or announcements for such information. Regarding the question "1. What is the commissioning progress of the mine in the Qingyang project in Anhui, and what is the current ore output? 2. What advantages does the company's vertical retort magnesium smelting technology have? How does it compare with peers in Fugu?" Baowu Magnesium Industry responded on June 17 on the investor interaction platform: The company adopts vertical retort magnesium smelting technology, which features outstanding technical advantages: increased single-retort capacity, shortened production cycle, improved production efficiency, extended service life of reduction retorts, and a higher level of mechanized and automated operations. The Anhui Qingyang mine project has reached a capacity of 20 million mt per year . On June 3, during a survey, Baowu Magnesium Industry stated that the company already has a certain level of technology reserves in magnesium-based hydrogen storage, but the development of the hydrogen storage industry mainly relies on downstream application expansion, which takes time. Currently, downstream application expansion is slow: the hydrogen energy industry chain (production/storage/transportation/utilization) lacks overall maturity, and orders have yet to materialize at scale. On June 3, during a survey, Baowu Magnesium Industry stated that in terms of end-use breakdown, the largest use of magnesium is in magnesium alloys, accounting for about 49%; followed by addition to aluminum alloys, about 26%; steel desulfurization, about 12%; as a metal reducing agent, about 8%; and other fields, about 5%. On June 3, during a survey, Baowu Magnesium Industry stated that the company's magnesium ingot production costs have the following advantages: 1. The company has a complete industry chain advantage, especially in stable raw material supply. 2. The company continues to increase investment in original magnesium smelting technology, enhancing the cost competitiveness of its primary magnesium through large-scale vertical retort magnesium smelting technology and energy efficiency optimization. Baowu Magnesium Industry announced on May 26 that it recently received a notice from its controlling shareholder, Baosteel Metal Co., Ltd., that 263 million shares (26.53% of total shares) will be transferred at no cost to China Baowu Steel Group Corporation Limited. After the transfer, the controlling shareholder will change to China Baowu, while the actual controller remains the State-owned Assets Supervision and Administration Commission of the State Council, unchanged. The announcement shows Baosteel Metal is a wholly owned subsidiary of China Baowu. Before this transfer, China Baowu indirectly held 26.53% of Baowu Magnesium through Baosteel Metal, being the indirect controlling shareholder. After the transfer, China Baowu will directly hold 26.53% and become the controlling shareholder. Performance: Baowu Magnesium Industry disclosed its 2025 annual report on April 29, showing: In 2025, the company achieved revenue of 9,911,752,817.29 yuan, up 10.34% YoY, and net profit attributable to shareholders of the publicly listed firm was 18,548,946.85 yuan, down 111.62% YoY. The decline was mainly due to the continued downward trend of magnesium prices, which caused a significant YoY decline in the magnesium material business profit; meanwhile, the joint venture Anhui Baomei Light Alloy Co., Ltd. is in the ramp-up stage of a new project, with low production and high costs, plus low magnesium prices, which dragged down the company's investment income YoY. Regarding the main business activities during the reporting period, Baowu Magnesium Industry introduced in its 2025 annual report: The company is a leader in magnesium-based new materials under China Baowu, with advantages across the entire industry chain and mine resources, leading vertical retort magnesium smelting technology, and its magnesium alloy capacity and market share are among the global frontrunners. The company focuses on lightweight materials, with products covering automotive, consumer electronics, e-bikes, building formwork, etc. After more than 30 years of development, the company has become a high-tech enterprise integrating mining, non-ferrous metal smelting, and processing, aiming to be a global leader in the magnesium industry. Its businesses include magnesium material business, magnesium products business, aluminum products business, mineral products business, and building formwork business. Its main products include magnesium alloys, magnesium alloy deep-processed products, aluminum alloys, aluminum alloy deep-processed products, master alloys, and strontium metal. Outlook on future development: Baowu Magnesium Industry stated in the 2025 annual report: 2026 marks the start of the company's 15th Five-Year Plan, and the industry will see an important period of high-end and large-scale development. The board will guide management with the core positioning of "building a lightweight solutions provider and becoming the new materials main force of China Baowu," focusing on the main business, deepening cultivation, advancing full-industry-chain upgrading, technological innovation, market expansion, and green development, to achieve sustained improvement in operating performance and significant enhancement of core competitiveness. 1. Strengthen strategic guidance and solidify the foundation for new quality productive forces in the magnesium industry. Accelerate building a full industry chain from primary magnesium to alloys, deep processing, and terminal applications, concentrate on breakthroughs in green smelting and stable, low-cost production technologies, and speed up large-scale promotion of key products. 2. Coordinate the construction of key projects to synergistically improve overall operational efficiency. Speed up construction and comprehensive acceptance of the Huayuan Wujia mine in the Qingyang project, orderly advance main plant construction and production indicator optimization, and steadily push forward key projects in Gansu Baomei, Wutai Baomei, and Chaohu Baomei. 3. Deepen magnesium industry reform and innovation, promoting modern corporate governance. Steadily advance business transformation and renewal, promote asset integration, and further optimize governance, management control, and business management models. 4. Accelerate intelligent development layout and fully advance IT system construction. Complete full implementation of the Baowu standard financial system and rollout of cost systems in subsidiaries, create a full-process IT model project for magnesium business, further enhance operational control, cost calculation, compliant operations, and risk prevention and control capabilities. 5. Focus on attack on primary magnesium cost to continuously enhance market competitiveness. Reduce manufacturing costs of three core components: reduction retorts, center pipes, and cones; optimize steel grades to extend retort service life; reduce auxiliary energy consumption and material-to-magnesium ratio. 6. Implement cost-conscious management and systematically build a high-quality development business model. Deepen overall benchmarking to identify and address gaps, systematically attack the "four major costs" — primary magnesium, energy, logistics, and quality — and improve the operational control system. 7. Strengthen safety and environmental protection fortresses, systematically elevate green development. Continuously strengthen safety and environmental compliance rectification. Highlight risk management in key areas and enhance intrinsic safety. Accelerate green factory and low-carbon capability building. 8. Main risk factors and countermeasures (1) Risk of fluctuating main raw material prices The company's main business is magnesium and aluminum alloys and deep processing, with primary raw materials being magnesium and aluminum metals. Prices are affected by supply-demand dynamics, global and Chinese economic conditions, and closely tied to automotive lightweighting progress, 3C industry demand, etc. If magnesium and aluminum prices swing wildly in the future, it will affect cost control and profitability. The company is raising the self-sufficiency ratio of raw materials, adjusting product mix, and increasing the proportion of deep-processed products to mitigate the impact. (2) Risk of fluctuating market demand The company's magnesium and aluminum lightweight alloy products are mainly used in automotive and consumer electronics. Currently, seizing auto lightweighting opportunities, the company is expanding into downstream deep processing such as magnesium alloy automotive die castings, magnesium alloy building formwork, and aluminum extrusion products. The pace of automotive lightweighting and 3C electronics demand are influenced by macro-economy, industrial policies, and process technology innovation. If downstream demand falls short of expectations, it will affect operating performance. The company is expanding product applications in various fields, increasing penetration rates, to reduce the risk of demand fluctuations. In addition, the Q1 2026 report released by Baowu Magnesium Industry shows: In Q1 2026, revenue was 2.132 billion yuan, up 4.86% YoY; net profit attributable to shareholders of the publicly listed firm was 5.0891 million yuan, down 81.94% YoY. Regarding the increase in Q1 revenue, Baowu Magnesium Industry explained: Sales of main products and material prices rose YoY. For the decline in net profit, the company said it was due to a decrease in product gross margins and increased losses from joint ventures. Baowu Magnesium Industry mentioned that its magnesium alloy capacity and market share rank among global leaders. Looking back at the performance of SMM magnesium alloy AZ91D in Q1 this year: The average price on March 31, 2026 was 19,650 yuan/mt, compared with 17,950 yuan/mt on December 31, 2025, the average price rose by 1,700 yuan/mt in Q1, or 9.47%. The daily average price in Q1 2026 was 18,932.14 yuan/mt, up 1,320.74 yuan/mt, or 7.5% YoY, from 17,611.4 yuan/mt in Q1 2025. According to SMM price quotes: The EXW price of SMM magnesium alloy AZ91D on June 24 ranged from 18,250 to 18,350 yuan/mt, with an average of 18,300 yuan/mt, down 0.54% from the previous trading day. Currently, magnesium alloy prices are in the doldrums alongside magnesium ingot prices, with overall low trading sentiment. Fundamentals side: Supply side, magnesium alloy smelters have stable operating rates, ample spot supply in the market, and overall supply is loose; demand side, downstream die-casting plants show significant divergence in orders, with stable automotive orders, persistently sluggish two-wheeler orders, and alloy processing fees in the doldrums. Overall, the magnesium alloy market maintains a supply-strong-demand-weak pattern, with prices expected to remain in a weak consolidation phase in the short term.

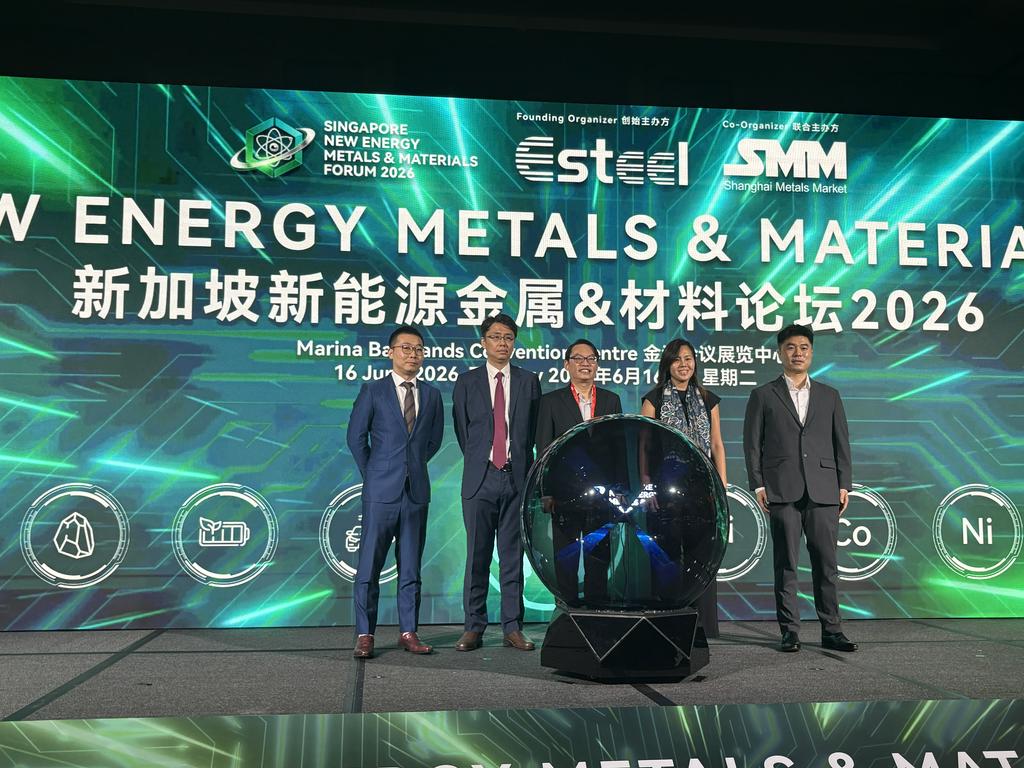

Jun 24, 2026 11:03  SMM CEO Attends Opening Ceremony of Singapore International Ferrous Week 2026

SMM CEO Attends Opening Ceremony of Singapore International Ferrous Week 2026The Singapore International Ferrous Week (SIFW) 2026 officially kicked off on June 16, 2026. Logan Lu, CEO of Shanghai Metals Market (SMM), attended the opening ceremony as a distinguished guest. Co-hosted by SGX and Green Esteel with support from Enterprise Singapore, the event runs from June 15 to June 19. Its core summit, Singapore Iron & Steel Conference, attracted over 350+ participants including miners and steel mills from Australia, Southeast Asia, Japan and South Korea, serving as Southeast Asia’s flagship ferrous industry exchange platform. SGX CEO Loh Boon Chye delivered a keynote, highlighting trends in iron ore pricing mechanisms and financialization. He noted that physical trade evolution calls for diversified, differentiated pricing benchmarks to streamline risk management. Iron ore has grown into a mainstream investable commodity, included in major global indices; SGX has partnered with SummerHaven to launch tradable iron ore products. Leveraging strengths in physical trade, shipping, financing and risk hedging, Singapore acts as a neutral global commodity hub, the core rationale behind SIFW. Singapore’s Minister of Trade and Industry Alvin Tan likened geopolitical and economic headwinds to kryptonite weighing on the sector, yet underscored steel’s strong resilience. He outlined four growth pillars: tapping robust Asian steel demand led by Southeast Asia and India; utilizing Singapore’s full industrial and financial ecosystem for supply chain and price risk management; advancing AI and digitalization to boost operational efficiency; and accelerating low-carbon steel and maritime decarbonization amid tightening global carbon regulations. The Singapore New Energy Metals & Materials Forum , co-organized by Green Esteel and SMM , was launched alongside this event with the goal to advance low-carbon metal collaboration. Satvinder Singh, Deputy Secretary General of the ASEAN Economic Community, delivered the opening remarks for the forum, focusing on the industry resilience of the global ferrous metals sector amid multiple challenges and echoing the four development strategy recommendations mentioned above: deepening engagement in Asia, basing in Singapore, technology enablement, and green transformation. He also highlighted Singapore’s positioning as a commodities trading hub, as well as local supporting measures for industrial digitalization and the low-carbon transition. On the same day, Logan Lu arranged two important opening events. At 10:30 a.m., he also attended the opening of the inaugural Singapore New Energy Metals & Materials Forum, co-hosted by Green Esteel and SMM, and engaged in in-depth exchanges with enterprises across the industry chain in and outside China on core topics such as ferrous metals, the global supply chain layout for new energy metals, and the industry’s green and low-carbon transformation. The Singapore New Energy Metals & Materials Forum represents a strategic extension into the fast-growing track of new energy metals and new materials. The forum adopts an integrated “Forum + Exhibition” model, bringing together global industry leaders, policy researchers, investment institutions, traders, and technology R&D and manufacturing producers to jointly assess the industry’s future development direction. As the global energy transition continues to accelerate, new energy metals and high-end new materials are a critical foundation for the low-carbon economy and the development of renewable energy. Coupled with multiple variables such as changes in the geopolitical environment, the restructuring of critical minerals supply chains, and adjustments to the global trade system, the industry is facing new opportunities and challenges. Centered on six major themes—global macro economy, supply and demand for critical metals, industry chain integration, supply chain resilience, industry investment, and breakthroughs in new materials technologies—the forum promotes global resource matching and strategic cooperation across the new energy metals industry chain through keynote speeches, panel discussions, business matchmaking, and industry exhibitions, thereby driving the industry’s sustainable development.

Jun 18, 2026 10:29