86results found for 'rare metal'

Sort by : |

- Ultra Rare Metals Acquires Full Ownership of PCH Rare Earth Project in Brazil

[SMM Rare Earth News] US-based Ultra Rare Metals recently completed full ownership of the PCH rare earth project in Goiás State, Brazil. Through a share swap agreement, Ultra Rare Metals increased its previously held 50% stake to 100%. Upon completion of the transaction, former Canadian partner Appia Rare Earths & Uranium Corp. will hold 25% equity in Ultra Rare Metals. The PCH project covers a total area of 42,932.2 hectares, encompassing two mineralization systems: hard rock carbonatite and ionic adsorption clay (IAC).

Jun 4, 2026 18:12 - Guangdong Jinhaoyu Environmental Protection Technology Co., Ltd. Invites You to the 2026 SMM (7th) Silver Industry Chain Innovation Conference

Against the backdrop of global energy transition and the accelerating development of the digital economy, silver—a strategic metal with both industrial and financial attributes—is seeing its industry chain undergo profound transformation. On one hand, demand for silver from emerging sectors such as PV, NEVs, and 5G communications continues to climb, driving the industry toward higher value-added and greener development. On the other hand, resource constraints, technological barriers, and market fluctuations impose higher demands on industry chain resilience, urgently requiring innovation-driven coordinated development across the entire chain. Dual Drivers of Policy and Market Under China's "dual carbon" goals and the global ESG investment wave, the silver industry faces pressing needs for green production, recycling, and low-carbon technologies. The NDRC's "14th Five-Year Plan for Circular Economy Development" explicitly calls for strengthening the recycling of precious metal resources, while international silver price fluctuations and geopolitical risks are compelling enterprises to enhance supply chain autonomy and controllability. Against this backdrop, the Silver Industry Chain Innovation Conference has emerged, aiming to build a collaborative platform integrating government, industry, academia, research, and end-use applications, to address industry pain points and lead the industry toward high-end, intelligent, and internationalized development. Innovation Needs and Industry Pain Points Technological Breakthroughs: Silver purification processes, nano-silver material applications, and scrap recovery technologies urgently need breakthroughs to meet the demand for high-purity, low-cost silver in emerging fields such as PV silver paste and flexible electronics. Industry Chain Coordination: Information barriers exist across mining, smelting and processing, and end-use application segments, requiring digital tools to achieve optimized resource allocation and risk sharing. Green Transformation: Traditional smelting processes are energy-intensive and highly polluting, necessitating the promotion of clean production technologies and circular economy models in response to global carbon neutrality commitments. Market Expansion: Silver's application potential in frontier fields such as hydrogen energy and quantum computing has yet to be fully explored, requiring strengthened cross-industry collaboration and standard-setting. Conference Objectives and Value Themed "Silver Chain Innovation · Intelligent Creation for the Future," this conference brings together global silver industry chain leaders, research institutions, financial institutions, and policymakers for in-depth dialogue on three core topics: technological R&D, supply chain optimization, and market expansion. Through the release of an industry white paper, the establishment of an innovation alliance, and the signing of major projects, the conference will drive the silver industry's transformation from "resource dependence" to "technology leadership," providing critical material support for the global energy revolution and digital economy. Guangdong Jinhaoyu Environmental Protection Technology Co., Ltd. will attend this grand event, joining industry peers to discuss industry development trends and work together to propel the silver industry to new heights. Click to register now, and together witness and participate in this extraordinary and far-reaching industry event, co-creating a brilliant new chapter! Guangdong Jinhaoyu Environmental Protection Technology Co., Ltd. is located in Nanshui Town, Gaolan Port, Jinwan District, Zhuhai City. Holding hazardous waste treatment qualifications in Guangdong Province, it is a technology-oriented environmental protection enterprise integrating R&D, production, and sales, specializing in comprehensive utilization of resources. The company possesses mature precious metal and rare metal recovery and disposal processes along with a professional technical team, capable of professionally recovering and deeply refining metals such as gold, silver, palladium, platinum, rhodium, and ruthenium from industrial scrap and wastewater, achieving harmless disposal of hazardous waste and resource recycling. Main Business 1. Hazardous Waste Disposal: Collection, storage, treatment, and comprehensive utilization of hazardous waste resources. 2. Finished Product Sales: A series of products including potassium gold cyanide, palladium chloride, palladium sulphuric acid, palladium sponge, platinum-group materials, gold ingots, silver ingots, copper powder, composite sheets & plates, etc. 3. Procurement Needs: Various types of precious metal-bearing scrap R&D and Innovation The company has a professional R&D laboratory, equipped with high-end equipment and a technical team, focusing on R&D in new materials, environmental protection technologies, and information technology. It continuously carries out technological breakthroughs, talent cultivation, and achievement transformation, empowering industrial upgrading through technological innovation. The enterprise adheres to the development philosophy of technological innovation and continuous improvement, encouraging all employees to refine and optimize based on their positions, maintaining industry leadership with stable and reliable technical capabilities. Meanwhile, the company actively deploys R&D in artificial intelligence deep learning technologies, delving into image recognition algorithm optimization and model building, empowering the enterprise's intelligent and high-quality development with cutting-edge technologies. Contact Information Sales Hotline: 13318942131 (Product Consultation, Order Cooperation) Procurement Hotline: 13923491869/18566557880 (Precious Metal-bearing Scrap Procurement) Long Press to Scan and Register Now 2026 SMM (7th) Silver Industry Chain Innovation Conference

May 26, 2026 14:50 - Policy Tailwinds Combined with Rising Expectations of Improving Demand, Rare Earth Permanent Magnets Concept Strengthened, Xiangdian Co. Hit Daily Limit [SMM Express]

SMM May 22 update: The "Regulations for the Implementation of the Mineral Resources Law of the People's Republic of China" was recently promulgated and will take effect from June 15, 2026. The tight supply situation on the raw material side remained unchanged. Pr-Nd oxide saw a notable increase on May 21, boosted by major manufacturers' procurement, but underwent a slight correction on May 22 under the influence of inquiries pushing for lower prices. Nevertheless, the recovery in market confidence provided some support for Pr-Nd prices. Demand side, the NEV, wind power, and humanoid robot industries continued to develop favorably, and the market expected promising growth in high performance NdFeB demand. Additionally, after the previous period of adjustment, some market funds flowed back into the rare earth permanent magnet sector, driving a notable rise in the rare earth permanent magnet concept on May 22. As of the close on May 22, the rare earth permanent magnet concept rose 3.14%. In terms of individual stocks: Xiangtan Electric Manufacturing hit the daily limit, while Advanced Technology & Materials, Hanghua Co., Huaxin Technology, Innuovo Technology, and Orient Zirconic Industry led the gains. News [Li Qiang Signs State Council Decree Promulgating the "Regulations for the Implementation of the Mineral Resources Law of the People's Republic of China"] Premier Li Qiang recently signed a State Council decree promulgating the "Regulations for the Implementation of the Mineral Resources Law of the People's Republic of China" (hereinafter referred to as the "Regulations"), which will take effect from June 15, 2026. The Regulations aim to ensure the effective implementation of the revised Mineral Resources Law, promote the rational development and utilization of mineral resources, strengthen the protection of mineral resources and the ecological environment, drive high-quality development of the mining industry, and safeguard mineral resource security. The Regulations consist of 8 chapters and 79 articles, mainly covering the following contents. First, further improving the mining rights system, with specific provisions on the establishment, transfer by tender, renewal, and assignment of mining rights. Second, refining systems related to mineral resource exploration and extraction, including establishing and improving technical standards and normative systems for basic geological surveys, clarifying procedures for applying for exploration permits and mining permits, strengthening land use guarantees for mining, promoting comprehensive utilization of mineral resources, and clarifying the legal effect of mineral resource reserve reports. Third, refining systems related to ecological restoration in mining areas, clarifying that mining right holders are responsible for ecological restoration in mining areas, detailing the contents that ecological restoration plans for mining areas should specify, and stipulating the completion deadlines and acceptance procedures for ecological restoration in mining areas. Fourth, further improving mineral resource reserve and emergency response systems, clarifying the principles to be followed in building a strategic mineral resource reserve system, further refining systems related to strategic mineral resource product reserves, capacity reserves, and production site reserves, and improving emergency response measures for mineral resources. Fifth, further improving the supervision and management system, refining the evaluation system for mineral resource development and utilization levels, implementing registration and tiered and classified supervision for entities engaged in mineral resource exploration, and clarifying dispute resolution mechanisms between mining right holders. Legal responsibilities were improved, specifying that violations involving strategic mineral resources shall be subject to heavier penalties within the statutory range. (Xinhua News Agency) Pr-Nd oxide price pulled back slightly on May 22; dysprosium oxide and terbium oxide prices remained stable Spot market: On May 22, the average price of Pr-Nd oxide edged down 0.57% from the previous trading day. Dysprosium oxide and terbium oxide prices remained flat compared to the previous trading day. Currently, rare earth market prices showed a slight correction. Focusing on the Pr-Nd market, mid-week, magnetic material enterprises conducted a round of concentrated procurement, but as the weekend approached, their inquiry activities decreased significantly, with most inquiries pushing for lower prices. Affected by this, the metal market inquiries came under pressure, and some metal enterprises slightly lowered their quotes. The oxide market was also affected; impacted by metal enterprises' price-pushing inquiries, some traders lowered their quotes. However, market confidence recovered somewhat in the short term, and suppliers had low willingness to sell at lower prices, so the overall decline in Pr-Nd products remained limited. Turning to the medium-heavy rare earth market, although market inquiry activities decreased, suppliers showed little willingness to sell at lower prices. Prices of products such as dysprosium and terbium therefore showed no significant fluctuations, maintaining overall stable operation. Overall, as downstream inquiry activities decreased near the weekend with price-pushing inquiries, Pr-Nd product prices saw a slight correction, while medium-heavy rare earth market prices remained relatively firm with stable overall operation. In the short term, as market trading activity picks up, Pr-Nd product prices are expected to move sideways. Institutional Views Guojin Securities research report noted: Rare earth: From the beginning of the year to date, the price center has been continuously rising, which we believe is likely highly correlated with supply-side policy documents issued from 2024 to 2025, as industry supply-side reform continues to advance. Full-year exports in 2025 were -1% YoY, while exports from early 2026 to date increased significantly, indicating that ex-China restocking demand remains substantial. The rare earth sector will continue to see dual appreciation in valuation and earnings, and 2026 is also a critical year for resolving horizontal competition among key targets. Resource side, we recommend attention to China Rare Earth (medium-heavy rare earth leader, biggest beneficiary of supply reform), China Rare Metals and Rare Earth (undervalued, high-growth South China rare earth leader), China Northern Rare Earth (light rare earth leader, significant cost advantages), Bao Gang United Steel (beneficiary of dual supply reform in rare earth and steel); magnetic material segment beneficiary: JL MAG Rare-Earth (magnetic material leader, robotics contributing growth potential). Other related targets include Zhenghai Magnetic Material and Ningbo Yunsheng. According to a Huaxi Securities research report: per the U.S. Geological Survey (USGS), rare earths are relatively abundant in the Earth's crust, but mineable reserves are less than most other mineral products. In 2025, global rare earth reserves were estimated at 85 million mt (in rare earth oxide equivalent, same below), of which China's reserves were 44 million mt, accounting for 51.76%. Production side, global rare earth production in 2025 was 380,000 mt, of which China's production was 270,000 mt, accounting for 71.05%. Midstream, 90% of smelting and processing demand in 2025 was handled by China. Downstream, according to Frost & Sullivan's forecast, global rare earth permanent magnet production in 2025 was 310,200 mt, of which sintered NdFeB production was 296,700 mt (95.65%); China's rare earth permanent magnet production was 284,200 mt (91.62% of global production), of which sintered NdFeB production was 271,800 mt (95.64%). Overall, global rare earth resources are highly concentrated, and China ranks first globally in both rare earth production and reserves. On November 7, 2025, the Ministry of Commerce and the General Administration of Customs jointly announced that from that date until November 10, 2026, six export control measures involving superhard materials, rare earth-related items, lithium batteries, and artificial graphite anode materials would be temporarily suspended, indicating some easing in China-US relations. The US government is actively rebuilding its domestic rare earth industry chain, with US magnet manufacturer eVAC recently shipping its first batch of NdFeB permanent magnets from its Sumter, South Carolina plant. However, in the short term, global rare earth permanent magnet production remains highly concentrated in China. Considering that ex-China capacity release still requires time and given the scale of China's new capacity, China remains the only country in the world with production capabilities across the entire rare earth industry chain for all product categories. The overall scale of the Western rare earth industry chain is far below that of China, with incomplete industry chains and obvious shortcomings. Looking ahead, although downstream new orders remain weak with most enterprises primarily digesting existing orders, some small and medium-sized enterprises' raw material inventory is approaching low levels, highlighting rigid restocking demand. According to a CITIC Securities research report, in 2025 and Q1 2026, earnings growth in the metals sector generally accelerated, with tungsten, lithium, lead-zinc, and rare earth magnetic materials leading the gains, while aluminum, copper, nickel-cobalt-tin-antimony, and gold performed relatively weakly since the beginning of the year. Current metals sector valuations remain at reasonable levels, with aluminum, copper, nickel-cobalt-tin-antimony, and gold valuations at relatively low levels, and valuation rebounds are still expected. Industry dividends pulled back slightly, but forecast dividend yields for some individual stocks still exceed 5%. Looking ahead to 2026, with liquidity shocks easing, supply disruptions occurring frequently, and certain downstream sectors sustaining relatively high prosperity, it is recommended to continue focusing on allocation opportunities in lithium, copper, rare earth, strategic metals, aluminum, and gold sectors. Recommended Reading:

May 22, 2026 19:36 - The 4th China (Jiangxi) International Non-ferrous Metals and Metallurgical Industry Exhibition 2027

The 4th China (Jiangxi) International Nonferrous Metals and Metallurgical Industry Exhibition, 2027 The 4th China (Jiangxi) International Nonferrous Metals and Metallurgical Industry Exhibition in 2027 Date: March 28-30, 2027 Venue: Nanchang Greenland International Expo Center "World Tungsten Capital" "World Copper Capital" "Asia's Lithium Capital" "Rare Earth Kingdom" Concurrent Events: The 4th China (Jiangxi) International Green Mining Exhibition, 2027 The 4th China (Jiangxi) International Foundry, Die Casting, Forging, Heat Treatment and Industrial Furnace Exhibition, 2027 [Jiangxi's Many Firsts] New China's first aircraft, first diesel wheeled tractor, first military sidecar motorcycle, first coastal defense missile, first artificial satellite, and today's C919 large passenger aircraft were all born here. [Industrial Advantages] The nonferrous metals industry is the largest pillar industry of Jiangxi Province. The energy consumption dual controls, dual carbon policies, and the new connotations of high-quality development have put forward new requirements for strengthening and expanding the nonferrous metals industry. Promoting the further healthy, rapid, and orderly development of the nonferrous metals industry and enhancing its core competitiveness is an inevitable requirement for transforming from a province rich in nonferrous metal resources to a province with a strong nonferrous metals industry, and is also an important lever for Jiangxi to achieve carbon peaking by 2030. Leveraging Jiangxi Province's abundant nonferrous mineral resources, Jiangxi's nonferrous metals industry has developed rapidly, with continuously expanding scale and improving standards. It has become Jiangxi's largest pillar industry and is currently a key "trillion-yuan-level" industry being cultivated in Jiangxi. It is the undisputed "ballast stone" of Jiangxi's manufacturing sector. Jiangxi has become an important nonferrous metal ore mining and production site in China. Jiangxi Province enjoys superior metallogenic geological conditions and abundant mineral resources, making it one of China's important bases for nonferrous metals, rare metals, rare earth, and uranium minerals, with a relatively high degree of mineral resource complementarity. Jiangxi's seven major categories of minerals — copper, tungsten, rare earth, uranium, tantalum-niobium, gold, and silver — are known as the "Seven Golden Flowers." According to Jiangxi Province's "2+6+N" Action Plan for High-Quality Leapfrog Industrial Development, the province's nonferrous metals industry plans to achieve a trillion-yuan level in main business revenue. To promote the healthy development of Jiangxi Province's nonferrous metals industry, facilitate foreign economic and trade cooperation, and guide Jiangxi's nonferrous metals industry to align with international standards, the Organizing Committee, after conducting multiple in-depth grassroots surveys and project analyses with government authorities and industry associations, has decided to hold the "4th China (Jiangxi) International Nonferrous Metals and Metallurgical Industry Exhibition, 2027" at the Nanchang Greenland International Expo Center on March 28-30, 2027. We look forward to seeing you there. [ Exhibition Dates ] Registration and Booth Setup: March 26-27, 2027 Opening Ceremony: March 28, 2027, 9:30 Exhibition and Trading: March 28-30, 2027 Dismantling: March 30, 2027, 14:00 [Scope of Exhibits] Non-ferrous Metal Raw Materials: copper, aluminum, magnesium, titanium, zinc, lead, manganese, zirconium, vanadium, nickel, molybdenum, silicon, antimony, tin, chromium, tungsten, tantalum, indium and other non-ferrous metal mineral product raw materials, magnetic materials, rare and rare earth materials, precious metal materials and various alloy materials; Non-ferrous Metal Products: copper products, aluminum products, titanium alloy products, magnesium alloy products, powder metallurgy products, etc.; Metallurgical Equipment and Technology: smelting furnaces and kilns, refining equipment, smelting pumps and valves, conveying equipment, heat exchange equipment, flue gas acid-making equipment, corrosion-resistant equipment, hydrometallurgy, electrolysis equipment, large power rectifier power supplies, electrolytic cells, extraction equipment, surface treatment equipment, etc.; Metal Processing Machine Tools: lathes, milling machines, sawing machines, drilling machines, grinding machines, punch presses, boring machines, machining centers, electrical discharge machines, wire cutting machines, laser processing equipment, etc.; Metal Automation Control Equipment: frequency converters, fieldbuses, industrial computers, instruments and meters, automation control, robots, electronic application systems, weighing instruments and information solutions for equipment manufacturing, etc.; Auxiliary Materials for Metal Production: chemicals, solvents, refractory materials, catalysts, gases, lubricating oils, etc.; Powder Metallurgy: raw materials, equipment, products, 3D printing, polymer powder materials, ceramic powder materials; Casting, Die Casting and Forging: castings, casting equipment, casting materials, casting molds, casting/pouring robots, new casting technology and supporting products, various heat treatment furnaces, industrial furnaces, die castings, die casting molds, die casting machines and peripheral equipment, post-processing equipment for die castings, surface treatment technology and equipment, die casting robots, new die casting technology and supporting products, forgings, flanges and rings, forging equipment and accessories, surface treatment technology and equipment, automation, forging mold manufacturing technology and equipment, forging raw materials. Geological (Mine) Exploration Technology and Equipment: geophysical exploration technology, geochemical exploration technology, aerial survey and remote sensing technology, surveying and mapping technology, geological data processing, mineral product analysis, laboratory instruments and meters. Mining Technology and Equipment: excavation equipment, drilling and rock drilling equipment, loading equipment, transportation equipment (excavators, loaders, underground mining vehicles, mining dump units), hoisting equipment, drilling, construction machinery, etc. [Media Promotion] 65 authoritative financial media outlets including Jiangxi Daily, Jiangxi Television Economic Channel, Dajiang Finance Channel, Jiangxi Net, China Net, China Daily Net, and China Finance Net; 10 major self-media platforms including Sohu, NetEase, and Toutiao; 53 industry-leading professional media outlets including China Mining Net, China Excavator Net, China Foundry Net, China Die Casting Net, China Auto Manufacturing Net, World Aluminum Net, China Nonferrous Metals Net, Nonferrous Metals Information Net, and Metalworking, along with 180 other industry-related professional media outlets; Comprehensive coverage of key words search clients through online search platforms such as Baidu Promotion and 360 Promotion; [Concurrent Events] 2027 China Foundry Technology Innovation Outstanding Contribution Award Ceremony 2027 China Metallurgical Melting and Casting Technology Seminar 2027 China Recycled Metals Industry Chain Integrated Development Forum 2027 China NEV and Auto Body Lightweighting Peak Forum 2027 China Green Mine Development Forum [Exhibition Rules] ★ Standard booth 3m×3m: China enterprises: RMB 9,800 yuan/booth; overseas enterprises: RMB 15,800 yuan/booth; ★ International brand booth (9 ㎡, deluxe decoration) RMB 12,800 yuan/booth; overseas enterprises: RMB 18,800 yuan/booth; ★ Indoor bare space (minimum 36 ㎡): China enterprises: RMB 1,000 yuan/㎡; overseas enterprises: RMB 2,000 yuan/㎡; Booth equipped with: two fluorescent tubes, one waste basket, display boards, header board, one table and two chairs, air conditioning, lighting, security, and cleaning services. Note: Bare space does not include any exhibition facilities. Special decoration management fees and hydropower fees charged by the venue shall be borne by the exhibitors and their special decoration contractors. [Organizing Committee Secretariat] Contact: Song Jia 132-1700-0270 (same on WeChat) Official website: http://www.jxysjs.net

May 12, 2026 15:30 - New Aluminum Compound Could Replace Rare Metals, Reducing Costs and Boosting Sustainability

On May 8, scientists at King's College London in the UK developed a powerful new-type aluminum compound whose unique triangular structure endows it with extraordinary stability and reactivity, enabling it to replace expensive rare metals and thereby significantly reduce costs. This discovery is expected to give rise to more environmentally friendly and economical industrial processes, and even create entirely new materials. The related findings were published in the latest issue of *Nature Communications*.

May 9, 2026 18:37 - Focusing on Tin, Tantalum, and Tungsten Resource Development, SMM Visited MMR to Deepen Industry Collaboration and Alignment

On April 16, Ye Jianhua, Director and Supervisor of SMM's Industry Research Department, Feng Chundi, Expert of SMM's Industry Research Institute, and Wu Tao, SMM Overseas Marketing Manager for Copper and Tin, visited Mining Mineral Resources (MMR) for a field trip and exchange, where they received a warm welcome from MMR's leadership. During the exchange, MMR and SMM engaged in in-depth discussions on the current status of the strategic minor metal industry and cross-border supply chain cooperation. MMR has been deeply engaged in compliant mining of critical minerals for over 15 years, with a strategic focus on three key minerals — tin, tantalum, and tungsten. The company holds multiple mining licenses in mineral-rich regions of the DRC, with concentrated resource deployment and exceptional endowment. The enterprise strictly adheres to compliant mining, full-process traceability, and international operational standards, ensuring long-term stable and compliant mine operations. SMM has long been deeply engaged in non-ferrous and rare metals, with core coverage spanning price quotations, industry surveys, and market analysis, comprehensively empowering global mineral trade and industry chain integrated services. Leveraging their respective business strengths, both parties exchanged practical experience on ex-China mineral development, compliance system building, raw material circulation coordination, and industry development trends, laying a solid foundation for subsequent industrial synergy and resource collaboration. Mining Mineral Resources (MMR) Overview Mining Mineral Resources (MMR) has been deeply engaged in compliant mining of critical minerals for over 15 years, with a core focus on the 3T strategic minerals (tin, tantalum, and tungsten). The company holds a portfolio of multiple mining licenses in mineral-rich regions of the DRC: tin (14 licenses covering 2,800 sq km), tantalum (6 licenses covering 400 sq km), and tungsten (1 license covering 300 sq km). The company upholds compliant procurement, full traceability, and international standard compliance systems, building a solid foundation for business operations. Key Tin Producer in Africa • 11 mechanized mines (including open-pit and underground mines) • Annual tin concentrates capacity: 10,000 mt Annual trading volume: 6,500 mt; annual mechanized mining production: 3,500 mt. Mechanized Mining Operations 8 beneficiation plant areas with a combined feed capacity of over 1,500 mt per hour; monthly tin concentrates production of 300 mt; creating employment opportunities and empowering inclusive community development. Smelting Production and Global Supply LME Grade A tin equivalent; Responsible Minerals Initiative (RMI) certified smelter; annual refined tin capacity: 4,500 mt. Tantalum Mining Operations The only mechanized tantalum ore beneficiation plant in the DRC; capacity: 20 mt per year of high-grade tantalum concentrates (grade 30% and above); equipped with modern laboratory detection and quality assay facilities. Ore-to-Alloy Entire Industry Chain Lead-free and tin-lead solder alloys, available in bars, wires, electrodes, and casting ingots. The only enterprise in Africa with a complete ore-to-alloy entire industry chain. Corporate Social Responsibility MMR is well aware of its significant social responsibility to the communities in the mining areas. The corporate social responsibility system is built on four core pillars: healthcare, education development, infrastructure improvement, and entrepreneurship empowerment. Scheduled to be held on October 13-14, 2026 in Lusaka, Zambia. Welcome to join us~ Conference Contact : Wu Tao: 18270916376 jennywu@smm.cn

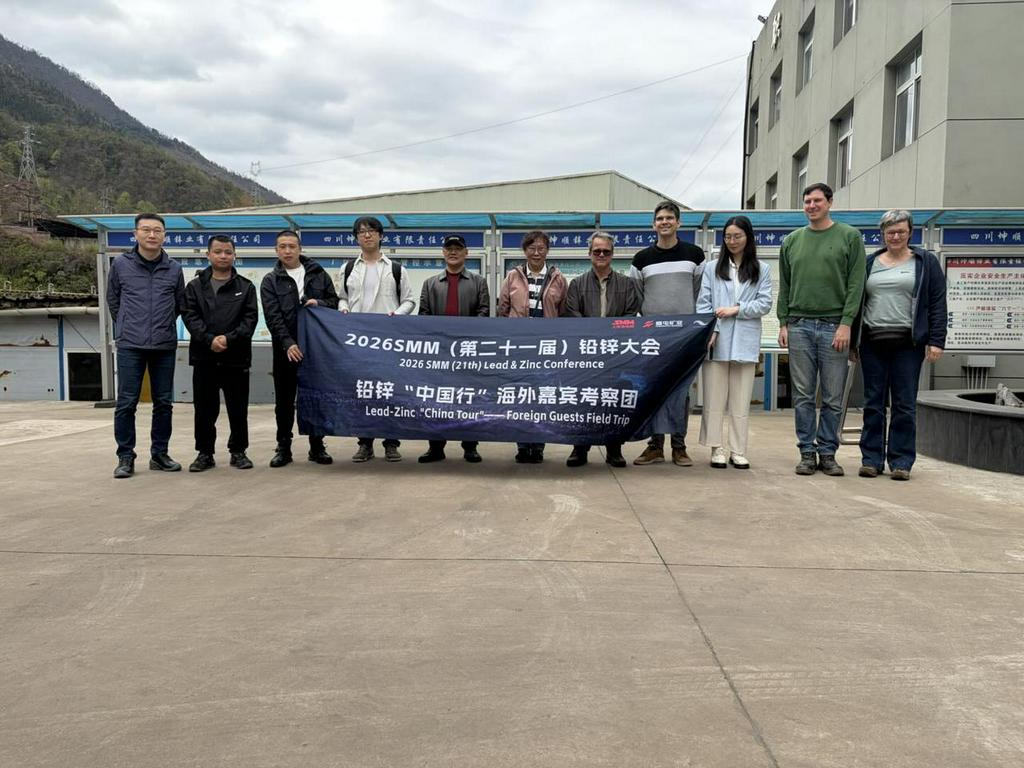

Apr 29, 2026 17:25  Post-Conference Tour: Connecting Global Lead-Zinc Giants with Key Chinese Players

Post-Conference Tour: Connecting Global Lead-Zinc Giants with Key Chinese PlayersThe 2026 SMM (21st) Lead & Zinc Conference and Industry Expo opened grandly at Howard Johnson Agile Plaza in Chengdu, Sichuan during March 25–27 2026. Organized by SMM, the event brought together global enterprises, professional experts and industry peers from across the entire lead and zinc supply chain. Participants focused on industry hot topics, analyzed market trends and explored development strategies, establishing a highly efficient platform for communication and collaboration to support high-quality growth of the sector. To further strengthen the overseas delegation’s comprehensive understanding of China’s lead and zinc industrial chain and build closer connections between international industry peers and key producers in China, SMM led a high-level overseas delegation on a multi-day industrial tour starting on the afternoon of March 27. The delegation included representatives from global giants, such as Nyrstar, a top European lead and zinc smelting firm, Nexa Resources, a South American giant in lead-zinc mining and smelting, and Befesa, a pioneer in zinc recycling. During the tour, the delegation visited 8 Chinese enterprises. including: COSCO Shipping Sichuan Chengtun Zinc & Germanium Technology Sichuan Kunshun Zinc Industry Yunnan Luoping Zinc & Electricity Hongzhou Hongqian Nonferrous Chemical Yunnan Zhenxing Industrial Group Mengzi Mining & Metallurgy Danxia Smelter of Shenzhen Zhongjin Lingnan Nonfemet The delegation members went deep into production sites, held in-depth discussions and exchanges, and gained a full picture of China’s lead and zinc industry in terms of production operations, technological innovation, capacity scale and market layout, greatly enhancing their insight into and understanding of the entire industrial chain. SMM has systematically compiled detailed information of all enterprises that were visited during this tour, with details below: COSCO Shipping On the afternoon of March 27, the delegation visited COSCO Shipping for an exchange, where they received a warm welcome from the company's leadership. Both sides engaged in discussions on topics such as equipment transportation and technological upgrades. Sichuan COSCO Shipping Logistics Supply Chain Management Co., Ltd. is a wholly-owned subsidiary of COSCO Shipping Logistics Supply Chain Co., Ltd., registered and established in Chengdu, Sichuan Province, with an investment of 30 million yuan. COSCO Shipping Logistics Supply Chain Co., Ltd. is affiliated with China COSCO Shipping Corporation Limited and serves as a core member of the "shipping, ports, and logistics" segment of COSCO Shipping Group, as well as an important component of its global digital supply chain system. The company operates warehouse space exceeding 6 million m², including 19 futures delivery warehouses. China COSCO Shipping Corporation Limited is a globally leading shipping enterprise group, with a combined fleet capacity of 130 million DWT across 1,535 vessels, ranking first in the world. Sichuan COSCO Shipping Logistics Supply Chain Management Co., Ltd. holds business qualifications and an operational scope covering multiple transportation modes including sea, land, air, and rail, providing comprehensive logistics services spanning both international and Chinese markets. Since entering the non-ferrous metals delivery warehouse business in 2016, the company has adhered to the principle of "client-centered and market-oriented," continuously enhancing its service capabilities and achieving steady business growth. Currently, at key logistics periods such as Shanghai Baoshan, Shanghai Yangshan, and Yixing in Jiangsu, the company successfully operates delivery warehouses designated by the Shanghai Futures Exchange for copper, nickel, zinc, and other products. It has become one of the three major non-ferrous metals warehouses of SHFE and was honored with the title of "Top Ten Designated Non-Ferrous Metals Delivery Warehouses" by the Shanghai Futures Exchange for two consecutive years. Sichuan Chengtun Zinc & Germanium Technology Co., Ltd. On March 28, the delegation visited Sichuan Chengtun Zinc & Germanium Technology Co., Ltd. (Shimian City). Both sides engaged in in-depth exchanges on the development of the zinc smelting industry, with a focus on thorough discussions regarding product processing, production techniques, capacity scale, market trends, and the current challenges facing the industry. Sichuan Chengtun Zinc & Germanium Technology Co., Ltd. was established on December 6, 2015, with a registered capital of 1.6 billion yuan. The company has an annual capacity of 300,000 mt of electrolytic zinc, 150,000 mt of sulphuric acid, 400,000 mt of electrolytic zinc waste residue processing, and 40 mt of high-purity germanium dioxide. On January 16, 2019, the company was approved by the China Securities Regulatory Commission and merged into the publicly listed firm Chengtun Mining Group Co., Ltd. The company's main business includes smelting and R&D of zinc-germanium series products, as well as comprehensive recovery of multiple metals. It has formed a complete industry chain from zinc concentrates entering the plant to finished products leaving the plant. Its production lines include zinc calcine, electrolytic zinc, electrolytic zinc waste residue processing, and comprehensive recovery of rare and precious metals. Sichuan Kunshun Zinc Industry Co., Ltd. (Shimian City) On March 28, the delegation headed to Sichuan Kunshun Zinc Industry Co., Ltd. (Shimian City) for a visit and exchange, where they received a warm reception from the enterprise. Both parties held in-depth discussions and exchanges on zinc smelting, covering topics such as production costs, production and market landscape, raw material procurement and processing, industry chain competitive advantages, and distinctive process technologies. Sichuan Kunshun Zinc Industry Co., Ltd. is a specialized and green environmental protection enterprise jointly invested and established by Sichuan Metallurgical Holding Group Co., Ltd. and Shimian Dongshun Zinc Industry Co., Ltd. to implement the national green production philosophy, actively develop the circular economy, and promote the comprehensive utilization of solid waste resources. It integrates solid waste treatment, recycling, and resource regeneration. The company primarily uses high-tech methods to carry out clean utilization and harmless treatment of heavy metal-containing waste generated by industries such as metallurgy and chemicals, eliminating the environmental impact of heavy metal solid waste at the source. The company was established in 2021 and is located in Zhuma Industrial Park, Shimian County, Ya'an City, Sichuan Province, covering an area of 65 mu with a total investment of 180 million yuan. The company has built a 3.5m × 50m Waelz rotary kiln production line, equipped with advanced and well-established low-grade zinc oxide production technology, achieving a resource recovery utilization rate of over 95% and effectively managing waste gas, noise, solid waste, and groundwater risks. It is also equipped with supporting facilities including desulphurization, denitrification, and flue gas defogging towers, as well as a wastewater treatment station, raw material warehouse, raw material pre-washing workshop, water slag processing workshop, biomass semi-gasification furnace, zinc crystallized salt workshop, production safety and environmental protection center, and laboratory for detection and testing. The company holds qualifications for treating hazardous waste categories including HW12, HW17, HW23, HW48, and HW49, with an annual capacity to process 100,000 mt of zinc-containing waste. Its main products include low-grade zinc oxide and zinc crystallized salt. The company has always upheld the green and environmentally friendly development philosophy, adhering to the fundamentals of "being responsible for the environment, for clients, and for employees," guided by technological innovation, and targeting the "reduction, recycling, and detoxification" of solid waste pollution prevention and control. The company is committed to building a modern "solid waste" management and disposal service provider, actively carrying out emergency environmental protection disposal, proactively assuming social service functions, and making positive contributions to promoting the circular economy development in Sichuan and strengthening the ecological civilization construction of lucid waters and lush mountains! Yunnan Luoping Zinc & Electricity Co., Ltd. (Qujing City) On March 30, the delegation visited Yunnan Luoping Zinc & Electricity Co., Ltd. (Qujing City) for exchanges. During the meeting, both sides conducted in-depth discussions on key topics including magnesium removal process optimization, production management organization, and raw material substitution plans, and put forward constructive suggestions on improving the plant environment. Yunnan Luoping Zinc & Electricity Co., Ltd. was established to fully leverage Luoping's local hydropower and lead-zinc mineral resource advantages. In accordance with the "ore, electricity, and smelting integration" development strategy proposed by the Luoping County Party Committee and County Government, and the overall requirements of the Municipal Party Committee and Municipal Government for the reform of industrial enterprises across the city, the company was registered and established at the Yunnan Provincial Administration for Industry and Commerce on December 21, 2000. It was listed on the Shenzhen Stock Exchange A-share market in 2007 and is a state-controlled enterprise under Luoping County. The company's assets are an optimized combination of three components: hydropower, lead-zinc mines, and zinc smelting. In terms of company assets, they are primarily composed of three advantageous resources of Luoping: mineral, hydropower, and zinc smelting. These mainly include six production units: Luoping County Fule Lead-Zinc Mine with an annual processing capacity of 100,000 mt of raw ore, Lazhuang Power Plant with annual power generation of 250 million kWh (installed capacity of 60,000 kW), a zinc smelter with an annual output of 120,000 mt of electrolytic zinc, a zinc powder plant with an annual output of 12,000 mt of ultra-fine zinc powder, a comprehensive utilization plant with an annual processing capacity of 129,500 mt of zinc slag, and a sulphuric acid plant with an annual output of 140,000 mt of sulphuric acid, achieving a total annual industrial output value exceeding 2 billion yuan. The company has six wholly-owned subsidiaries. The company's main businesses include hydropower generation, mining of lead, zinc, and other non-ferrous metals, as well as the production and sales of zinc smelting and its extended products. It is currently the only publicly listed firm in China's zinc smelting industry that integrates mining, power generation, chemical processing, and smelting. Its products include zinc sulphide concentrates, lead concentrates, zinc ingots, industrial sulphuric acid, ultra-fine zinc powder, cadmium, germanium concentrates, silver concentrates, copper concentrates, zinc alloys, industrial and residential electricity, edible oils and fats, among others. Its main product, "Jiulong" brand zinc ingots, is popular in non-ferrous product markets in and outside China thanks to its superior product quality and corporate reputation. Honghe Prefecture Hongqian Non-ferrous Chemical Joint-Stock Co., Ltd. On March 31, the delegation visited Honghe Prefecture Hongqian Non-ferrous Chemical Joint-Stock Co., Ltd. for exchanges. The two sides held in-depth discussions on topics including the economic benefits of smelting by-products, energy utilization efficiency, the current status of enterprise development, and future cooperation intentions. Honghe Prefecture Hongqian Non-ferrous Chemical Joint-Stock Co., Ltd. was established on August 1, 2007, with a registered capital of 50 million yuan. The total investment in project construction was 475.5543 million yuan. The company currently has over 600 employees and covers an area of 443 mu. The plant is located in the Heishenmiaobo Industrial Zone, situated in the central area of the Gejiu-Kaiyuan-Mengzi urban cluster. The company is a new-type joint-stock enterprise centered on crude lead smelting, integrating sulphur dioxide acid production, waste heat power generation, lead electrolysis, and recovery of precious and rare metals such as gold, silver, antimony, and bismuth, with further extension into deep processing of lead-series products including red lead, massicot, electrode plates, and storage batteries. It is a benchmark enterprise among private lead smelters in the city, featuring a relatively large scale, advanced technology, compliance with environmental protection standards, comprehensive utilization of resources, and a complete industry chain. The company pioneered the application of new technologies to upgrade and transform the traditional crude lead smelting model among private enterprises in the city. The company has formulated the working philosophy of "prioritizing environmental protection, ensuring safety, attracting talent, enforcing strict management, and enhancing efficiency," and continues to drive high-quality development. In April 2007, the company commissioned China ENFI Engineering Technology Co., Ltd. to conduct a feasibility study on the lead smelting technological transformation project, and determined a comprehensive industrial facility technological transformation project with a total investment of 490 million yuan and an annual capacity of 60,000 mt of crude lead. On December 21, 2009, the "Demonstration Project of Oxygen-Enriched Bottom-Blowing Lead Smelting Technology with Annual Output of 60,000 mt of Crude Lead" was designated by the Provincial Department of Science and Technology as a 2009 Yunnan Provincial Science and Technology Innovation Project. In 2010, it was further designated as a key industrial project by the provincial, prefectural, and municipal governments. On November 14, 2011, the company obtained ISO9001:2008 quality management system certification. On March 7, 2012, "HSPb99.94PCT" was successfully registered on the London Metal Exchange. In 2019, the company successively passed the safety completion acceptance and environmental impact assessment completion acceptance, fully achieving compliant operations and sustainable development. Yunnan Zhenxing Industrial Group Co., Ltd. On March 31, the delegation headed to Yunnan Zhenxing Industrial Group Co., Ltd. for a visit and exchange. Both parties conducted in-depth discussions on topics including Yunnan Province's mineral resource endowment, smelting industry development trends, corporate business strategies, and technological innovation applications, jointly assessing the current status and prospects of the industry and analyzing the challenges and opportunities ahead. Yunnan Zhenxing Industrial Group Co., Ltd. (hereinafter referred to as "the Group") was founded in 1996 and is located in the Chongposhao New Materials Industrial Park, Shadian Sub-district Office, Gejiu City. The Group currently has 7 subsidiaries, 2 holding companies, and 1 equity-participation company, with approximately 3,000 employees. Its capacity reaches annual output of crude lead (100,000 mt), electrolytic lead (60,000 mt), zinc ingot (20,000 mt), lead-acid battery plates (9 million sets), lead-acid batteries (6 million units), superphosphate (350,000 mt), sulphuric acid (200,000 mt), and monoammonium phosphate (MAP) (60,000 mt). The Group has established five major production sites and five major product brands covering crude lead raw material, lead-zinc smelting, power supply manufacturing, fertilizer and chemical production, and resource recovery. It has formed an internal industrial cycle spanning lead ore mining—lead-zinc smelting—lead-based alloy melting—battery manufacturing—waste battery recycling—precious metals production, making it one of the few private non-ferrous enterprises in China with a complete lead industry chain. Since 2013, the Group has been consecutively recognized as one of the Top 100 Non-Public Enterprises in Yunnan Province. In 2025, it ranked 41st among the "Top 100 Non-Public Enterprises in Yunnan Province" and was selected for the first time into the "Top 20 Private Enterprises in Innovation Capability," ranking 7th. Yunnan Shadian Lead Industry Co., Ltd., a subsidiary controlled by the Group, ranked 71st. The Group has received nearly 100 honors at various levels, including "High-tech Enterprise," "Outstanding Private Technology Enterprise," "Enterprise with Harmonious Labor Relations," "Provincial Model Collective for Ethnic Unity and Progress," and "Key Enterprise for Industrial Development in Honghe Prefecture" in Yunnan Province. The Group's Yunsha brand lead ingot was successfully registered on the London Metal Exchange in 2007 and on the Shanghai Futures Exchange in 2020. In 2021, the Group was rated AAA in enterprise credit rating in the national non-ferrous metals industry. In August 2024, it was designated as a "Qiangyuan Zhuqi" Industry-Finance Service Base by the Shanghai Futures Exchange. Looking ahead, the Group will pursue the philosophy of "seeking survival, pursuing development, and accelerating enterprise transformation and upgrading," adhering to the working approach of "rooting in Honghe, basing in Yunnan, radiating to surrounding regions, and expanding across China." It will thoroughly implement strategies of enterprise management transformation, technology-driven development, talent empowerment, and sustainable development, striving to achieve significant increases in capacity and production of major products by 2035, with gross industrial output value up YoY, and to build itself into a 10 billion green lead-zinc comprehensive recycling technology enterprise. Mengzi Mining and Metallurgy Co., Ltd. On March 31, SMM and the field trip delegation headed to Mengzi Mining and Metallurgy Co., Ltd. for a visit and exchange. Both parties engaged in in-depth discussions on the entire zinc smelting process, covering topics including production technology, raw material supply, product sales, environmental protection governance, and future development plans, aiming to share experience, address industry pain points, and jointly clarify the direction of development. Mengzi Mining and Metallurgy Co., Ltd. was established in 1996. It is a resource-based mining and metallurgy enterprise integrating R&D, exploration, mining, mineral processing, smelting, and trading, with a focus on comprehensive utilization of resources. The company is one of the few comprehensive private enterprises in the non-ferrous metal industry that possesses an entire industry chain and operates independent trading and supply chain business platforms. It is among the top 100 enterprises in Yunnan Province and a key enterprise in Honghe Prefecture. Shenzhen Zhongjin Lingnan Nonfemet Co., Ltd. — Danxia Smelter On April 2, the SMM delegation visited Zhongjin Lingnan's Danxia Smelter for a survey and field trip to the core plant area. In-depth discussions were held on production operations, technological R&D, and raw material procurement, covering key topics such as production capacity, technical cooperation, and raw material procurement strategies. Shenzhen Zhongjin Lingnan Nonfemet Co., Ltd. (hereinafter referred to as "Zhongjin Lingnan") was established in September 1984 and listed on the Shenzhen Stock Exchange in January 1997 (stock code: 000060). It is an internationalized entire industry chain resource company primarily engaged in lead, zinc, and copper mining, mineral processing, and smelting, as well as comprehensive recovery of rare, scattered, and precious metals. It is a publicly listed firm controlled by Guangsheng Holdings Group, a key wholly state-owned enterprise under Guangdong Province. Zhongjin Lingnan's business covers segments including mines, smelting, new materials, and supply chains. It has 23 directly affiliated enterprises, wholly-owned and controlled subsidiaries. Major operating entities include Fankou Lead-Zinc Mine, Shaoguan Smelter, Danxia Smelter, Zhongjin Copper Co., Guangxi Mining Co., Perilya Limited in Australia, Zhongjin Technology Co., and Huajiari Co. The company has an annual output of 300,000 mt of lead and zinc metal content in concentrates, 450,000 mt of smelted lead and zinc products, 450,000 mt of copper cathode, 21,000 mt of aluminum extrusion, 20,000 mt of battery zinc powder, and 5,400 mt of composite metal materials. Among these, its battery zinc powder ranked first in Chinese market share, nickel-metal hydride and nickel-cadmium battery electrode sheets & plates materials ranked first in Chinese market share, and thermal bimetal ranked first in Chinese market share. The 2026 field trip brought together some global lead and zinc industry leaders for an inspiring and highly productive journey across China’s leading smelters and enterprises. The warm welcome, operational excellence, and innovative technologies on display made this event a resounding success — and we extend our deepest gratitude to all the companies and participants who made it happen. Looking ahead – Save the date for 2027: We are excited to announce that the 2027 SMM (22nd) Lead & Zinc Conference and Industry EXPO will take place from March 17–19, 2027 in Kunming, Yunnan, China . This premier event will once again bring together the global lead-zinc community for high-level networking, insight sharing, and industrial exploration. Interactive call – We want to hear from you: As we plan the field trip for the 2027 conference, we’d love your input. Which smelters or companies would you most like to visit for technical exchange and on-site learning? Please share your suggestions in the comments below — your feedback will help shape the 2027 experience. Let us know where the industry should go next!

Apr 7, 2026 14:32- Multiple Bearish Factors Stall the Uptrend; Short-Term Correction in the Tantalum Market, with Solid Medium and Long-Term Support [SMM Analysis]

[Multiple Bearish Factors Stall the Uptrend; China’s Tantalum Market Undergoes Short-Term Adjustment While Medium and Long-Term Support Remains Solid] Recently, the sustained upward momentum in China’s tantalum products market came to a halt, with the overall market entering a phase of temporary consolidation and adjustment. Upward momentum slowed markedly in the short term, mainly due to three core factors: the transmission of macro sentiment, changes in circulating supply, and weakening raw material costs.

Mar 29, 2026 13:36 - Chinese Team Sets New Record in CZTSSe Thin-Film PV Tech, Hits 16.6% Efficiency

Recently, the team led by Meng Qingbo at the Institute of Physics, Chinese Academy of Sciences, once again set a new record in new-type thin-film PV copper-zinc-tin-sulfur-selenium (CZTSSe) technology, raising the battery’s certified efficiency to 16.6%, marking the technology’s official crossing of the critical threshold for industrialisation from 15 to 16. Composed of common, low-cost elements such as copper, zinc, and tin, CZTSSe materials not only avoid reliance on rare metals but also offer strong resistance to space radiation. At present, the team has also completed the development of high performance flexible batteries and modules, and this technology is expected to achieve large-scale application in fields such as low-Earth-orbit satellite internet, space-based energy bases, and aerospace equipment in the future. This progress not only established China’s internationally leading position in this field, but also opened up strategic, high-value-added application prospects for tin metal in new energy and deep-space exploration.

Mar 27, 2026 15:19 - [SMM Analysis] Metal Rhenium Spot Market Analysis and Market Outlook

Currently, China's spot market for metallic rhenium exhibits an operational pattern characterized by divergence between upstream and downstream segments of the industry chain, bilateral supply-demand gaming, and price consolidation at highs. The overall market is jointly influenced by multiple factors including macro investment sentiment, industry chain stockpiling pace, ex-China supply chain risks, and domestic supply-demand fundamentals. I. Upstream: Price Range Held Steady, Producers Accelerated Shipment Pace Mainstream upstream producers of metallic rhenium in China maintained stable raw material quotations, with the core price range controlled around 28,000, while only a few producers raised raw material quotations to around 30,000. The overall price tiers were clear with no wild swings. From the market circulation perspective, upstream producers' willingness to sell increased recently, with shipment frequency rising significantly. II. Midstream: Scheduled Production Concentrated, Low Acceptance of High-Priced Ammonium Perrhenate Midstream refineries and rhenium processing enterprises were all in scheduled production status, with pre-holiday order delivery cycles relatively concentrated, and most producers' orders scheduled for delivery completion in March and April. Cost side and procurement mentality, midstream processing enterprises generally showed low acceptance of high-priced ammonium perrhenate, with the procurement side more inclined toward rational price negotiation and resistant to rushing to buy amid continuous price rise. This mentality directly constrained the upside room for ammonium perrhenate prices. III. Downstream: Investment Sentiment Cooled, Industrial Demand Steadily Recovered The downstream market demand side exhibited clear structural divergence, with investment demand and industrial demand trending in opposite directions, becoming the core factor affecting short-term market sentiment. On one hand, previously active investment demand gradually cooled, market investment atmosphere faded, retail investors showed panic-driven exit sentiment, and low-price dumping phenomena emerged successively in the market. Some holders chose to sell below market price to quickly recover funds, which to some extent impacted short-term spot market transaction prices. On the other hand, industrial demand exhibited a healthy trend of steady recovery and sustained growth. As the core rigid demand support for metallic rhenium, the recovery of industrial demand provided solid fundamental support for the market, offsetting some of the bearish impact from investment-driven selling. IV. Outlook Forecast Combining the macro market environment with industry chain supply-demand fundamentals, the current core logic of China's rhenium market is clear, with bullish and bearish factors intertwined in gaming, jointly driving prices to consolidate at highs. Specific influencing factors and outlook are as follows: Short-term, influenced by the international macro environment, investment enthusiasm in the energy sector continued to surge, diverting market funds, while overall investment sentiment in the non-ferrous metals sector pulled back notably. This sentiment gradually transmitted to the niche rare metal rhenium market, suppressing investment-side enthusiasm. Additionally, upstream and downstream enterprises in the industry chain had completed phased restocking before and after Chinese New Year, with market inventory at a relatively ample level. Raw material prices lacked momentum for significant rallies, and short-term upside room for prices was limited. Long-term, gaming in the international critical minerals field intensified, with US-Chile critical minerals consultations continuing to advance, and the trend toward exclusive cooperation in global critical minerals supply chains becoming increasingly evident, directly leading to declining stability of ex-China ammonium perrhenate import channels and continuously climbing external supply risks. Ammonium perrhenate supply showed a tightening trend, providing support for prices.

Mar 19, 2026 17:26