182results found for 'private enterprises'

Sort by : |

- Total exports of electric two-wheelers in Q1 2026 surged significantly, up 68.2% YoY.

[E-bike Market Dynamics] According to data from the General Administration of Customs, exports of electric motorcycles and bicycles grew 18.1% YoY in 2025. In addition, in Q1 2026, exports of electric motorcycles and bicycles by private enterprises were up 30% YoY; total exports of electric two-wheelers across the industry reached approximately 7.2 million units, up 68.2% YoY.

May 9, 2026 21:03 - National Energy Administration: Investment in Hydrogen Energy, New-Type Energy Storage and Others Accelerated in Q1

The National Energy Administration held a press conference on April 27 to present the national energy situation and development achievements in Q1 2026. Energy investment maintained relatively fast growth in Q1, providing strong support for the turnaround of national fixed asset investment to positive growth. The power grid's role in ensuring security and expanding investment continued to be demonstrated, and investment in areas such as hydrogen energy, coal-to-oil and gas, and new-type energy storage accelerated its release. Private enterprises deeply participated in national science and technology projects in the energy sector, and a number of major projects were accelerated, providing strong support for China's energy security.

Apr 28, 2026 15:58 - US Dollar Weakened, Metals Rose Broadly, Alumina Up Over 3%, Lithium Carbonate and SHFE Nickel Up Over 2%, Polysilicon Led Declines [SMM Midday Review]

SMM April 27 News: Metals market: As of the midday close, domestic market base metals rose across the board. SHFE copper was up 0.38%, SHFE aluminum up 0.3%, SHFE lead up 0.3%, SHFE zinc up 0.7%, SHFE tin up 0.48%, and SHFE nickel up 2.62%. In addition, the most-traded casting aluminum futures rose 0.4%, the most-traded alumina contract rose 3.36%, the most-traded lithium carbonate contract rose 2.75%, the most-traded silicon metal contract rose 0.29%, and the most-traded polysilicon futures fell 4.47%. Ferrous metals mostly rose. Iron ore was flat at 786 yuan/mt, rebar edged up, hot-rolled coil rose 0.15%, and stainless steel rose 1.26%. Coking coal and coke: the most-traded coking coal contract rose 1.23%, and the most-traded coke contract rose 0.44%. Overseas market base metals: as of 11:43, LME metals mostly rose. LME copper was up 0.51%, LME aluminum up 0.95%, LME lead up 0.1%, LME zinc up 0.58%, LME tin edged down, and LME nickel was up 0.71%. Precious metals: as of 11:43, COMEX gold fell 0.11% and COMEX silver fell 0.38%. Domestic precious metals: the most-traded SHFE gold contract rose 0.12%, and the most-traded SHFE silver contract fell 0.08%. In addition, as of the midday close, the most-traded platinum futures rose 1.21%, and the most-traded palladium futures rose 1.52%. As of the midday close, the most-traded Europe containerized freight index contract rose 1.03% to 2,209.8 points. As of 11:43 on April 27, midday futures quotes for selected contracts: Spot and fundamentals Copper: Today, Guangdong #1 copper cathode spot prices against the front-month contract: high-quality copper was quoted at a premium of 280 yuan/mt, flat with the previous trading day; standard-quality copper was quoted at a premium of 200 yuan/mt, flat with the previous trading day; SX-EW copper was quoted at a premium of 140 yuan/mt, flat with the previous trading day. The average price of Guangdong #1 copper cathode was 103,085 yuan/mt, up 290 yuan/mt from the previous trading day; the average price of SX-EW copper was 102,985 yuan/mt, up 290 yuan/mt from the previous trading day. Spot market: After the weekend, Guangdong inventory declined again, mainly due to fewer arrivals and some manufacturers stockpiling ahead of the holiday... Macro front China: [NBS: January-March profits of China's above-scale industrial enterprises rose 15.5% YoY; non-ferrous sector profits surged 116.7% YoY] NBS data showed that from January to March, total profits of China's above-scale industrial enterprises reached 1.696 trillion yuan, up 15.5% YoY. From January to March, among above-scale industrial enterprises, state-controlled enterprises posted profits of 619.61 billion yuan (up 10.1% YoY), joint-stock enterprises 1.305 trillion yuan (up 20.9%), foreign-invested and Hong Kong, Macao, and Taiwan-invested enterprises 383.73 billion yuan (up 1.2%), and private enterprises 430.53 billion yuan (up 25.4%). Yu Weining, Chief Statistician of the Industrial Department of the National Bureau of Statistics (NBS), interpreted the industrial enterprise profit data for January–March 2026: In Q1, facing a complex economic environment, the CPC Central Committee and the State Council promptly stepped up macro regulation efforts and proactively implemented more active and effective macro policies. The industrial economy steadily rebounded, profits of above-designated-size industrial enterprises grew at a faster pace, profits in equipment manufacturing and high-tech manufacturing grew rapidly, profits in raw material manufacturing posted double-digit growth, and the efficiency of industrial enterprises continued to improve. [National Energy Administration: China's Oil and Gas Supply Was Generally Stable and Orderly in Q1] The National Energy Administration held a press conference on April 27 to brief on the national energy situation and development achievements in Q1 2026. Xing Yiteng, Deputy Director of the Development Planning Department of the National Energy Administration, noted that energy security was effectively safeguarded. The impacts of the Venezuela crisis and the US-Israel-Iran conflict on China's energy supply were properly managed. In Q1, China's oil and gas supply was generally stable and orderly, with above-designated-size industrial crude oil and natural gas production up 1.3% and 3.0% YoY, respectively. Raw coal production remained stable despite a relatively high base in the same period last year, with above-designated-size industrial raw coal production up 0.1% YoY. The safety situation in the power sector was stable and improving, with efficient completion of power emergency responses to various natural disasters and successful completion of power supply assurance for the Chinese New Year and the Two Sessions. (Jin10 Data) [PBOC Achieved a Net Withdrawal of 382 Billion Yuan via Reverse Repo Operations] The PBOC conducted 218.5 billion yuan of 7-day reverse repo operations today. As 600 billion yuan of 1-year MLF and 500 million yuan of 7-day reverse repo operations matured today, a net withdrawal of 382 billion yuan was achieved. (Jin10 Data APP) US dollar: As of 11:43, the US dollar index fell 0.08% to 98.42. Multiple sources revealed that the US Department of Justice was expected to conclude its criminal investigation into Fed Chairman Jerome Powell as early as Friday, thereby ending the standoff that could have delayed the appointment of Powell's successor. Sources said senior DOJ officials recently contacted several senators, including Republican Senator Tom Tillis, a member of the Senate Banking Committee, informing them of plans to drop the investigation into alleged cost overruns in the renovation of the US Fed's Washington headquarters and refer the matter to the Fed's internal watchdog. Powell's term is set to expire next month, but he indicated in March that he would remain in office until Trump's nominee for Fed Chairman, Kevin Warsh, is confirmed. According to the CME "Fed Watch" tool, the probability of the US Fed keeping interest rates unchanged in April was 100%. The probability of a cumulative 25-basis-point interest rate cut by June was 4.7%, while the probability of keeping rates unchanged was 95.3%. (Jin10 Data) Data: Germany's May GfK Consumer Confidence Index, the UK's April CBI Retail Sales Balance, and the US April Dallas Fed Business Activity Index are scheduled for release today. Crude oil: As of 11:43, oil prices in both markets rose, with WTI up 0.85% and Brent up 1.11%. Crude oil futures rose at the start of Monday's session as peace talks between the US and Iran reached an impasse, while oil shipments through the Strait of Hormuz remained limited, keeping global oil supply under sustained pressure. Crude oil futures prices swung wildly recently, as traders had to predict not only when oil exports from the Persian Gulf would resume, but also how long it would take for production in the region to recover to pre-war levels. Trump said on Sunday that Iran was facing growing domestic pressure due to its inability to export oil, which could cause long-term damage to its energy export infrastructure. Goldman Sachs analysts said on Sunday that they had pushed back their expectations for the Strait of Hormuz to return to normal export levels from mid-May to late June. Meanwhile, they raised their Q4 WTI crude oil price expectations from $75 per barrel to $83 per barrel. (Jin10 Data) Citi raised its forecast for the average Brent crude oil price for the remainder of 2026 on Sunday evening local time, stating that if oil shipments through the Strait of Hormuz continued to be disrupted through the end of June, oil prices could rise to $150 per barrel. The bank raised its base-case average price forecasts for Brent crude oil in Q2, Q3, and Q4 of 2026 to $110, $95, and $80 per barrel, respectively. Citi also pushed back its expectations for the reopening of the Strait of Hormuz from mid-to-late April to the end of May. Citi stated: "Given that significant gaps remain between the two sides on their respective red-line issues, we believe the risks are tilted toward the upside for near-term bullish sentiment and H2 2026 base-case oil price forecasts." In the bullish scenario (30% probability), Citi assumed that oil shipment disruptions would persist through the end of June at a scale similar to the current level of disruption. Under this scenario, Brent prices could surge to $150 per barrel, with Q2 and Q3 2026 averages approaching $130 per barrel, before pulling back to around $100 in Q4. The bank also proposed a "super bullish" scenario in which the Strait of Hormuz remained closed beyond June, noting that this would have severe implications for the share of oil expenditure in both global and US economic output. Spot Market Overview: ► ► ► ► ► ► ► ► ► ► ►

Apr 27, 2026 14:08 - US Dollar Fell for 9 Consecutive Days, Metals Rose Nearly Across the Board, SHFE Aluminum Up Nearly 3%, Lithium Carbonate Up Over 4% [SMM Daily Review]

SMM April 16: Metal market: As of the daytime close, domestic base metals generally rose, with SHFE tin being the only decliner, down 0.07%. SHFE aluminum led the gains with a 2.89% increase, while the rest of the metals gained less than 1%. The alumina front-month contract rose 1.44%, and the foundry aluminum front-month contract rose 1.62%. In addition, the lithium carbonate front-month contract rose 4.2%, polysilicon rose 1.08%, silicon metal rose 0.89%, and the Europe containerized freight front-month contract rose 4.75% to close at 2,044.7. Ferrous metals all posted gains to varying degrees except for stainless steel, which fell 0.03%. Iron ore rose 3.1%. Hot-rolled coil and rebar rose over 1%, with hot-rolled coil up 1.22% and rebar up 1.06%. Coking coal and coke side, coking coal rose 2.32% and coke rose 1.94%. Overseas market, as of 15:04, overseas base metals generally rose, with LME tin leading the gains at 1.41%, LME aluminum up 1.31%, and the rest of the metals gaining less than 1%. Precious metals, as of 15:04, COMEX gold rose 0.51% and COMEX silver rose 1.08%. In China, SHFE gold rose 0.17% and SHFE silver rose 1.43%. In addition, the platinum front-month contract rose 0.45%, and the palladium front-month contract fell 0.66%. Market data as of 15:04 today Macro Front China: [NBS: Q1 GDP Up 5% YoY! National Economy Off to a Good Start with Accelerating Industrial Production Growth] According to preliminary estimates by the NBS, Q1 GDP reached 33,419.3 billion yuan, up 5.0% YoY in real terms, accelerating by 0.5 percentage points from Q4 last year. By industry, the primary sector's value added was 1,194.1 billion yuan, up 3.8% YoY; the secondary sector's value added was 11,613.5 billion yuan, up 4.9%; and the tertiary sector's value added was 20,611.7 billion yuan, up 5.2%. On a QoQ basis, Q1 GDP grew 1.3%. In Q1, the value added of China's above-scale industrial enterprises rose 6.1% YoY, accelerating by 1.1 percentage points from Q4 last year. By three major categories, the value added of the mining industry rose 6.0% YoY, manufacturing rose 6.4%, and the production and supply of electricity, heat, gas, and water rose 4.3%. The value added of equipment manufacturing rose 8.9% YoY, and that of high-tech manufacturing rose 12.5%, outpacing the overall above-scale industrial value added by 2.8 and 6.4 percentage points, respectively. By economic type, value added of state-controlled enterprises increased 4.8% YoY; joint-stock enterprises rose 6.6%, foreign-funded enterprises and those with investment from Hong Kong, Macao, and Taiwan rose 3.9%; and private enterprises rose 6.1%. By product, production of 3D printing equipment, lithium-ion batteries, and industrial robots increased 54.0%, 40.8%, and 33.2% YoY, respectively. In March, value added of industrial enterprises above designated size increased 5.7% YoY and 0.28% MoM. In March, the manufacturing PMI was 50.4%, up 1.4 percentage points from the previous month; the enterprise production and business activity expectations index was 53.4%. In January–February, industrial enterprises above designated size nationwide recorded total profits of 1,024.6 billion yuan, up 15.2% YoY. [National Bureau of Statistics (NBS): China’s Imports and Exports Are Well Positioned to Maintain Solid Growth] Mao Shengyong, Deputy Director of the National Bureau of Statistics (NBS), said at a press conference held by the State Council Information Office that, based on years of practice, regardless of how the external environment changes, even during the pandemic when the market worried about whether China’s foreign trade could be sustained, China’s imports and exports have remained very strong. This was attributable to enterprises working hard to strengthen their fundamentals, enhance the technological content of products, and improve overall competitiveness. Overall, China’s imports and exports are still well positioned to maintain relatively solid growth. (Wallstreetcn) The PBOC conducted 500 million yuan of 7-day reverse repo operations in the open market, with the operation rate unchanged at 1.40%; 500 million yuan of reverse repos matured today. US dollar: As of 15:04, the US dollar index fell 0.05% to 98.03, marking a nine-session decline. Musalem of the US Fed said on Wednesday that high oil prices could push the underlying inflation rate for the remainder of this year to nearly one percentage point above the US Fed’s 2% target, and the US Fed may need to keep interest rates unchanged. Musalem said, “We are very likely to see some pass-through from oil prices to core inflation.” By the end of this year, the core measure of price increases would be “slightly below 3%, perhaps around 3%,” and there were risks of a further rise. Musalem said the US Fed may keep its policy rate in the current 3.50%–3.75% range “for some time,” while monitoring inflation, employment, and economic data in the coming months, and many of his colleagues shared the same view. The impact of last year’s tariff increases may gradually fade this quarter, and housing price inflation is also easing. As oil prices rise, inflation in a range of services has stayed high; if inflation begins to rise and could boost inflation expectations, he would be open to raising rates. Musalem also stated that the oil market is experiencing "the third negative supply shock in 12 months," which, combined with rising tariff rates and stricter immigration regulations, poses risks to both inflation prospects and the job market, potentially impacting economic growth. He predicted this year's economic growth would slow down but remain between 1.5% and 2%. (Jin10 Data APP) According to CME's "FedWatch," the probability of the US Fed raising interest rates by 25 basis points in April stands at 1.6%, while the likelihood of maintaining unchanged rates is 98.4%. For June, the probability of a cumulative 25-basis-point interest rate cut is 0%, with a 98% chance of unchanged rates and a 2% chance of a cumulative 25-basis-point hike. (Jin10 Data APP) On the macro front: Today, the UK will release February's three-month GDP monthly rate, manufacturing output monthly rate, seasonally adjusted goods trade balance, and industrial output monthly rate. The eurozone will announce March's final CPI annual and monthly rates. The US will report initial jobless claims for the week ending April 11, the Philadelphia Fed Manufacturing Index for April, and March's industrial output monthly rate. Additionally, key events include: US Fed Governor Bowman speaking at the IIF forum; the Fed releasing its Beige Book; Bank of England Governor Bailey discussing global economic imbalances during IMF meetings; China's NBS publishing the monthly report on residential property prices in 70 major cities; a State Council press conference on national economic performance; the ECB releasing March's monetary policy meeting minutes; FOMC permanent voter and New York Fed President Williams delivering remarks; US Fed Governor Milan speaking; and the G20 finance ministers and central bank governors meeting. Crude oil side: As of 15:04, oil prices showed mixed performance, with WTI down 0.06% and Brent up 0.2%. Market uncertainty persists over whether US-Iran peace talks will yield an agreement. Last week, US crude exports surged to near-record highs to meet demand from Asian and European buyers seeking alternatives to disrupted Middle Eastern supplies due to the Iran conflict. This brought the US close to becoming a net crude exporter for the first time since WWII. However, analysts and traders noted the US is rapidly approaching its export capacity limit. Government data released Wednesday showed net crude imports (exports minus imports) narrowed to 66,000 barrels per day, the lowest since weekly records began in 2001, while exports rose to 5.2 million barrels per day, a seven-month high. Annual data indicates the US last achieved net exporter status in 1943. Jin10 Data APP) Documents released by the White House show that US President Trump issued multiple oil pipeline permits on Wednesday, including one for a new pipeline aimed at facilitating the transportation of crude oil and petroleum products between the US and Canada. The construction permit has been granted to Bakken Pipeline for pipeline facility construction in Burke County, North Dakota. Additionally, he issued other permits for the maintenance and operation of existing pipelines near border areas in North Dakota and Michigan. (Jin10 Data APP) SMM Daily Review ► ► ► ► ► ► ► ► ► ► ►

Apr 16, 2026 18:42 - NBS: Q1 GDP Up 5% YoY! National Economy Off to a Good Start with Accelerating Industrial Production Growth

According to preliminary estimates by the National Bureau of Statistics (NBS), China's GDP in Q1 totaled 33,419.3 billion yuan, up 5.0% YoY in real terms, accelerating by 0.5 percentage points from Q4 of the previous year. By industry, the value added of the primary industry was 1,194.1 billion yuan, up 3.8% YoY; the value added of the secondary industry was 11,613.5 billion yuan, up 4.9%; and the value added of the tertiary industry was 20,611.7 billion yuan, up 5.2%. On a QoQ basis, GDP grew by 1.3% in Q1. The National Economy Achieved a Good Start in Q1 In Q1, under the strong leadership of the CPC Central Committee with Comrade Xi Jinping at its core, all regions and departments thoroughly implemented the decisions and plans of the CPC Central Committee and the State Council, stepped up the implementation of more proactive and effective macro policies, and worked to stabilize employment, enterprises, markets, and expectations. Efforts were accelerated to foster and develop new quality productive forces. Production and supply growth picked up, market demand continued to improve, the employment situation remained generally stable, market prices saw a mild rebound, high-quality development advanced toward new and better directions, the national economy achieved a good start, and development resilience and vitality were further demonstrated. According to preliminary estimates, China's GDP in Q1 totaled 33,419.3 billion yuan, up 5.0% YoY in real terms, accelerating by 0.5 percentage points from Q4 of the previous year. By industry, the value added of the primary industry was 1,194.1 billion yuan, up 3.8% YoY; the value added of the secondary industry was 11,613.5 billion yuan, up 4.9%; and the value added of the tertiary industry was 20,611.7 billion yuan, up 5.2%. On a QoQ basis, GDP grew by 1.3% in Q1. I. Agricultural Production Was in Good Shape, and the Livestock Industry Remained Generally Stable In Q1, the value added of agriculture (crop farming) grew 3.7% YoY. The sown area of winter wheat remained stable, seedling conditions continued to improve, and spring plowing and preparation progressed smoothly. According to the national planting intention survey, the intended sown area for grain this year remained generally stable, with the rice area basically flat and the corn area stable with a slight increase. In Q1, the production of pork, beef, mutton, and poultry totaled 26.62 million mt, up 4.8% YoY, of which pork and poultry production increased by 4.2% and 9.3% respectively, while beef and mutton production decreased by 1.4% and 2.0% respectively; milk production increased by 3.4%, and egg production decreased by 3.1%. In Q1, hog slaughter reached 200.26 million heads, up 2.8% YoY; the quarter-end hog inventory stood at 423.58 million heads, up 1.5%. II. Industrial Production Growth Accelerated, with Equipment Manufacturing and High-Tech Manufacturing Growing Rapidly In Q1, the value added of China's industrial enterprises above designated size grew 6.1% YoY, accelerating by 1.1 percentage points from Q4 of the previous year. By three major sectors, the value added of the mining industry grew 6.0% YoY, manufacturing grew 6.4%, and the production and supply of electricity, heat, gas, and water grew 4.3%. The value added of equipment manufacturing grew 8.9% YoY, and that of high-tech manufacturing grew 12.5%, outpacing the overall value added of industrial enterprises above designated size by 2.8 and 6.4 percentage points, respectively. By economic type, the value added of state-owned holding enterprises grew 4.8% YoY; joint-stock enterprises grew 6.6%, foreign-invested and Hong Kong, Macao, and Taiwan-invested enterprises grew 3.9%; and private enterprises grew 6.1%. By product, the production of 3D printing equipment, lithium-ion batteries, and industrial robots grew 54.0%, 40.8%, and 33.2% YoY, respectively. In March, the value added of industrial enterprises above designated size grew 5.7% YoY and up 0.28% MoM. In March, the manufacturing PMI stood at 50.4%, up 1.4 percentage points from the previous month; the expectations index for enterprise production and business activities was 53.4%. In January–February, the total profits of industrial enterprises above designated size nationwide reached 1,024.6 billion yuan, up 15.2% YoY. III. Services Sector Grew Rapidly, with Strong Momentum in Modern Services In Q1, the value added of the services sector grew 5.2% YoY. Among them, leasing and business services, information transmission, software and information technology services, financial services, transportation, warehousing and postal services, and accommodation and catering grew 12.2%, 10.6%, 6.5%, 4.3%, and 4.3%, respectively. In March, the national services sector production index grew 5.0% YoY. Among them, the production indices of information transmission, software and information technology services, leasing and business services, and financial services grew 11.8%, 10.1%, and 6.7%, respectively. In January–February, the operating revenue of services enterprises above designated size grew 7.4% YoY. In March, the business activity index for the services sector was 50.2%, up 0.5 percentage points from the previous month; the business activity expectations index for the services sector was 54.8%. Among them, the business activity indices of railway transportation, telecommunications, radio, television and satellite transmission services, monetary and financial services, and insurance were in the relatively high prosperity range above 55.0%. IV. Market Sales Picked Up, with Rapid Growth in Services Retail In Q1, total retail sales of consumer goods reached 12,769.5 billion yuan, up 2.4% YoY, accelerating by 0.7 percentage points from Q4 of the previous year. By location of business units, urban retail sales of consumer goods reached 11,057.4 billion yuan, up 2.3% YoY; rural retail sales of consumer goods reached 1,712.1 billion yuan, up 3.1%. By type of consumption, retail sales of goods reached 11,307.2 billion yuan, up 2.2%; catering revenue reached 1,462.3 billion yuan, up 4.2%. Sales of basic living necessities and some upgraded goods grew relatively fast. On a YoY basis, retail sales of grain, oil and food, garments, footwear, hats, knitwear and textiles, communication equipment, and gold, silver and jewelry by units above designated size increased by 10.0%, 9.3%, 20.8% and 12.6% respectively. In March, total retail sales of consumer goods were up 1.7% YoY and up 0.14% MoM. In Q1, retail sales of services were up 5.5% YoY, with the growth rate on par with the full year of the previous year. Among them, retail sales of communication and information services, tourism, consulting and rental services, and culture, sports and leisure services grew relatively fast. In Q1, national online retail sales of goods and services reached 4,977.4 billion yuan, up 8.0% YoY. Of this, online retail sales of goods reached 3,161.4 billion yuan, up 7.5%, accounting for 24.8% of total retail sales of consumer goods; online retail sales of services reached 1,816 billion yuan, up 8.8%. V. Fixed Asset Investment Grew Steadily, Infrastructure Investment Grew Relatively Fast In Q1, national fixed asset investment (excluding rural households) reached 10,270.8 billion yuan, up 1.7% YoY, compared with a decline of 3.8% for the full year of the previous year; excluding real estate development investment, national fixed asset investment grew by 4.8%. By sector, infrastructure investment was up 8.9% YoY, manufacturing investment was up 4.1%, and real estate development investment was down 11.2%. The floor space of commercial buildings sold nationwide was 195.25 million m², down 10.4% YoY; sales of newly-built commercial buildings totaled 1,726.2 billion yuan, down 16.7%. By industry, investment in the primary industry was up 15.9% YoY, investment in the secondary industry was up 5.8%, and investment in the tertiary industry was down 1.0%. Private investment was down 2.2% YoY, with the decline narrowing by 4.2 percentage points from the full year of the previous year; excluding real estate development investment, private investment grew by 1.3%. Investment in high-tech industries was up 7.4% YoY, of which investment in computer and office equipment manufacturing, aerospace and aircraft equipment manufacturing, and information services grew by 28.3%, 19.0% and 20.9% respectively. In March, fixed asset investment (excluding rural households) was up 0.52% MoM. VI. Trade in Goods Grew Rapidly, Trade Structure Continued to Optimize In Q1, total value of goods imports and exports reached 11,838 billion yuan, up 15.0% YoY. Of this, exports reached 6,846.7 billion yuan, up 11.9%; imports reached 4,991.3 billion yuan, up 19.6%. Ordinary Trade imports and exports were up 9.0% YoY. Imports and exports to countries participating in the Belt and Road Initiative grew by 14.2%. Imports and exports of private enterprises grew by 16.2%, accounting for 57.3% of total imports and exports. Exports of electromechanical products grew by 18.3%. In March, total imports and exports reached 4,104.6 billion yuan, up 9.2% YoY. VII. Consumer Price Increases Expanded, and Industrial Producer Prices Continued to Rebound In Q1, the national consumer price index (CPI) rose by 0.9% YoY, with the increase expanding by 0.4 percentage points from Q4 of the previous year. By category, prices of food, tobacco, alcohol and dining out rose by 0.5% YoY, clothing by 1.8%, housing fell by 0.2%, household goods and services rose by 2.3%, transportation and communication fell by 1.1%, education, culture and entertainment rose by 1.0%, healthcare rose by 1.8%, and other goods and services rose by 14.1%. Among food, tobacco, alcohol and dining out prices, pork prices fell by 11.3%, grain prices fell by 0.3%, fresh fruit prices rose by 4.3%, and fresh vegetable prices rose by 7.6%. Core CPI, excluding food and energy prices, rose by 1.2% YoY. In March, the national CPI rose by 1.0% YoY and fell by 0.7% MoM. In Q1, national ex-factory prices of industrial producers fell by 0.6% YoY, with the decline narrowing by 1.5 percentage points from Q4 of the previous year. Among them, March saw a YoY increase of 0.5%, compared with a decrease of 0.9% in the previous month; and a MoM increase of 1.0%. In Q1, the purchase prices of industrial producers nationwide fell by 0.5% YoY. Among them, March saw a YoY increase of 0.8%, compared with a decrease of 0.7% in the previous month; and a MoM increase of 1.2%. VIII. The Employment Situation Remained Generally Stable, with the Urban Surveyed Unemployment Rate Unchanged YoY In Q1, the average national urban surveyed unemployment rate was 5.3%, unchanged from the same period of the previous year. In March, the national urban surveyed unemployment rate was 5.4%. The surveyed unemployment rate for local household-registered labor force was 5.4%; the surveyed unemployment rate for non-local household-registered labor force was 5.3%, of which the surveyed unemployment rate for non-local labor force with agricultural household registration was 5.7%. The urban surveyed unemployment rate in 31 major cities was 5.3%. The average weekly working hours of employees in enterprises nationwide was 48.1 hours. At the end of Q1, the total number of rural migrant workers working outside their hometowns was 188.38 million, up 0.2% YoY. IX. Household Income Continued to Grow, with Rural Residents' Income Growing Faster Than That of Urban Residents In Q1, the national per capita disposable income was 12,782 yuan, a nominal increase of 4.9% YoY, or a real increase of 4.0% after deducting price factors. By place of permanent residence, the per capita disposable income of urban residents was 16,549 yuan, up 4.2% YoY in nominal terms and 3.2% in real terms; the per capita disposable income of rural residents was 7,433 yuan, up 6.1% YoY in nominal terms and 5.4% in real terms. By income source, the per capita nationwide wage income, net business income, net property income, and net transfer income grew 4.9%, 6.6%, 1.6%, and 5.1% in nominal terms, respectively. The median per capita disposable income of nationwide residents was 10,433 yuan, up 5.0% YoY in nominal terms. Overall, major macro indicators rebounded in Q1, new momentum grew rapidly, and the national economy achieved a good start. However, it should also be noted that the external environment has become more complex and volatile, the domestic imbalance of strong supply and weak demand remains prominent, and the foundation for economic improvement still needs to be consolidated. In the next phase, it is important to adhere to the guidance of Xi Jinping Thought on Socialism with Chinese Characteristics for a New Era, resolutely implement the decisions and plans of the CPC Central Committee and the State Council, fully and faithfully apply the new development philosophy, accelerate the construction of a new development paradigm, focus on promoting high-quality development, maintain the general principle of seeking progress while ensuring stability, implement more proactive and effective macro policies, continuously expand domestic demand and optimize supply, improve incremental resources and revitalize existing assets, and make efforts to stabilize employment, enterprises, markets, and expectations, so as to continuously consolidate and expand the steady and positive momentum of the economy. Recommended reading:

Apr 16, 2026 10:23 - NBS: Industrial Value Added of Enterprises Above Designated Size Grew 5.7% in March; Non-Ferrous Metal Smelting and Rolling Processing Industry Remained Flat YoY

According to NBS data, in March, the value added of industrial enterprises above designated size grew 5.7% YoY in real terms. On a MoM basis, the value added of industrial enterprises above designated size rose 0.28% from the previous month in March. From January to March, the value added of industrial enterprises above designated size was up 6.1% YoY. Value Added of Industrial Enterprises above Designated Size Up 5.7% in March 2026 In March, the value added of industrial enterprises above designated size grew 5.7% YoY in real terms (all value added growth rates are real growth rates after deducting price factors). On a MoM basis, the value added of industrial enterprises above designated size rose 0.28% from the previous month in March. From January to March, the value added of industrial enterprises above designated size was up 6.1% YoY. By three major sectors, in March, the value added of the mining sector grew 5.7% YoY, manufacturing grew 6.0%, and the production and supply of electricity, heat, gas and water grew 3.5%. By economic type, in March, the value added of state-holding enterprises grew 5.9% YoY; joint-stock enterprises grew 6.2%, foreign-invested and Hong Kong, Macao and Taiwan-invested enterprises grew 3.7%; and private enterprises grew 4.0%. By industry, in March, 30 out of 41 major industrial sectors maintained YoY growth in value added. Among them, coal mining and washing grew 5.3%, oil and natural gas extraction grew 9.4%, agricultural and sideline food processing grew 8.0%, liquor, beverage and refined tea manufacturing grew 2.4%, textile industry grew 1.7%, chemical raw material and chemical product manufacturing grew 9.0%, non-metallic minerals product manufacturing declined 5.5%, ferrous metals smelting and rolling processing grew 1.7%, non-ferrous metals smelting and rolling processing remained flat YoY, general equipment manufacturing grew 6.3%, special equipment manufacturing grew 6.2%, automobile manufacturing grew 7.5%, railway, shipbuilding, aerospace and other transportation equipment manufacturing grew 13.3%, electrical machinery and equipment manufacturing grew 5.4%, computer, communication and other electronic equipment manufacturing grew 12.5%, and electricity and heat production and supply grew 4.2%. By product, in March, 329 out of 626 products of industrial enterprises above designated size recorded YoY growth in production. Among them, steel products totaled 130.98 million mt, down 2.3% YoY; cement 123.1 million mt, down 21.0%; ten kinds of non-ferrous metals 7.07 million mt, up 2.2%; ethylene 3.64 million mt, up 6.8%; automobiles 3.067 million units, down 0.1%, of which NEVs 1.336 million units, up 1.2%; power generation 802.5 billion kWh, up 1.4%; crude oil processing volume 61.67 million mt, down 2.2%. In March, the product sales rate of industrial enterprises above designated size was 93.8%, up 0.7 percentage points YoY; the export delivery value of industrial enterprises above designated size reached 1,458 billion yuan, up 8.7% YoY in nominal terms.

Apr 16, 2026 10:20 - China's Steel Exports Stable, HRC Orders Improve, Prices at $480-485/mt

SMM Express: China's steel export prices remained stable today, with most shipments scheduled for May to June. Intraday market inquiries were active, and HRC order-taking also improved recently, with most deals concluded at $480-485/mt, while some transactions in North China were closed at $475/mt. Billet performance remained steady, while slab trading volume saw a significant increase, mostly concentrated among private enterprises.

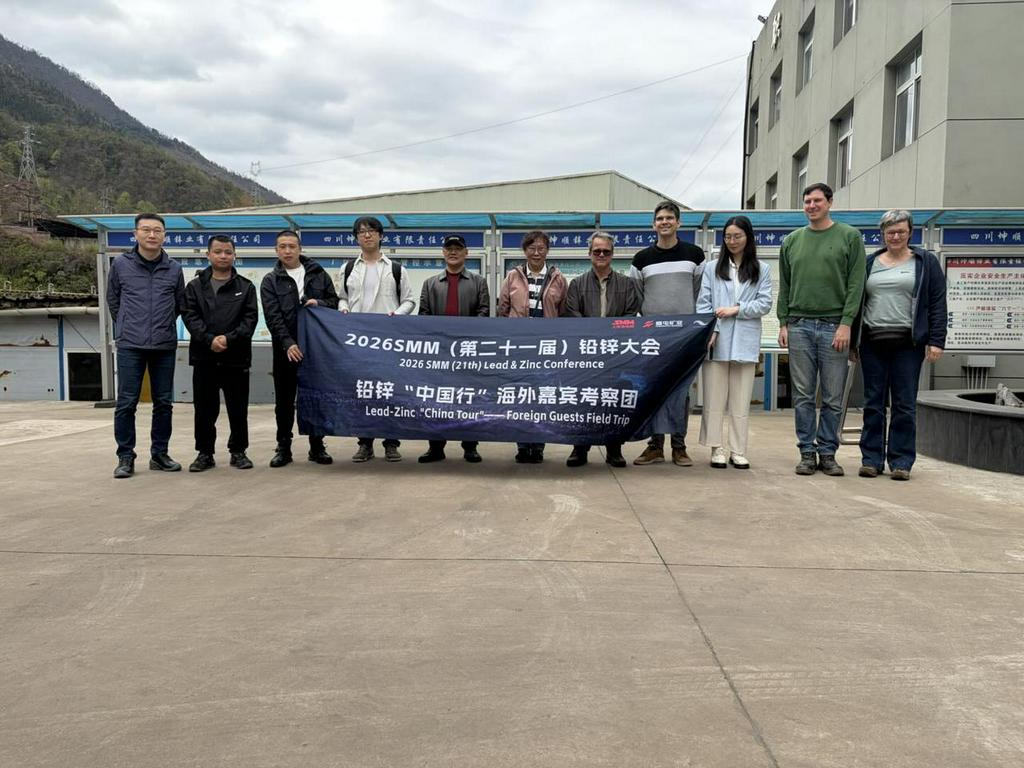

Apr 14, 2026 17:56  Post-Conference Tour: Connecting Global Lead-Zinc Giants with Key Chinese Players

Post-Conference Tour: Connecting Global Lead-Zinc Giants with Key Chinese PlayersThe 2026 SMM (21st) Lead & Zinc Conference and Industry Expo opened grandly at Howard Johnson Agile Plaza in Chengdu, Sichuan during March 25–27 2026. Organized by SMM, the event brought together global enterprises, professional experts and industry peers from across the entire lead and zinc supply chain. Participants focused on industry hot topics, analyzed market trends and explored development strategies, establishing a highly efficient platform for communication and collaboration to support high-quality growth of the sector. To further strengthen the overseas delegation’s comprehensive understanding of China’s lead and zinc industrial chain and build closer connections between international industry peers and key producers in China, SMM led a high-level overseas delegation on a multi-day industrial tour starting on the afternoon of March 27. The delegation included representatives from global giants, such as Nyrstar, a top European lead and zinc smelting firm, Nexa Resources, a South American giant in lead-zinc mining and smelting, and Befesa, a pioneer in zinc recycling. During the tour, the delegation visited 8 Chinese enterprises. including: COSCO Shipping Sichuan Chengtun Zinc & Germanium Technology Sichuan Kunshun Zinc Industry Yunnan Luoping Zinc & Electricity Hongzhou Hongqian Nonferrous Chemical Yunnan Zhenxing Industrial Group Mengzi Mining & Metallurgy Danxia Smelter of Shenzhen Zhongjin Lingnan Nonfemet The delegation members went deep into production sites, held in-depth discussions and exchanges, and gained a full picture of China’s lead and zinc industry in terms of production operations, technological innovation, capacity scale and market layout, greatly enhancing their insight into and understanding of the entire industrial chain. SMM has systematically compiled detailed information of all enterprises that were visited during this tour, with details below: COSCO Shipping On the afternoon of March 27, the delegation visited COSCO Shipping for an exchange, where they received a warm welcome from the company's leadership. Both sides engaged in discussions on topics such as equipment transportation and technological upgrades. Sichuan COSCO Shipping Logistics Supply Chain Management Co., Ltd. is a wholly-owned subsidiary of COSCO Shipping Logistics Supply Chain Co., Ltd., registered and established in Chengdu, Sichuan Province, with an investment of 30 million yuan. COSCO Shipping Logistics Supply Chain Co., Ltd. is affiliated with China COSCO Shipping Corporation Limited and serves as a core member of the "shipping, ports, and logistics" segment of COSCO Shipping Group, as well as an important component of its global digital supply chain system. The company operates warehouse space exceeding 6 million m², including 19 futures delivery warehouses. China COSCO Shipping Corporation Limited is a globally leading shipping enterprise group, with a combined fleet capacity of 130 million DWT across 1,535 vessels, ranking first in the world. Sichuan COSCO Shipping Logistics Supply Chain Management Co., Ltd. holds business qualifications and an operational scope covering multiple transportation modes including sea, land, air, and rail, providing comprehensive logistics services spanning both international and Chinese markets. Since entering the non-ferrous metals delivery warehouse business in 2016, the company has adhered to the principle of "client-centered and market-oriented," continuously enhancing its service capabilities and achieving steady business growth. Currently, at key logistics periods such as Shanghai Baoshan, Shanghai Yangshan, and Yixing in Jiangsu, the company successfully operates delivery warehouses designated by the Shanghai Futures Exchange for copper, nickel, zinc, and other products. It has become one of the three major non-ferrous metals warehouses of SHFE and was honored with the title of "Top Ten Designated Non-Ferrous Metals Delivery Warehouses" by the Shanghai Futures Exchange for two consecutive years. Sichuan Chengtun Zinc & Germanium Technology Co., Ltd. On March 28, the delegation visited Sichuan Chengtun Zinc & Germanium Technology Co., Ltd. (Shimian City). Both sides engaged in in-depth exchanges on the development of the zinc smelting industry, with a focus on thorough discussions regarding product processing, production techniques, capacity scale, market trends, and the current challenges facing the industry. Sichuan Chengtun Zinc & Germanium Technology Co., Ltd. was established on December 6, 2015, with a registered capital of 1.6 billion yuan. The company has an annual capacity of 300,000 mt of electrolytic zinc, 150,000 mt of sulphuric acid, 400,000 mt of electrolytic zinc waste residue processing, and 40 mt of high-purity germanium dioxide. On January 16, 2019, the company was approved by the China Securities Regulatory Commission and merged into the publicly listed firm Chengtun Mining Group Co., Ltd. The company's main business includes smelting and R&D of zinc-germanium series products, as well as comprehensive recovery of multiple metals. It has formed a complete industry chain from zinc concentrates entering the plant to finished products leaving the plant. Its production lines include zinc calcine, electrolytic zinc, electrolytic zinc waste residue processing, and comprehensive recovery of rare and precious metals. Sichuan Kunshun Zinc Industry Co., Ltd. (Shimian City) On March 28, the delegation headed to Sichuan Kunshun Zinc Industry Co., Ltd. (Shimian City) for a visit and exchange, where they received a warm reception from the enterprise. Both parties held in-depth discussions and exchanges on zinc smelting, covering topics such as production costs, production and market landscape, raw material procurement and processing, industry chain competitive advantages, and distinctive process technologies. Sichuan Kunshun Zinc Industry Co., Ltd. is a specialized and green environmental protection enterprise jointly invested and established by Sichuan Metallurgical Holding Group Co., Ltd. and Shimian Dongshun Zinc Industry Co., Ltd. to implement the national green production philosophy, actively develop the circular economy, and promote the comprehensive utilization of solid waste resources. It integrates solid waste treatment, recycling, and resource regeneration. The company primarily uses high-tech methods to carry out clean utilization and harmless treatment of heavy metal-containing waste generated by industries such as metallurgy and chemicals, eliminating the environmental impact of heavy metal solid waste at the source. The company was established in 2021 and is located in Zhuma Industrial Park, Shimian County, Ya'an City, Sichuan Province, covering an area of 65 mu with a total investment of 180 million yuan. The company has built a 3.5m × 50m Waelz rotary kiln production line, equipped with advanced and well-established low-grade zinc oxide production technology, achieving a resource recovery utilization rate of over 95% and effectively managing waste gas, noise, solid waste, and groundwater risks. It is also equipped with supporting facilities including desulphurization, denitrification, and flue gas defogging towers, as well as a wastewater treatment station, raw material warehouse, raw material pre-washing workshop, water slag processing workshop, biomass semi-gasification furnace, zinc crystallized salt workshop, production safety and environmental protection center, and laboratory for detection and testing. The company holds qualifications for treating hazardous waste categories including HW12, HW17, HW23, HW48, and HW49, with an annual capacity to process 100,000 mt of zinc-containing waste. Its main products include low-grade zinc oxide and zinc crystallized salt. The company has always upheld the green and environmentally friendly development philosophy, adhering to the fundamentals of "being responsible for the environment, for clients, and for employees," guided by technological innovation, and targeting the "reduction, recycling, and detoxification" of solid waste pollution prevention and control. The company is committed to building a modern "solid waste" management and disposal service provider, actively carrying out emergency environmental protection disposal, proactively assuming social service functions, and making positive contributions to promoting the circular economy development in Sichuan and strengthening the ecological civilization construction of lucid waters and lush mountains! Yunnan Luoping Zinc & Electricity Co., Ltd. (Qujing City) On March 30, the delegation visited Yunnan Luoping Zinc & Electricity Co., Ltd. (Qujing City) for exchanges. During the meeting, both sides conducted in-depth discussions on key topics including magnesium removal process optimization, production management organization, and raw material substitution plans, and put forward constructive suggestions on improving the plant environment. Yunnan Luoping Zinc & Electricity Co., Ltd. was established to fully leverage Luoping's local hydropower and lead-zinc mineral resource advantages. In accordance with the "ore, electricity, and smelting integration" development strategy proposed by the Luoping County Party Committee and County Government, and the overall requirements of the Municipal Party Committee and Municipal Government for the reform of industrial enterprises across the city, the company was registered and established at the Yunnan Provincial Administration for Industry and Commerce on December 21, 2000. It was listed on the Shenzhen Stock Exchange A-share market in 2007 and is a state-controlled enterprise under Luoping County. The company's assets are an optimized combination of three components: hydropower, lead-zinc mines, and zinc smelting. In terms of company assets, they are primarily composed of three advantageous resources of Luoping: mineral, hydropower, and zinc smelting. These mainly include six production units: Luoping County Fule Lead-Zinc Mine with an annual processing capacity of 100,000 mt of raw ore, Lazhuang Power Plant with annual power generation of 250 million kWh (installed capacity of 60,000 kW), a zinc smelter with an annual output of 120,000 mt of electrolytic zinc, a zinc powder plant with an annual output of 12,000 mt of ultra-fine zinc powder, a comprehensive utilization plant with an annual processing capacity of 129,500 mt of zinc slag, and a sulphuric acid plant with an annual output of 140,000 mt of sulphuric acid, achieving a total annual industrial output value exceeding 2 billion yuan. The company has six wholly-owned subsidiaries. The company's main businesses include hydropower generation, mining of lead, zinc, and other non-ferrous metals, as well as the production and sales of zinc smelting and its extended products. It is currently the only publicly listed firm in China's zinc smelting industry that integrates mining, power generation, chemical processing, and smelting. Its products include zinc sulphide concentrates, lead concentrates, zinc ingots, industrial sulphuric acid, ultra-fine zinc powder, cadmium, germanium concentrates, silver concentrates, copper concentrates, zinc alloys, industrial and residential electricity, edible oils and fats, among others. Its main product, "Jiulong" brand zinc ingots, is popular in non-ferrous product markets in and outside China thanks to its superior product quality and corporate reputation. Honghe Prefecture Hongqian Non-ferrous Chemical Joint-Stock Co., Ltd. On March 31, the delegation visited Honghe Prefecture Hongqian Non-ferrous Chemical Joint-Stock Co., Ltd. for exchanges. The two sides held in-depth discussions on topics including the economic benefits of smelting by-products, energy utilization efficiency, the current status of enterprise development, and future cooperation intentions. Honghe Prefecture Hongqian Non-ferrous Chemical Joint-Stock Co., Ltd. was established on August 1, 2007, with a registered capital of 50 million yuan. The total investment in project construction was 475.5543 million yuan. The company currently has over 600 employees and covers an area of 443 mu. The plant is located in the Heishenmiaobo Industrial Zone, situated in the central area of the Gejiu-Kaiyuan-Mengzi urban cluster. The company is a new-type joint-stock enterprise centered on crude lead smelting, integrating sulphur dioxide acid production, waste heat power generation, lead electrolysis, and recovery of precious and rare metals such as gold, silver, antimony, and bismuth, with further extension into deep processing of lead-series products including red lead, massicot, electrode plates, and storage batteries. It is a benchmark enterprise among private lead smelters in the city, featuring a relatively large scale, advanced technology, compliance with environmental protection standards, comprehensive utilization of resources, and a complete industry chain. The company pioneered the application of new technologies to upgrade and transform the traditional crude lead smelting model among private enterprises in the city. The company has formulated the working philosophy of "prioritizing environmental protection, ensuring safety, attracting talent, enforcing strict management, and enhancing efficiency," and continues to drive high-quality development. In April 2007, the company commissioned China ENFI Engineering Technology Co., Ltd. to conduct a feasibility study on the lead smelting technological transformation project, and determined a comprehensive industrial facility technological transformation project with a total investment of 490 million yuan and an annual capacity of 60,000 mt of crude lead. On December 21, 2009, the "Demonstration Project of Oxygen-Enriched Bottom-Blowing Lead Smelting Technology with Annual Output of 60,000 mt of Crude Lead" was designated by the Provincial Department of Science and Technology as a 2009 Yunnan Provincial Science and Technology Innovation Project. In 2010, it was further designated as a key industrial project by the provincial, prefectural, and municipal governments. On November 14, 2011, the company obtained ISO9001:2008 quality management system certification. On March 7, 2012, "HSPb99.94PCT" was successfully registered on the London Metal Exchange. In 2019, the company successively passed the safety completion acceptance and environmental impact assessment completion acceptance, fully achieving compliant operations and sustainable development. Yunnan Zhenxing Industrial Group Co., Ltd. On March 31, the delegation headed to Yunnan Zhenxing Industrial Group Co., Ltd. for a visit and exchange. Both parties conducted in-depth discussions on topics including Yunnan Province's mineral resource endowment, smelting industry development trends, corporate business strategies, and technological innovation applications, jointly assessing the current status and prospects of the industry and analyzing the challenges and opportunities ahead. Yunnan Zhenxing Industrial Group Co., Ltd. (hereinafter referred to as "the Group") was founded in 1996 and is located in the Chongposhao New Materials Industrial Park, Shadian Sub-district Office, Gejiu City. The Group currently has 7 subsidiaries, 2 holding companies, and 1 equity-participation company, with approximately 3,000 employees. Its capacity reaches annual output of crude lead (100,000 mt), electrolytic lead (60,000 mt), zinc ingot (20,000 mt), lead-acid battery plates (9 million sets), lead-acid batteries (6 million units), superphosphate (350,000 mt), sulphuric acid (200,000 mt), and monoammonium phosphate (MAP) (60,000 mt). The Group has established five major production sites and five major product brands covering crude lead raw material, lead-zinc smelting, power supply manufacturing, fertilizer and chemical production, and resource recovery. It has formed an internal industrial cycle spanning lead ore mining—lead-zinc smelting—lead-based alloy melting—battery manufacturing—waste battery recycling—precious metals production, making it one of the few private non-ferrous enterprises in China with a complete lead industry chain. Since 2013, the Group has been consecutively recognized as one of the Top 100 Non-Public Enterprises in Yunnan Province. In 2025, it ranked 41st among the "Top 100 Non-Public Enterprises in Yunnan Province" and was selected for the first time into the "Top 20 Private Enterprises in Innovation Capability," ranking 7th. Yunnan Shadian Lead Industry Co., Ltd., a subsidiary controlled by the Group, ranked 71st. The Group has received nearly 100 honors at various levels, including "High-tech Enterprise," "Outstanding Private Technology Enterprise," "Enterprise with Harmonious Labor Relations," "Provincial Model Collective for Ethnic Unity and Progress," and "Key Enterprise for Industrial Development in Honghe Prefecture" in Yunnan Province. The Group's Yunsha brand lead ingot was successfully registered on the London Metal Exchange in 2007 and on the Shanghai Futures Exchange in 2020. In 2021, the Group was rated AAA in enterprise credit rating in the national non-ferrous metals industry. In August 2024, it was designated as a "Qiangyuan Zhuqi" Industry-Finance Service Base by the Shanghai Futures Exchange. Looking ahead, the Group will pursue the philosophy of "seeking survival, pursuing development, and accelerating enterprise transformation and upgrading," adhering to the working approach of "rooting in Honghe, basing in Yunnan, radiating to surrounding regions, and expanding across China." It will thoroughly implement strategies of enterprise management transformation, technology-driven development, talent empowerment, and sustainable development, striving to achieve significant increases in capacity and production of major products by 2035, with gross industrial output value up YoY, and to build itself into a 10 billion green lead-zinc comprehensive recycling technology enterprise. Mengzi Mining and Metallurgy Co., Ltd. On March 31, SMM and the field trip delegation headed to Mengzi Mining and Metallurgy Co., Ltd. for a visit and exchange. Both parties engaged in in-depth discussions on the entire zinc smelting process, covering topics including production technology, raw material supply, product sales, environmental protection governance, and future development plans, aiming to share experience, address industry pain points, and jointly clarify the direction of development. Mengzi Mining and Metallurgy Co., Ltd. was established in 1996. It is a resource-based mining and metallurgy enterprise integrating R&D, exploration, mining, mineral processing, smelting, and trading, with a focus on comprehensive utilization of resources. The company is one of the few comprehensive private enterprises in the non-ferrous metal industry that possesses an entire industry chain and operates independent trading and supply chain business platforms. It is among the top 100 enterprises in Yunnan Province and a key enterprise in Honghe Prefecture. Shenzhen Zhongjin Lingnan Nonfemet Co., Ltd. — Danxia Smelter On April 2, the SMM delegation visited Zhongjin Lingnan's Danxia Smelter for a survey and field trip to the core plant area. In-depth discussions were held on production operations, technological R&D, and raw material procurement, covering key topics such as production capacity, technical cooperation, and raw material procurement strategies. Shenzhen Zhongjin Lingnan Nonfemet Co., Ltd. (hereinafter referred to as "Zhongjin Lingnan") was established in September 1984 and listed on the Shenzhen Stock Exchange in January 1997 (stock code: 000060). It is an internationalized entire industry chain resource company primarily engaged in lead, zinc, and copper mining, mineral processing, and smelting, as well as comprehensive recovery of rare, scattered, and precious metals. It is a publicly listed firm controlled by Guangsheng Holdings Group, a key wholly state-owned enterprise under Guangdong Province. Zhongjin Lingnan's business covers segments including mines, smelting, new materials, and supply chains. It has 23 directly affiliated enterprises, wholly-owned and controlled subsidiaries. Major operating entities include Fankou Lead-Zinc Mine, Shaoguan Smelter, Danxia Smelter, Zhongjin Copper Co., Guangxi Mining Co., Perilya Limited in Australia, Zhongjin Technology Co., and Huajiari Co. The company has an annual output of 300,000 mt of lead and zinc metal content in concentrates, 450,000 mt of smelted lead and zinc products, 450,000 mt of copper cathode, 21,000 mt of aluminum extrusion, 20,000 mt of battery zinc powder, and 5,400 mt of composite metal materials. Among these, its battery zinc powder ranked first in Chinese market share, nickel-metal hydride and nickel-cadmium battery electrode sheets & plates materials ranked first in Chinese market share, and thermal bimetal ranked first in Chinese market share. The 2026 field trip brought together some global lead and zinc industry leaders for an inspiring and highly productive journey across China’s leading smelters and enterprises. The warm welcome, operational excellence, and innovative technologies on display made this event a resounding success — and we extend our deepest gratitude to all the companies and participants who made it happen. Looking ahead – Save the date for 2027: We are excited to announce that the 2027 SMM (22nd) Lead & Zinc Conference and Industry EXPO will take place from March 17–19, 2027 in Kunming, Yunnan, China . This premier event will once again bring together the global lead-zinc community for high-level networking, insight sharing, and industrial exploration. Interactive call – We want to hear from you: As we plan the field trip for the 2027 conference, we’d love your input. Which smelters or companies would you most like to visit for technical exchange and on-site learning? Please share your suggestions in the comments below — your feedback will help shape the 2027 experience. Let us know where the industry should go next!

Apr 7, 2026 14:32- [SMM Hydrogen Energy Policy Update] National Energy Administration Holds Press Conference (on the National Energy Situation in 2025 and Other Matters)