46results found for 'Smelting Industry'

Sort by : |

Copper Concentrate TCs Break Through Negative Triple Digits: What Challenges Do Smelters Face?

Copper Concentrate TCs Break Through Negative Triple Digits: What Challenges Do Smelters Face?I. Market Status: Negative TCs Enter Triple Digits, Structural Tightening in Copper Concentrate Supply-Demand As global smelter capacity continues to climb, China, as the world's largest copper smelting country, faces a continuously declining self-sufficiency rate in copper concentrates and rising external dependency. Compounded by geopolitical crises, production cuts by ex-China miners, declining mine grades, and frequent production accidents, the copper industry has undergone a dramatic shift from "tight balance" to "structural deficit." Currently, the global copper concentrate market has fallen into a state of persistently tight supply. On May 15, the SMM Imported Copper Concentrate Index (weekly) reported -$102.84/dmt, breaking through the -$100/dmt threshold for the first time in history, setting a record negative depth. The payable indicator for 20%-grade domestic trade ore was 97.5%-98.5%, up 0.5 percentage points MoM. Supply-side factors driving TCs persistently lower continue to accumulate. 1) Full production resumptions at Freeport's Grasberg mine have fallen short of expectations. According to Freeport's Q1 earnings call, the company plans to achieve full production resumptions by the end of 2027; 2) The Peruvian government signed Emergency Decree No. 003-2026 on May 11, triggering widespread market concerns over the country's energy supply and copper mine output; 3) Geopolitical disruptions—the continued blockade of the Strait of Hormuz has driven sulfur prices persistently higher, pushing smelting acid prices to rise continuously. With smelting profits climbing, smelters' purchase willingness has increased, driving copper concentrate TCs persistently lower. Customs data showed that China's copper ore and concentrate imports in April 2026 were 2.352 million mt in physical content, down 19.57% YoY; cumulative imports from January to April were 9.915 million mt in physical content, down 0.8% compared to the same period last year. Since December 2020, China's copper concentrate cumulative imports had maintained positive YoY growth; this marks the first decline in over five years. II. Smelter Operating Rates Stay High Contrary to the intuition of "industry-wide losses" implied by deeply negative TCs, operating rates at China's copper smelters have not experienced a cliff-like decline. From a pure smelting perspective, operating willingness and actual profitability across different types of enterprises show significant divergence. Under the extreme environment of deeply negative TCs, the core reason China's copper smelters can maintain relatively resilient operations is that by-product revenues are becoming the key variable determining break-even. Meanwhile, China's copper cathode production declined MoM due to the maintenance peak. SMM data showed that China's copper cathode production in April fell 2.26% MoM. Cumulative copper cathode production from January to April 2026 reached 4.7067 million mt. However, according to SMM, some smelters postponed their maintenance plans or completed crude smelting maintenance ahead of schedule to capture revenue from the by-product sulphuric acid. III. Breakdown of Smelter Profit Sources (i) Sulphuric Acid: The Strongest Profit Contributor at the Current Stage Sulphuric acid is currently the most important by-product profit source for smelters. In pyrometallurgy-based copper cathode production, approximately 3-4 mt of sulphuric acid is produced as a by-product for every 1 mt of copper cathode. As of May 15, the SMM China Copper Smelting Acid Index stood at 1,665 yuan/mt, up 83.7% from the beginning of the year. Sulphuric acid prices currently stay high, meaning sulphuric acid revenue can offset a considerable portion of the revenue loss caused by negative TCs. However, this "sulphuric acid moat" is facing policy challenges. China suspended exports of ordinary industrial sulphuric acid and smelting by-product sulphuric acid starting in May for a period of 8 months. The export ban is not intended to suppress domestic sulphuric acid prices, but rather to prioritize domestic supply for agricultural phosphate fertiliser production and strategic industries such as new energy. Demand side, overall sulphuric acid demand remains tight. Although downstream sectors including phosphate fertiliser, titanium dioxide, and new energy materials saw declining operating rates due to high-priced raw materials, just-in-time procurement still exists. Meanwhile, the supply side is also constrained by concentrated smelter maintenance and high sulphur-based acid production costs, with industry-wide capacity utilization rates at low levels. Cost side, firm sulphur prices provide bottom support for sulphuric acid; supply side, concentrated maintenance limits downside room; demand side, although weak, has not yet formed a substantial enough impact to break down high prices. This means sulphuric acid continues to serve as a profit pillar for smelters. (ii) Precious Metal Recovery: "Incremental Game" Under High Copper Prices In addition, copper concentrates typically contain associated precious metals such as gold and silver, which can be recovered through anode slime processing during smelting. Copper prices are currently at historically high levels, and gold prices also fluctuate at highs, greatly enhancing the economics of precious metal recovery. According to SMM market sources, when gold and silver prices are at high levels, raw materials with impurities rich in gold and silver are assigned extremely high added value. The profit contribution of precious metal recovery to smelters is reflected in: smelters can achieve recovery utilization rates exceeding the gold and silver payable indicators through refined processing, profiting from spot smelting revenue. This portion of revenue is often a significant component of smelters' comprehensive profit structure. However, as gold and silver prices continue to rise, suppliers in the copper concentrates spot trade are simultaneously raising gold and silver payable indicators. The continuously rising precious metal payable indicators and payable benchmark pose an increasingly severe challenge to smelter profitability. IV. Future Trends: Coexistence of Industry Landscape Evolution and Technology Upgrade Requirements However, industry chain profits are irreversibly shifting toward the upstream ore side. Under the medium and long-term landscape of persistently tightening copper concentrates supply and demand, the scarcity value of the resource side is being reassessed by the market. As the copper concentrates supply-demand gap persists over the medium and long-term horizon, and smelters' bargaining power will remain under pressure over the long term. The market is widely concerned about whether TC can quickly pull back in tandem once the continuously rising sulphuric acid prices reach a turning point. Facing the long-term trend of profit squeeze at the mine end and losses in the smelting segment, the future landscape of the copper smelting industry will evolve in the following directions: Direction 1: Integrated consolidation extending upstream. Enterprises with upstream mine assets will have a significant advantage in profitability. Direction 2: Technological upgrades to achieve differentiated competition. Against the backdrop of narrowing profit margins from non-payable metals, the technological barriers of smelters will become increasingly important. Those who can more efficiently extract valuable metals from low-grade ore or complex ore will seize the initiative in the industry reshuffle. Under the extreme environment of persistently negative TCs, sulphuric acid by-product revenue and precious metal recovery are the core profit pillars currently sustaining smelter operations. The supply-demand pattern dictates that the pricing power and profit margins at the mine end will continue to outperform those at the smelting end. The copper smelting industry is transitioning from the traditional model of "earning TCs" to a new competitive landscape of "resource control + technological barriers + integrated operations."

May 19, 2026 15:48- Gansu Changba Nonferrous Metals Co., Ltd. Looks Forward to Meeting You at the 2026 SMM Zinc Industry Conference

The year 2026 marks the opening year of the "15th Five-Year Plan" period. Against the backdrop of intensifying global macro volatility and the deepening advancement of high-quality development in China, the zinc industry is undergoing profound transformation: tightness on the ore side and the release of smelting capacity are creating structural tension, divergence between domestic and overseas inventories reflects the complex dynamics of supply-demand rebalancing, and technological innovation is becoming the key momentum for resolving contradictions and reshaping the landscape. Key areas under the "15th Five-Year Plan" such as new energy and new-type infrastructure are injecting new momentum into traditional zinc consumption, while green, low-carbon, and circular economy principles are accelerating the restructuring of industrial logic driven by technological innovation. With the joint support of upstream and downstream enterprises in the zinc industry, industry associations, and relevant parties, SMM is about to hold the 2026 SMM Zinc Industry Conference & the 8th Hot-Dip Galvanizing Industry Development and Technological Innovation Forum & the 14th Zinc Salt, Zinc Oxide and Zinc Secondary Resources Development Forum & the Zinc-Based Materials Development Forum on August 6-8 in Qingdao, Shandong. Themed "Converging Zinc Momentum · Building Zinc Industry · Embarking on a New Journey," the conference is driven by the dual engines of macro perspectives and fundamental analysis, closely aligned with the "15th Five-Year Plan" high-quality development mainline, focusing on four major dimensions: macro policies, supply-demand patterns, global trade, and technological innovation. It aims to drive cost reduction and efficiency improvement through technological breakthroughs, respond to market fluctuations through collaborative innovation, and jointly chart a new blueprint for high-quality and sustainable development of the zinc industry. Gansu Changba Nonferrous Metals Co., Ltd. will attend this grand event, discussing industry development trends with industry peers and jointly driving the zinc industry to new heights. Click the to register now, witness and participate in this significant and far-reaching industry event, and co-create a glorious new chapter! ◆ Company Overview ◆ Gansu Changba Nonferrous Metals Co., Ltd. is a subsidiary of Baiyin Nonferrous Group Co., Ltd., with Chengzhou Zinc Smelter and Changba Lead-Zinc Mine under its management. It is a large state-owned nonferrous metals enterprise integrating lead-zinc mining, mineral processing, smelting, and scientific research. Chengzhou Zinc Smelter currently has an annual electrolytic zinc production capacity of 100,000 mt. It is a modern smelter integrating zinc metal smelting, comprehensive utilization of resources, and R&D of new nonferrous metal smelting processes. The enterprise adheres to the development direction of "lean collaboration, digital integration, and green leadership," closely aligned with the goal of creating the ultimate quality benchmark. It has continuously made breakthroughs in improving zinc smelting quality. In 2026, the first batch of high-purity zinc ingots with a purity of 99.998% was successfully produced, injecting solid momentum into further enhancing the enterprise's core competitiveness, expanding the high-end zinc materials market, and driving high-quality development of the enterprise. The Chengzhou Zinc Smelter has always adhered to the pursuit of excellence and perfection. With the successful production of 99.998% high-purity zinc ingots as a major breakthrough, the smelter has continued to increase investment in scientific research, actively introduced advanced and applicable production technologies and equipment, focused on building a high-caliber professional and technical talent team, continuously optimized the production process for 99.997% high-purity zinc ingots, and steadily carried out technical research on even higher-purity zinc products. ◆ Honors Bestowed: Quality Certified by Authoritative Bodies ◆ The outstanding quality of the 99.998% high-purity zinc ingots has been widely recognized by authoritative institutions both within and outside the industry, with numerous prestigious awards attesting to their quality excellence: · Technology Innovation Awards: Leveraging core technological breakthroughs such as "Research and Application of Low-Impurity Electrolytic Zinc Standard Creation," the smelter won the "Second Prize of Nonferrous Metals Industry Science and Technology Award," the "First Prize of Gansu Province Science and Technology Progress Award," and the "Grand Prize of Science and Technology of CITIC Guoan Group Co., Ltd.," with its technical capabilities recognized at national, provincial, and municipal/county levels. The "R&D and Application of High-Grade Zinc Ingot Preparation Process Technology" won a Bronze Award at the 11th International Invention Exhibition "Belt and Road" and BRICS Skills Development and Technological Innovation Competition. "Full-Process Lean Management Control for Creating Excellent Zinc Ingot Quality" won the Second Prize of the 2025 Nonferrous Metals Enterprise Management Modernization Innovation Achievement Award. The smelter built Nanshi's first 5G+ digital workshop, deployed industrial robots and unmanned AGV systems, achieved full-process automation of ingot production, and improved production efficiency by 30%. · Product Quality Awards: The main product, zinc ingots (including the 99.997% grade), together with the by-product sulphuric acid, were awarded the highest honor in nonferrous metals product physical quality certification — the "Gold Cup Award," serving as an authoritative endorsement of their quality stability and superiority by the industry. In 2025, the smelter was recognized as a "Premium Brand" by the CNIA. · Market Access Certification: The main product, zinc ingots, was successfully registered on the Shanghai Stock Exchange, obtaining standardized market circulation qualifications. The brand value reached 2.482 billion yuan, ranking 31st nationwide among "Product Brands," laying a solid foundation for the market promotion of 99.997% high-purity zinc ingots. ◆ Diverse Applications: Empowering High-End Industrial Development ◆ Due to its extremely low impurity content and excellent chemical stability, the 99.998% high-purity zinc ingot demonstrates irreplaceable application value in multiple high-end fields: · High-End Electronics: As a core raw material for electronic component coatings, its low-impurity characteristics effectively enhance the conductivity and service life of electronic devices, and it is widely used in the production of precision electronic components such as integrated circuits and smartphone chips. · Aerospace: Used in anti-corrosion coatings for aerospace components and lightweight alloy material manufacturing, its stable physicochemical properties can adapt to extreme environments, ensuring the reliability of aerospace equipment. · Pharmaceutical and Chemical Industry: Serving as raw materials for pharmaceutical intermediates and high-end catalysts, its high-purity characteristics ensure product safety and efficacy, meeting the stringent standards of the pharmaceutical and chemical industry. · New Energy: In the production of new energy products such as zinc-based batteries and energy storage equipment, high-purity zinc ingots can enhance battery energy density and cycle life, facilitating the upgrading of the new energy industry. ◆ Outstanding Performance: Market Recognition Demonstrates Strength ◆ With a zinc ingot capacity of 100,000 mt, the 99.998% high-purity zinc ingots, leveraging core advantages of low lead, low iron, and low cadmium, received strong recognition from downstream clients upon market launch, delivering impressive market results: · Industry-Leading Zinc Ingot Quality: Zinc ingot purity reaches 99.998%, with lead content at 0.0009%, iron content stable at 0.0003%, and cadmium, tin, and aluminum consistently maintained at 0.0002%, placing it at a leading level in the ISP zinc smelting industry. · Extensive Market Coverage: Products were rapidly sold to core markets such as Shanghai and Xuzhou, covering multiple sectors including high-end electronics and precision manufacturing, breaking the supply bottleneck of high-end high-purity zinc ingots. · Leading Client Satisfaction: With stable purity, extremely low impurity content, and reliable supply capability, a stable client base and strong market reputation have been established. Client satisfaction in 2025 reached 100%. ◆ Future Outlook: Continuously Leading High-Quality Development ◆ Chengzhou Zinc Smelter consistently adheres to the pursuit of excellence and perfection. Taking the successful production of 99.998% high-purity zinc ingots as a significant breakthrough, it continues to increase R&D investment, actively introduces advanced and applicable production technologies and equipment, focuses on building a high-caliber professional technical talent team, and continuously optimizes the production process for 99.997% high-purity zinc ingots while steadily advancing technical breakthroughs for even higher-purity zinc products. Meanwhile, it deepens industry-academia-research collaborative innovation, expands application scenarios of high-purity zinc in high-end manufacturing, new materials, and other fields, and promotes coordinated improvement and synergistic development across the upstream and downstream of the industry chain. The enterprise is anchored on the goal of building an industry-leading lean benchmark enterprise, continuously strengthening whole-process quality management, deepening green and low-carbon production, accelerating intelligent transformation and upgrading, and driving enterprise quality improvement, efficiency enhancement, and transformation with solid achievements, contributing tangible "Chengye Strength" to the high-quality development of the zinc smelting industry. ◆ Contact Information ◆ Long press to scan the code and register now 2026 SMM Zinc Industry Conference

May 15, 2026 11:47 - [SMM Analysis] Sulphuric Acid: A Key Variable Reshaping Copper Pricing Logic

[SMM Analysis] Sulphuric Acid: A Key Variable Reshaping Copper Pricing Logic

May 8, 2026 18:24 - Wuzhongda Reports 32.59% Revenue Growth in Magnesium-Aluminum New Materials in 2025

[SMM Magnesium Express] On April 28, Wuzhongda Group Joint Stock Company (Wuzhongda) released its 2025 annual report. The report revealed that in the processing of magnesium-aluminum new materials, the full industrial chain layout has achieved positive results. In 2025, this segment achieved operating revenue of 2.787 billion yuan, with a year-on-year increase of 32.59%; total profit reached 222 million yuan, with a year-on-year increase of 66.92%. The report also disclosed that by the end of 2025, its subsidiary Qixin Alloy Materials Co., Ltd. had a primary magnesium production capacity of 73,000 tons, and it is expected that the production capacity will exceed 100,000 tons by the end of 2026, further consolidating its leading position in the primary magnesium smelting industry.

Apr 30, 2026 18:26 - Sulphuric Acid Prices Key to Copper Smelter Cutbacks Amid Collapsing TCs

On April 24, the SMM Imported Copper Concentrate Index (weekly) stood at -81.44 USD/dmt, down 2.83 USD/dmt from the previous reading of -78.61 USD/dmt. The deeply negative TC reflects the tightness in the global copper concentrate market, which has already shifted from market expectations to an actual rigid contraction in supply. In the first quarter of 2026, the world's leading mining companies frequently revised down their production guidance, with supply-side disruptions far exceeding early-year forecasts. Freeport significantly lowered its full-year 2026 copper production forecast from 1.542 million tonnes to approximately 1.406 million tonnes, with an expected recovery rate of only 65%, due to slower-than-expected mine recovery at its Grasberg site in Indonesia, affected by mudslides and ore moisture. In addition, road blockades caused by strikes at BHP's Escondida and Zaldivar mines have led to actual production impacts that remain to be monitored. According to SMM exclusive data, the global copper concentrate deficit in 2026 is estimated at 317,000 metal tonnes, a situation that may ease somewhat in 2029. In stark contrast to the persistently falling TC, domestic smelter operating rates remained high in Q1 2026. According to SMM data, China's electrolytic copper output in March 2026 reached 1.2061 million tonnes, up 5.58% month-on-month and 7.49% year-on-year. In Q1 2026, total electrolytic copper output was 3.5278 million tonnes, up 4.60% quarter-on-quarter and 10.45% year-on-year. SMM survey data shows that 11 smelters have confirmed maintenance schedules for Q2 2026. This means that domestic electrolytic copper output is expected to decline in Q2, with spot supplies likely tightening temporarily in May and June. However, some smelters have reported that due to high sulfuric acid prices, maintenance completion times may be brought forward. Sulfuric acid is currently the most important by-product revenue source for the copper smelting industry. According to SMM data, on April 24, 2026, China's copper smelting acid index stood at 1,660.5 RMB/ton, up 31.5 RMB/ton from the previous period. As sulfuric acid revenues have risen steadily from 890 RMB/ton at the start of 2026 to 1,660.5 RMB/ton in April 2026, based on the co-production of 3–4.5 tonnes of sulfuric acid per tonne of electrolytic copper, sulfuric acid income can now cover the copper concentrate procurement cost and part of the processing cost for smelters. The upward slope and magnitude of this increase exceed the deterioration in spot TC. The substantial boost in sulfuric acid profitability allows smelters to tolerate lower TC, creating a cycle of "higher sulfuric acid prices, lower TC." Meanwhile, rising gold and silver prices have further expanded smelters' comprehensive profit margins. Although the copper smelting segment is deeply loss-making, driven by the hefty profits from sulfuric acid, gold, and silver, domestic copper smelters have been able to maintain high operating rates without large-scale production cuts caused by deeply negative TC. Additionally, about 20% of the world's electrolytic copper comes from hydrometallurgical processes, with the DRC and Chile together accounting for nearly 80% of that. Hydrometallurgical copper production consumes large amounts of sulfuric acid, and sulfur is a key raw material for sulfuric acid. The current disruption in the Strait of Hormuz has cut off approximately 50–60% of Middle Eastern sulfur shipments by sea, pushing up sulfur and sulfuric acid prices. Worth noting is that as late April 2026 progresses, sulfuric acid export restrictions combined with increased domestic production have shown signs of price softening. If sulfuric acid prices continue to decline, it will directly squeeze the comprehensive profit margins of domestic smelters. At that point, the dual pressure of persistently low TC and falling sulfuric acid prices could trigger real production cuts on the smelting side. Although gold and silver prices do not directly determine TC trends, their macro-pricing logic as part of the non-ferrous metals sector is worth attention. The market has largely priced in the expectation that the Federal Reserve will not cut interest rates at all in 2026, with the first rate cut possibly delayed until July 2027. For copper, a delayed rate cut means no near-term easing of macro liquidity, but copper's core pricing logic remains the ongoing tug-of-war between tightening supply on the mining side and rigid demand. In other words, precious metals are under pressure, but industrial metals' pricing center remains in real supply-demand fundamentals, which explains why weaker gold and silver prices have not dragged copper prices lower. According to SMM, for Chinese smelters, domestic copper concentrate spot TC transactions are feasible in the range of -81 USD/dmt to -88 USD/dmt. Some holders have attempted to offer TC at -100 USD/dmt, while some smelters are willing to accept deliveries at the lower end around -90 USD/dmt. The downward trend in TC has not yet stopped, and smelter purchasing activity may have weakened slightly, but not significantly. Key areas to watch moving forward: Sulfuric acid side: The price trend will depend on the interplay of multiple factors. First, China's sulfuric acid export policy direction: if export restrictions continue, domestic sulfuric acid supply will be relatively abundant, and prices may fall from highs; if exports are temporarily allowed, overseas hydrometallurgical copper supply risks will rise, but domestic sulfuric acid prices may find support. Second, the recovery of sulfur supply: when shipping through the Strait of Hormuz returns to normal will directly affect the pace at which Middle Eastern sulfur can supplement global markets. Third, seasonal demand changes for downstream products such as phosphate fertilizers will also cause periodic price volatility for sulfuric acid. Mining side: Focus on the progress of the Grasberg conversion project, labor negotiation results at Chilean mines, and logistics stability at mines such as Las Bambas in Peru. Any new supply release will effectively ease TC pressure. Macro side: Monitor the Federal Reserve's monetary policy path, the U.S. dollar index, the actual driving effect of China's pro-growth policies on copper consumption, and whether the growth rate of copper demand in global new energy sectors is slowing marginally.

Apr 29, 2026 19:51 - SMM Visits Chambishi Copper Smelter, Both Parties Engage in In-Depth Discussion on Current Status and Future Development of Copper Industry Chain

On April 14, a delegation from SMM Information & Technology Co., Ltd. (SMM), including Ye Jianhua, Director and Supervisor of SMM's Industry Research Department, Feng Chundi, Expert at SMM's Industry Research Institute, and Wu Tao, SMM's Copper and Tin Overseas Marketing Manager, visited Chambishi Copper Smelter Limited (CCS) for exchange and survey. The delegation received warm hospitality from CCS's leadership. During the visit, both parties engaged in pragmatic communication based on their respective core businesses. Leveraging its core strengths in non-ferrous metal price index R&D, industry chain big data monitoring, copper market analysis and forecasting, in-depth industry research, and global non-ferrous resource connectivity, SMM shared insights on international copper market operating logic and price trend analysis with the enterprise, in the context of the current global copper smelting supply-demand pattern, raw material procurement landscape, and TC fluctuation trends. As a core copper smelting producer outside China, CCS provided a detailed introduction to its production and operation status, smelting process advantages, capacity release pace, raw material procurement, and product exports layout, and elaborated on the practical experience of ex-China copper smelters in production management, cost control, green production, and localized operations. Meanwhile, both parties exchanged views on common industry topics including development pain points of the copper smelting industry outside China, raw material supply security, finished product circulation and trade, industry policy changes, and low-carbon smelting development trends. They also reached preliminary consensus on future directions such as industry chain information sharing, market data exchange, joint market analysis, and industry resource coordination, laying a solid foundation for deepening regular exchanges and promoting high-quality collaborative development of the copper smelting industry chain. Introduction to Chambishi Copper Smelter Limited (CCS) Chambishi Copper Smelter Limited (CCS) is the first large-scale modern pyrometallurgy copper smelting enterprise invested by China overseas, entirely self-designed and constructed. Located in the Zambia-China Economic and Trade Cooperation Zone, the company has 170 Chinese staff and 1,600 Zambian employees. The company has always focused on its vision of "building an internationally first-class smelting enterprise with enduring prosperity," upheld the corporate spirit of "self-transcendence, continuous breakthroughs, and pursuit of excellence," benchmarked against first-class standards with meticulous craftsmanship, and continuously strengthened and optimized enterprise management, with its comprehensive competitiveness steadily improving. As of the end of 2024, the company had produced over 3.3 million mt of copper products and 8.7 million mt of sulphuric acid, with cumulative sales revenue of approximately $21 billion, effectively driving local economic development in Zambia and becoming a shining pearl along the Belt and Road! Enterprise History and Development Achievements (Pursuing Excellence, Benchmarking Against the Best and Forging Ahead) To extend the industry chain and retain more added value locally, in 2006, China Nonferrous Metal Mining (Group) Co., Ltd. cooperated with Yunnan Copper to introduce the advanced ISA copper smelting process to Zambia, with shareholding ratios of 60% and 40% respectively. From the design stage, the Company drew on successful experience in China and incorporated the characteristics of Zambian raw materials to re-optimize and re-innovate the key processes and technologies of the ISASMELT process, strengthening system integration. This resulted in multiple innovative achievements, including "Integration Innovation and Application of ISASMELT Furnace" and "Comprehensive Automated Control System," which were awarded the First Prize for Scientific and Technological Progress by China Nonferrous Metals Industry Association (CNIA) in 2010. The ISASMELT furnace campaign life broke world records multiple times, with the second campaign reaching 218 weeks and the third campaign reaching 244 weeks, establishing an international benchmark. In 2021 and 2022, the Company's copper production exceeded the designed capacity of 250,000 mt for two consecutive years, making history. In 2024, production further surpassed 260,000 mt, setting a new historical record. In September 2013, the Company was honored with the title of Advanced Collective of Central State-Owned Enterprises. In July 2021, it was successfully selected as a Benchmarking Enterprise under the administration of the State-owned Assets Supervision and Administration Commission of the State Council (SASAC). Process Flow (Dedicated and Professional, Striving for Excellence to Drive Development) The Company adopts the internationally advanced and mature process of "oxygen-enriched top-blown submerged bath smelting, electric furnace settling and separation, PS converter blowing, and anode furnace pyrometallurgy refining" to produce copper anode, and employs the "double-conversion double-absorption" process to produce sulphuric acid. Adhering to the concept of sustainable development, the Company has built a slag flotation recovery system with a daily processing capacity of 1,500 mt of furnace slag, and a bismuth recovery system with a daily processing capacity of 6 mt of flue dust, continuing to recover metals such as copper, cobalt, and bismuth from smelting slag and flue dust. Social Responsibility (Cooperation and Sharing, Giving Back to Society with Strong Responsibility) The Company actively practices its core values of "Dedication, Cooperation, and Sharing," consistently focusing on its core business of copper pyrometallurgy smelting, engaging in extensive cooperation with upstream and downstream clients, and sharing development achievements with employees and local communities. Since its establishment, the Company has cumulatively paid over $300 million in various taxes and fees in Zambia, created over 5,000 employment opportunities, and cooperated with more than 300 local suppliers, contributing to Zambia's green, harmonious, and shared development. The Company actively fulfills its social responsibilities by increasing investment in social welfare programs for local communities in Zambia, covering infrastructure, education, healthcare, and sanitation. These efforts include sponsoring the renovation of clinics in Kalulushi, supporting the Bushifire Orphanage, donating the construction of classrooms at Buyantashi School, Luato Market, Kankuko Bridge, Chibuluma Community Tennis Court, Chimfunshi Chimpanzee Rescue Center, and Modern Stars Football Club, among others. With a cumulative investment of over $4 million, the Company has earned high praise from local government and warm welcome from the public, establishing a strong corporate image. The Company actively promotes employee localization and continuously achieves skills transfer. The company invested over 5 million Kwacha, and externally carried out technical and non-technical training programs in electric welding, electrical power, pneumatics, technical control, management supervision, and equipment maintenance through the China-Zambia Vocational and Technical College, the TEVETA Fund, and other channels. Internally, through mentorship programs and other approaches, the company conducted business training in masonry, fitting, and other skills. The localization rate of the company's employees reached over 92%, the skills of local employees were significantly enhanced, and technical expertise was exported to the DRC. Vision and Outlook (Staying True to Our Original Aspiration, Building Tomorrow with a Shared Destiny) Innovation-driven development knows no bounds. Over the past decade and more, the company has upheld a sense of survival crisis and market competition awareness, adhered to innovation-driven development, and achieved high-quality growth. In 2021, the company's information technology infrastructure was completed and successfully put into use, with a commitment to building an automated, digitalized, and intelligent factory. In August 2023, the company's anode furnace pyrometallurgy refining system technical renovation project was completed and put into operation. In November 2024, the company's three-year action plan for technology-empowered safety and environmental protection was officially finalized, focusing on technology empowerment and fostering new quality productive forces, propelling the company's high-quality development to a new level. Through collaborative development, benchmarking against first-class standards, technological innovation, and increased production and efficiency, the company continues to advance toward its corporate vision of "becoming an evergreen, world-class smelter." The conference is scheduled to be held on September 15–16, 2026 in Lusaka, Zambia. You are cordially invited to participate! Conference Contact : Wu Tao: 18270916376 jennywu@smm.cn

Apr 28, 2026 18:32 - Tibet Summit Resources Unveils 2025 Annual Report, Outlines 2026 Mining and Processing Goals

[Tibet Summit Resources 2025 Annual Report Released] On April 23, Tibet Summit Resources released its 2025 annual report. In 2026, the lead-zinc-copper mine plans to achieve a mining volume of 4.25 million mt, an ore output of 4 million mt, a mineral processing volume of 3.84 million mt, and a lead-zinc-copper-silver metal content output of 150,000 mt. Currently, Tazhong Mining has completed construction of 4 million mt/year mining and processing capacity and 50,000 mt crude lead smelting capacity, and is implementing an additional 2 million mt mining and processing expansion project as well as a smelting industry chain extension project.

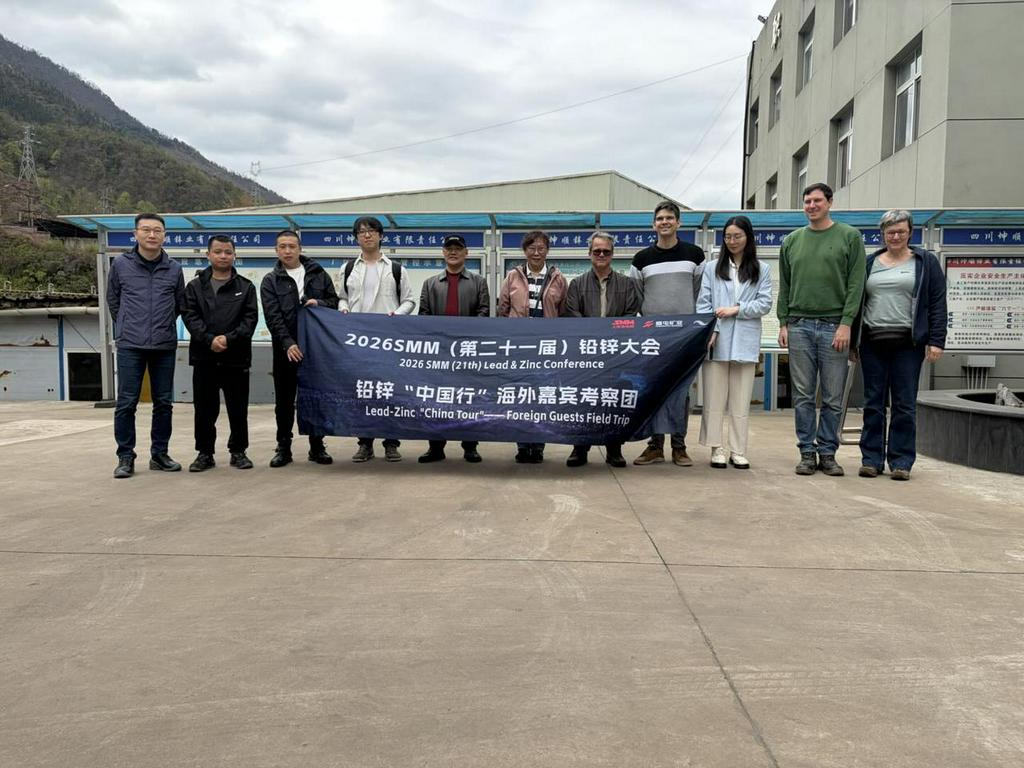

Apr 23, 2026 14:14  Post-Conference Tour: Connecting Global Lead-Zinc Giants with Key Chinese Players

Post-Conference Tour: Connecting Global Lead-Zinc Giants with Key Chinese PlayersThe 2026 SMM (21st) Lead & Zinc Conference and Industry Expo opened grandly at Howard Johnson Agile Plaza in Chengdu, Sichuan during March 25–27 2026. Organized by SMM, the event brought together global enterprises, professional experts and industry peers from across the entire lead and zinc supply chain. Participants focused on industry hot topics, analyzed market trends and explored development strategies, establishing a highly efficient platform for communication and collaboration to support high-quality growth of the sector. To further strengthen the overseas delegation’s comprehensive understanding of China’s lead and zinc industrial chain and build closer connections between international industry peers and key producers in China, SMM led a high-level overseas delegation on a multi-day industrial tour starting on the afternoon of March 27. The delegation included representatives from global giants, such as Nyrstar, a top European lead and zinc smelting firm, Nexa Resources, a South American giant in lead-zinc mining and smelting, and Befesa, a pioneer in zinc recycling. During the tour, the delegation visited 8 Chinese enterprises. including: COSCO Shipping Sichuan Chengtun Zinc & Germanium Technology Sichuan Kunshun Zinc Industry Yunnan Luoping Zinc & Electricity Hongzhou Hongqian Nonferrous Chemical Yunnan Zhenxing Industrial Group Mengzi Mining & Metallurgy Danxia Smelter of Shenzhen Zhongjin Lingnan Nonfemet The delegation members went deep into production sites, held in-depth discussions and exchanges, and gained a full picture of China’s lead and zinc industry in terms of production operations, technological innovation, capacity scale and market layout, greatly enhancing their insight into and understanding of the entire industrial chain. SMM has systematically compiled detailed information of all enterprises that were visited during this tour, with details below: COSCO Shipping On the afternoon of March 27, the delegation visited COSCO Shipping for an exchange, where they received a warm welcome from the company's leadership. Both sides engaged in discussions on topics such as equipment transportation and technological upgrades. Sichuan COSCO Shipping Logistics Supply Chain Management Co., Ltd. is a wholly-owned subsidiary of COSCO Shipping Logistics Supply Chain Co., Ltd., registered and established in Chengdu, Sichuan Province, with an investment of 30 million yuan. COSCO Shipping Logistics Supply Chain Co., Ltd. is affiliated with China COSCO Shipping Corporation Limited and serves as a core member of the "shipping, ports, and logistics" segment of COSCO Shipping Group, as well as an important component of its global digital supply chain system. The company operates warehouse space exceeding 6 million m², including 19 futures delivery warehouses. China COSCO Shipping Corporation Limited is a globally leading shipping enterprise group, with a combined fleet capacity of 130 million DWT across 1,535 vessels, ranking first in the world. Sichuan COSCO Shipping Logistics Supply Chain Management Co., Ltd. holds business qualifications and an operational scope covering multiple transportation modes including sea, land, air, and rail, providing comprehensive logistics services spanning both international and Chinese markets. Since entering the non-ferrous metals delivery warehouse business in 2016, the company has adhered to the principle of "client-centered and market-oriented," continuously enhancing its service capabilities and achieving steady business growth. Currently, at key logistics periods such as Shanghai Baoshan, Shanghai Yangshan, and Yixing in Jiangsu, the company successfully operates delivery warehouses designated by the Shanghai Futures Exchange for copper, nickel, zinc, and other products. It has become one of the three major non-ferrous metals warehouses of SHFE and was honored with the title of "Top Ten Designated Non-Ferrous Metals Delivery Warehouses" by the Shanghai Futures Exchange for two consecutive years. Sichuan Chengtun Zinc & Germanium Technology Co., Ltd. On March 28, the delegation visited Sichuan Chengtun Zinc & Germanium Technology Co., Ltd. (Shimian City). Both sides engaged in in-depth exchanges on the development of the zinc smelting industry, with a focus on thorough discussions regarding product processing, production techniques, capacity scale, market trends, and the current challenges facing the industry. Sichuan Chengtun Zinc & Germanium Technology Co., Ltd. was established on December 6, 2015, with a registered capital of 1.6 billion yuan. The company has an annual capacity of 300,000 mt of electrolytic zinc, 150,000 mt of sulphuric acid, 400,000 mt of electrolytic zinc waste residue processing, and 40 mt of high-purity germanium dioxide. On January 16, 2019, the company was approved by the China Securities Regulatory Commission and merged into the publicly listed firm Chengtun Mining Group Co., Ltd. The company's main business includes smelting and R&D of zinc-germanium series products, as well as comprehensive recovery of multiple metals. It has formed a complete industry chain from zinc concentrates entering the plant to finished products leaving the plant. Its production lines include zinc calcine, electrolytic zinc, electrolytic zinc waste residue processing, and comprehensive recovery of rare and precious metals. Sichuan Kunshun Zinc Industry Co., Ltd. (Shimian City) On March 28, the delegation headed to Sichuan Kunshun Zinc Industry Co., Ltd. (Shimian City) for a visit and exchange, where they received a warm reception from the enterprise. Both parties held in-depth discussions and exchanges on zinc smelting, covering topics such as production costs, production and market landscape, raw material procurement and processing, industry chain competitive advantages, and distinctive process technologies. Sichuan Kunshun Zinc Industry Co., Ltd. is a specialized and green environmental protection enterprise jointly invested and established by Sichuan Metallurgical Holding Group Co., Ltd. and Shimian Dongshun Zinc Industry Co., Ltd. to implement the national green production philosophy, actively develop the circular economy, and promote the comprehensive utilization of solid waste resources. It integrates solid waste treatment, recycling, and resource regeneration. The company primarily uses high-tech methods to carry out clean utilization and harmless treatment of heavy metal-containing waste generated by industries such as metallurgy and chemicals, eliminating the environmental impact of heavy metal solid waste at the source. The company was established in 2021 and is located in Zhuma Industrial Park, Shimian County, Ya'an City, Sichuan Province, covering an area of 65 mu with a total investment of 180 million yuan. The company has built a 3.5m × 50m Waelz rotary kiln production line, equipped with advanced and well-established low-grade zinc oxide production technology, achieving a resource recovery utilization rate of over 95% and effectively managing waste gas, noise, solid waste, and groundwater risks. It is also equipped with supporting facilities including desulphurization, denitrification, and flue gas defogging towers, as well as a wastewater treatment station, raw material warehouse, raw material pre-washing workshop, water slag processing workshop, biomass semi-gasification furnace, zinc crystallized salt workshop, production safety and environmental protection center, and laboratory for detection and testing. The company holds qualifications for treating hazardous waste categories including HW12, HW17, HW23, HW48, and HW49, with an annual capacity to process 100,000 mt of zinc-containing waste. Its main products include low-grade zinc oxide and zinc crystallized salt. The company has always upheld the green and environmentally friendly development philosophy, adhering to the fundamentals of "being responsible for the environment, for clients, and for employees," guided by technological innovation, and targeting the "reduction, recycling, and detoxification" of solid waste pollution prevention and control. The company is committed to building a modern "solid waste" management and disposal service provider, actively carrying out emergency environmental protection disposal, proactively assuming social service functions, and making positive contributions to promoting the circular economy development in Sichuan and strengthening the ecological civilization construction of lucid waters and lush mountains! Yunnan Luoping Zinc & Electricity Co., Ltd. (Qujing City) On March 30, the delegation visited Yunnan Luoping Zinc & Electricity Co., Ltd. (Qujing City) for exchanges. During the meeting, both sides conducted in-depth discussions on key topics including magnesium removal process optimization, production management organization, and raw material substitution plans, and put forward constructive suggestions on improving the plant environment. Yunnan Luoping Zinc & Electricity Co., Ltd. was established to fully leverage Luoping's local hydropower and lead-zinc mineral resource advantages. In accordance with the "ore, electricity, and smelting integration" development strategy proposed by the Luoping County Party Committee and County Government, and the overall requirements of the Municipal Party Committee and Municipal Government for the reform of industrial enterprises across the city, the company was registered and established at the Yunnan Provincial Administration for Industry and Commerce on December 21, 2000. It was listed on the Shenzhen Stock Exchange A-share market in 2007 and is a state-controlled enterprise under Luoping County. The company's assets are an optimized combination of three components: hydropower, lead-zinc mines, and zinc smelting. In terms of company assets, they are primarily composed of three advantageous resources of Luoping: mineral, hydropower, and zinc smelting. These mainly include six production units: Luoping County Fule Lead-Zinc Mine with an annual processing capacity of 100,000 mt of raw ore, Lazhuang Power Plant with annual power generation of 250 million kWh (installed capacity of 60,000 kW), a zinc smelter with an annual output of 120,000 mt of electrolytic zinc, a zinc powder plant with an annual output of 12,000 mt of ultra-fine zinc powder, a comprehensive utilization plant with an annual processing capacity of 129,500 mt of zinc slag, and a sulphuric acid plant with an annual output of 140,000 mt of sulphuric acid, achieving a total annual industrial output value exceeding 2 billion yuan. The company has six wholly-owned subsidiaries. The company's main businesses include hydropower generation, mining of lead, zinc, and other non-ferrous metals, as well as the production and sales of zinc smelting and its extended products. It is currently the only publicly listed firm in China's zinc smelting industry that integrates mining, power generation, chemical processing, and smelting. Its products include zinc sulphide concentrates, lead concentrates, zinc ingots, industrial sulphuric acid, ultra-fine zinc powder, cadmium, germanium concentrates, silver concentrates, copper concentrates, zinc alloys, industrial and residential electricity, edible oils and fats, among others. Its main product, "Jiulong" brand zinc ingots, is popular in non-ferrous product markets in and outside China thanks to its superior product quality and corporate reputation. Honghe Prefecture Hongqian Non-ferrous Chemical Joint-Stock Co., Ltd. On March 31, the delegation visited Honghe Prefecture Hongqian Non-ferrous Chemical Joint-Stock Co., Ltd. for exchanges. The two sides held in-depth discussions on topics including the economic benefits of smelting by-products, energy utilization efficiency, the current status of enterprise development, and future cooperation intentions. Honghe Prefecture Hongqian Non-ferrous Chemical Joint-Stock Co., Ltd. was established on August 1, 2007, with a registered capital of 50 million yuan. The total investment in project construction was 475.5543 million yuan. The company currently has over 600 employees and covers an area of 443 mu. The plant is located in the Heishenmiaobo Industrial Zone, situated in the central area of the Gejiu-Kaiyuan-Mengzi urban cluster. The company is a new-type joint-stock enterprise centered on crude lead smelting, integrating sulphur dioxide acid production, waste heat power generation, lead electrolysis, and recovery of precious and rare metals such as gold, silver, antimony, and bismuth, with further extension into deep processing of lead-series products including red lead, massicot, electrode plates, and storage batteries. It is a benchmark enterprise among private lead smelters in the city, featuring a relatively large scale, advanced technology, compliance with environmental protection standards, comprehensive utilization of resources, and a complete industry chain. The company pioneered the application of new technologies to upgrade and transform the traditional crude lead smelting model among private enterprises in the city. The company has formulated the working philosophy of "prioritizing environmental protection, ensuring safety, attracting talent, enforcing strict management, and enhancing efficiency," and continues to drive high-quality development. In April 2007, the company commissioned China ENFI Engineering Technology Co., Ltd. to conduct a feasibility study on the lead smelting technological transformation project, and determined a comprehensive industrial facility technological transformation project with a total investment of 490 million yuan and an annual capacity of 60,000 mt of crude lead. On December 21, 2009, the "Demonstration Project of Oxygen-Enriched Bottom-Blowing Lead Smelting Technology with Annual Output of 60,000 mt of Crude Lead" was designated by the Provincial Department of Science and Technology as a 2009 Yunnan Provincial Science and Technology Innovation Project. In 2010, it was further designated as a key industrial project by the provincial, prefectural, and municipal governments. On November 14, 2011, the company obtained ISO9001:2008 quality management system certification. On March 7, 2012, "HSPb99.94PCT" was successfully registered on the London Metal Exchange. In 2019, the company successively passed the safety completion acceptance and environmental impact assessment completion acceptance, fully achieving compliant operations and sustainable development. Yunnan Zhenxing Industrial Group Co., Ltd. On March 31, the delegation headed to Yunnan Zhenxing Industrial Group Co., Ltd. for a visit and exchange. Both parties conducted in-depth discussions on topics including Yunnan Province's mineral resource endowment, smelting industry development trends, corporate business strategies, and technological innovation applications, jointly assessing the current status and prospects of the industry and analyzing the challenges and opportunities ahead. Yunnan Zhenxing Industrial Group Co., Ltd. (hereinafter referred to as "the Group") was founded in 1996 and is located in the Chongposhao New Materials Industrial Park, Shadian Sub-district Office, Gejiu City. The Group currently has 7 subsidiaries, 2 holding companies, and 1 equity-participation company, with approximately 3,000 employees. Its capacity reaches annual output of crude lead (100,000 mt), electrolytic lead (60,000 mt), zinc ingot (20,000 mt), lead-acid battery plates (9 million sets), lead-acid batteries (6 million units), superphosphate (350,000 mt), sulphuric acid (200,000 mt), and monoammonium phosphate (MAP) (60,000 mt). The Group has established five major production sites and five major product brands covering crude lead raw material, lead-zinc smelting, power supply manufacturing, fertilizer and chemical production, and resource recovery. It has formed an internal industrial cycle spanning lead ore mining—lead-zinc smelting—lead-based alloy melting—battery manufacturing—waste battery recycling—precious metals production, making it one of the few private non-ferrous enterprises in China with a complete lead industry chain. Since 2013, the Group has been consecutively recognized as one of the Top 100 Non-Public Enterprises in Yunnan Province. In 2025, it ranked 41st among the "Top 100 Non-Public Enterprises in Yunnan Province" and was selected for the first time into the "Top 20 Private Enterprises in Innovation Capability," ranking 7th. Yunnan Shadian Lead Industry Co., Ltd., a subsidiary controlled by the Group, ranked 71st. The Group has received nearly 100 honors at various levels, including "High-tech Enterprise," "Outstanding Private Technology Enterprise," "Enterprise with Harmonious Labor Relations," "Provincial Model Collective for Ethnic Unity and Progress," and "Key Enterprise for Industrial Development in Honghe Prefecture" in Yunnan Province. The Group's Yunsha brand lead ingot was successfully registered on the London Metal Exchange in 2007 and on the Shanghai Futures Exchange in 2020. In 2021, the Group was rated AAA in enterprise credit rating in the national non-ferrous metals industry. In August 2024, it was designated as a "Qiangyuan Zhuqi" Industry-Finance Service Base by the Shanghai Futures Exchange. Looking ahead, the Group will pursue the philosophy of "seeking survival, pursuing development, and accelerating enterprise transformation and upgrading," adhering to the working approach of "rooting in Honghe, basing in Yunnan, radiating to surrounding regions, and expanding across China." It will thoroughly implement strategies of enterprise management transformation, technology-driven development, talent empowerment, and sustainable development, striving to achieve significant increases in capacity and production of major products by 2035, with gross industrial output value up YoY, and to build itself into a 10 billion green lead-zinc comprehensive recycling technology enterprise. Mengzi Mining and Metallurgy Co., Ltd. On March 31, SMM and the field trip delegation headed to Mengzi Mining and Metallurgy Co., Ltd. for a visit and exchange. Both parties engaged in in-depth discussions on the entire zinc smelting process, covering topics including production technology, raw material supply, product sales, environmental protection governance, and future development plans, aiming to share experience, address industry pain points, and jointly clarify the direction of development. Mengzi Mining and Metallurgy Co., Ltd. was established in 1996. It is a resource-based mining and metallurgy enterprise integrating R&D, exploration, mining, mineral processing, smelting, and trading, with a focus on comprehensive utilization of resources. The company is one of the few comprehensive private enterprises in the non-ferrous metal industry that possesses an entire industry chain and operates independent trading and supply chain business platforms. It is among the top 100 enterprises in Yunnan Province and a key enterprise in Honghe Prefecture. Shenzhen Zhongjin Lingnan Nonfemet Co., Ltd. — Danxia Smelter On April 2, the SMM delegation visited Zhongjin Lingnan's Danxia Smelter for a survey and field trip to the core plant area. In-depth discussions were held on production operations, technological R&D, and raw material procurement, covering key topics such as production capacity, technical cooperation, and raw material procurement strategies. Shenzhen Zhongjin Lingnan Nonfemet Co., Ltd. (hereinafter referred to as "Zhongjin Lingnan") was established in September 1984 and listed on the Shenzhen Stock Exchange in January 1997 (stock code: 000060). It is an internationalized entire industry chain resource company primarily engaged in lead, zinc, and copper mining, mineral processing, and smelting, as well as comprehensive recovery of rare, scattered, and precious metals. It is a publicly listed firm controlled by Guangsheng Holdings Group, a key wholly state-owned enterprise under Guangdong Province. Zhongjin Lingnan's business covers segments including mines, smelting, new materials, and supply chains. It has 23 directly affiliated enterprises, wholly-owned and controlled subsidiaries. Major operating entities include Fankou Lead-Zinc Mine, Shaoguan Smelter, Danxia Smelter, Zhongjin Copper Co., Guangxi Mining Co., Perilya Limited in Australia, Zhongjin Technology Co., and Huajiari Co. The company has an annual output of 300,000 mt of lead and zinc metal content in concentrates, 450,000 mt of smelted lead and zinc products, 450,000 mt of copper cathode, 21,000 mt of aluminum extrusion, 20,000 mt of battery zinc powder, and 5,400 mt of composite metal materials. Among these, its battery zinc powder ranked first in Chinese market share, nickel-metal hydride and nickel-cadmium battery electrode sheets & plates materials ranked first in Chinese market share, and thermal bimetal ranked first in Chinese market share. The 2026 field trip brought together some global lead and zinc industry leaders for an inspiring and highly productive journey across China’s leading smelters and enterprises. The warm welcome, operational excellence, and innovative technologies on display made this event a resounding success — and we extend our deepest gratitude to all the companies and participants who made it happen. Looking ahead – Save the date for 2027: We are excited to announce that the 2027 SMM (22nd) Lead & Zinc Conference and Industry EXPO will take place from March 17–19, 2027 in Kunming, Yunnan, China . This premier event will once again bring together the global lead-zinc community for high-level networking, insight sharing, and industrial exploration. Interactive call – We want to hear from you: As we plan the field trip for the 2027 conference, we’d love your input. Which smelters or companies would you most like to visit for technical exchange and on-site learning? Please share your suggestions in the comments below — your feedback will help shape the 2027 experience. Let us know where the industry should go next!

Apr 7, 2026 14:32- Historically Low TCs Threaten Chinese Copper Smelters’ Survival – Sulfuric Acid & Geopolitics Emerge as Key Variables

Since the beginning of this year, the spot treatment charge market for copper concentrates has shown an unprecedented and severe downward trend. The SMM Copper Concentrate Spot Index has fallen from -45 USD/dmt at the start of the year to near -70 USD/dmt, with the speed and magnitude of the decline being historically rare. A negative treatment charge means that when smelters purchase copper concentrates, they not only fail to receive traditional processing income from miners but instead must pay the sellers. Based on the current TC of -70 USD/dmt, the actual cost smelters pay sellers in the copper smelting process is equivalent to a TC of 70 USD, or further converted to a TC+RC of approximately 112 USD. This extreme price signal has quickly drawn high market attention to smelter profitability and even sparked concerns about the sustainability of domestic copper smelting production. Despite treatment charges falling to historic lows, copper cathode production by Chinese smelters remains at high levels, currently around 1.2 million tons per month. This phenomenon of "producing more while losing more" appears, on the surface, to contradict market logic, but actually reflects smelters' passive choices and structural supporting factors in the current complex environment. Historically, extreme treatment charge scenarios are not unprecedented. In past industry downturns, smelters often relied on one or several factors—exchange rate fluctuations, rising sulfuric acid prices, or treatment charges themselves—to barely maintain cash flow balance. In the current cycle, the sharp rise in sulfuric acid prices has become a key variable supporting smelter survival. Currently, the ex-factory prices of smelter acid sold by domestic copper smelters generally range from 800 to 1,600 yuan per ton. The latest SMM Copper Smelting Acid Index stands at 1,235.5 yuan/ton. As a crucial byproduct of copper smelting, sulfuric acid price fluctuations significantly impact smelters' comprehensive earnings. Typically, smelters produce approximately one ton of sulfuric acid for every dry metric ton of copper concentrate processed. Based on the current sulfuric acid price of 1,235.5 yuan/ton, after deducting value-added tax (at a 13% rate) and converting to US dollars (using an exchange rate of 6.9), each ton of sulfuric acid can contribute about 158 USD in revenue for the smelter, equivalent to an additional 158 USD per dry metric ton of copper concentrate. If further converted to the TC+RC metric, this amounts to about 99 USD. Thus, the rise in sulfuric acid prices has significantly offset the loss pressure from negative copper concentrate treatment charges, with some more efficient smelters even achieving marginal profitability. It is precisely this "stabilizer" role of sulfuric acid that allows smelters to maintain high operating rates under extreme treatment charge conditions. However, the support of sulfuric acid for smelting profits is not unlimited, as its price trend is itself influenced by more complex international geopolitical factors. The recent sharp escalation of the Middle East situation has brought significant uncertainty to the global sulfuric acid and sulfur supply chain. Since the joint US-Israeli military strike against Iran on February 28, 2026, the Strait of Hormuz, the world's most critical energy transport route, has rapidly fallen into a severe transit crisis. After taking office, Iran's new Supreme Leader, Mojtaba Khamenei, immediately declared that the strait would remain closed as a strategic lever against the US-Israeli alliance and suggested that neighboring countries close US military bases. The Islamic Revolutionary Guard Corps subsequently explicitly announced a ban on any vessels associated with the US or Israel from passing through the Strait of Hormuz, warning of severe consequences for unauthorized passage. The Strait of Hormuz is a critical chokepoint for global sulfur transport. Statistics show that before the conflict, over 100 ships passed through the strait daily. However, after the conflict erupted, transit traffic plummeted by over 90%, with extreme cases of no ships passing for an entire day, leaving over 3,000 vessels stranded in nearby waters. This effective blockade has not only directly impacted the crude oil market—with Brent crude futures rising over 50% within a month to exceed 114 USD per barrel—but has also severely disrupted the global supply chain for sulfur and sulfuric acid. War risks have caused shipping insurance costs to soar to over 20% of the cargo value, further increasing logistics costs and plunging global sulfur supply into a logistical crisis. Although Iran claims to allow passage for vessels from "non-hostile" countries, requiring them to obtain prior permission, actual transit volumes remain extremely low, far below global trade demand. Simultaneously, the Houthi armed group in Yemen has announced its involvement, posing new security threats to the Red Sea-Suez route. The compounding pressure on the two major shipping chokepoints of the Strait of Hormuz and the Red Sea is posing a systemic challenge to the global supply chains for energy and chemical raw materials. As the primary raw material for sulfuric acid production, the disruption in sulfur supply directly drives international and domestic sulfuric acid prices progressively higher. Given the current situation, geopolitical conflicts show no signs of easing in the short term, implying further room for sulfuric acid price increases. The continued rise in sulfuric acid prices will have a dual impact on the domestic copper smelting industry. On the one hand, increased sulfuric acid revenue will continue to provide crucial profit supplementation for smelters, enabling them to maintain production even at lower TC levels and potentially further depressing spot copper concentrate treatment charges. On the other hand, this surge in sulfuric acid prices, driven by geopolitical conflict, also makes smelter profitability highly dependent on external unstable factors, rendering the industry's overall risk resilience increasingly fragile. Notably, the extreme treatment charge environment has begun to have a tangible impact on the global layout of copper smelting capacity. Mitsubishi Materials of Japan recently announced its plan to cease operations at its Onahama copper smelter by the end of March 2027. The smelter has a crude and refined capacity of 230,000 tons, and the main reason for the closure is precisely the intensified competition in the global copper smelting industry, leading to a sharp deterioration in copper concentrate TC/RC and persistent pressure on business prospects. This decision sends a clear signal: against the backdrop of continuously bottoming treatment charges and industry profits highly dependent on byproducts and external environments, some high-cost smelting capacity or those lacking comprehensive recovery capabilities are facing pressure to exit the market. In summary, China's copper smelting industry is currently at a highly unusual cyclical juncture. On one hand, smelters, benefiting from high sulfuric acid prices, have temporarily weathered the impact of negative treatment charges, maintaining high output. On the other hand, sulfuric acid prices themselves are heavily dependent on geopolitical situations, and external variables like the Strait of Hormuz blockade introduce significant uncertainty into the sustainability of smelting profits. If tensions in the Middle East persist, sulfuric acid prices may continue to rise, leaving room for TC to fall further, potentially enhancing smelters' tolerance for extreme treatment charges in phases. However, if geopolitical tensions ease, sulfur supply chains recover, and sulfuric acid prices retreat from their highs, smelters would face the risk of a "double blow" from both low treatment charges and reduced byproduct revenue, potentially heralding a genuine phase of capacity reduction and deep adjustment for the industry. Therefore, the current apparent "resilience" of the copper smelting industry is essentially built upon a fragile balance between geopolitical factors and the byproduct market. For market participants, besides monitoring TC trends, it is crucial to closely track changes in sulfuric acid prices and the underlying geopolitical factors to make more accurate judgments regarding the production sustainability and profitability prospects of the smelting industry.

Mar 30, 2026 12:20 - [SMM Analysis] How Chinese Copper Smelters Navigate Counter-Cycle & Negative TCs: Sulfuric Acid Becomes Primary Product

On March 13, 2026, China's copper smelting industry set a new historical record. According to SMM data, the imported copper concentrate index closed at -60.39 USD/dmt, officially breaking through the -60 USD level.

Mar 13, 2026 18:46