756results found for 'Price Forecast'

Price

News

- Lead Prices Pull Back After Slight Catch-Up Gains, Consumption Performance Restricts Rebound Room for Lead Prices [SMM Lead Morning Meeting Summary]

Futures: Overnight, LME lead opened at $1,893/mt, drifted higher in Asian trading to touch a high of $1,907.5/mt before weakening, and entering European trading, LME lead gave back most of its gains, dipping to a low of $1,883.5/mt, and finally closing at $1,890/mt, unchanged with a 0% change. Overnight, the most-traded SHFE lead 2609 contract opened at 15,735 yuan/mt, early in the session touched a session high of 15,745 yuan/mt before drifting lower, bulls reduced positions on SHFE lead, dipping to a low of 15,600 yuan/mt in late trading, and finally closing at 15,640 yuan/mt, down 0.73%. Macro Front: US July ADP employment came in at 44,000, below market expectations of a 70,000 increase and the downwardly revised 95,000 in June, marking the smallest gain since January this year. The US Treasury Department will maintain its buyback program at the same pace as the previous quarter and keep auction sizes unchanged at least for the coming few quarters. China's Ministry of Commerce: Countermeasures taken against US compliance testing companies. China's designated certification body for CCC certification suspended entrusting US certification organizations to conduct factory follow-up inspections. The "15th Five-Year Plan for Promoting the Development of Small and Medium-Sized Enterprises," jointly formulated by MIIT and multiple departments, is about to be released. The Ministry of Foreign Affairs responded to the US plan to ban Chinese optical modules: China firmly opposes the US generalization of the national security concept and will continue to firmly safeguard the legitimate rights and interests of Chinese enterprises. Spot Fundamentals: In Shanghai, Chihong lead was quoted at 15,730-15,830 yuan/mt, representing premiums of 50-100 yuan/mt against the most-traded SHFE lead 2609 contract. SHFE lead rose sharply, suppliers sold cargoes as the market moved, and premium quotes in Jiangsu, Zhejiang, Shanghai remained unchanged. However, quotes for EXW cargoes from primary lead smelters diverged; smelters held prices firm while selling, while traders widened discounts on sales, with mainstream producing regions quoting premiums of 0-50 yuan/mt against SMM #1 lead average price. In secondary lead, as lead prices rebounded, secondary lead smelters showed slightly improved willingness to sell, secondary refined lead quotes were at discounts of 25-0 yuan/mt against SMM #1 lead average price, with a few at a premium of 75 yuan/mt. Downstream enterprises exhibited strong wait-and-see sentiment, inquiries significantly decreased from yesterday, some suppliers indicated almost no inquiries, and spot market trading volume plummeted. Inventory: On August 5, LME lead inventory decreased by 3,325 mt to 431,550 mt; as of August 3, SMM lead ingot social inventory across five locations totaled 72,100 mt, up 3,700 mt from July 27 and 3,600 mt from July 30. Lead Price Forecast Today: Supply side, primary lead saw additional maintenance in August, with production expected to decline; while secondary lead production also has expectations of decline, attention should be paid to the boost from the rebound in lead prices on smelter production enthusiasm, with some enterprises having the probability of early production resumptions. In addition, currently lead ingot social inventory stays high, be cautious of the pullback risk for lead prices due to suppliers' lead ingot warehouse transfers before delivery. Domestic consumption is neutral overall, with conservative demand in the e-bike sector and relatively stable demand in July-August; in the automobile sector, demand is experiencing a tug-of-war: enterprises handling export orders are doing well, while those serving the Chinese market are underperforming. Overall, the exit of bears has led to a short-term lead price rebound and catch-up rally, but the performance of the consumption side determines the room for the lead price rebound.

Aug 6, 2026 08:06 - Gold, Silver, Platinum, Palladium Dance Together, Precious Metals Sector Surges Nearly 8%, Shengda Resources and Sichuan Gold Hit Daily Limit [SMM Flash News]

SMM, August 5: Expectations for Middle East geopolitics are shifting toward easing, oil prices have pulled back sharply for two consecutive trading days, and market concerns about inflation have cooled. Expectations for a US Fed interest rate hike in September have pulled back, with multiple positive factors resonating to drive precious metals futures and stocks to strengthen together. In the futures market: As of around 17:12 on August 5, COMEX gold was up 1.7% at $4,223.1/oz; SHFE gold main contract was up 3.1% at 910.4 yuan/g; COMEX silver was up 2.53% at $61.77/oz; SHFE silver main contract was up 7.08% at 15,105 yuan/kg; silver T+D was up 5.8% at 14,988 yuan/kg. Platinum main contract futures were up 9.18% at 441.15 yuan/g; palladium main contract futures were up 8.51% at 329.65 yuan/g. In the stock market: As of market close on August 5, the precious metals sector was up 7.87%. In individual stocks: Sengda Resources and Sichuan Gold hit the daily limit up, while Xiaocheng Technology, Chifeng Gold, Zhongjin Gold, Xingye Silver&Tin, and Shanjin International were among the top gainers. News [South Korea's Central Bank Plans to Purchase Domestically Refined Gold Bars for the First Time in 13 Years] According to South Korean media reports, the Bank of Korea said on Monday that it will cooperate with LS MnM, the Korea Exchange (KRX), and the Korea Securities Depository (KSD) to purchase domestically produced gold for the first time in 13 years through over-the-counter transactions, as heightened geopolitical risks have increased the need to diversify foreign exchange reserves. LS MnM and Korea Zinc produce about 40 to 45 mt of gold annually as a by-product of smelting, of which about 10% is exported. The central bank stated that if relevant enterprises apply, it will consider using the trading and settlement system of the KRX and the storage facilities being prepared by the KSD to purchase some of the gold intended for export. The central bank said it will arrange bulk transactions after prior consultations on price and quantity to limit the impact on domestic gold prices, and that the new channel should reduce foreign exchange risks, since previous overseas purchases were all paid in US dollars. Additionally, the central bank also stated that it purchased a small amount of gold ETFs in Q2. Separately, it was reported that as of July, its gold holdings remained unchanged at 104.4 mt, while South Korea's foreign exchange reserves at the end of June stood at $427.36 billion, including gold reserves worth $4.79 billion. [World Gold Council: Gold Investment Demand Expected to Remain Positive] The World Gold Council report noted that in the remainder of 2026, investment demand is expected to be the main driver of gold demand growth, and will be increasingly supported by over-the-counter trading activities and Asian investment demand. Central banks will remain key gold buyers. High gold prices will continue to suppress gold jewelry demand, but the response of gold ore production and recycled gold supply is expected to be relatively mild. Gold investment demand is expected to remain positive for the rest of 2026. OTC activity and Asian investment demand are expected to play a larger role, while Western gold ETF flows may continue to be sensitive to US Treasury real yields, Fed monetary policy expectations, and the US dollar. Although consumer spending has remained relatively resilient, high gold prices will continue to suppress gold jewelry demand; technology-related gold demand is expected to further benefit from AI investment, but downside risks are accumulating. (Jinshi Data) [Zijin Mining: Terminates Acquisition of United Gold, Plans to Subscribe for 9.2% Equity] Zijin Mining announced on the Hong Kong Stock Exchange that on January 26, 2026, its controlled subsidiary Zijin Gold International signed an Arrangement Agreement with United Gold, under which Zijin Gold International would acquire all outstanding common shares of United Gold for a cash price of C$44 per share, with a total consideration of approximately C$5.5 billion (approximately $4 billion). However, after comprehensive evaluation, both parties believed that certain closing conditions precedent could not be fully satisfied or waived by the deadline stipulated in the acquisition agreement (which had been extended to July 29, 2026) or within a reasonable period thereafter. The parties agreed to terminate the acquisition, and neither party is required to pay a termination fee or any other fees to the other. Meanwhile, the parties separately entered into a Share Subscription Agreement, under which Zijin Gold International intends to subscribe for 12.8 million common shares (representing approximately 9.2% of the enlarged share capital post-issuance) placed by United Gold at a cash price of C$32.55 per share, with a total subscription amount of C$416.6 million, equivalent to approximately $295 million. [Chifeng Gold: Expects H1 2026 Net Profit to Increase by 54%-61% YoY] Chifeng Gold disclosed an earnings forecast on the evening of July 14, expecting its H1 2026 net profit attributable to shareholders to be 1.7 billion yuan to 1.78 billion yuan, up 54%-61% YoY. [Zhaojin Gold: Expects H1 2026 Net Profit to Increase by 347.48%-436.98% YoY] Zhaojin Gold disclosed an earnings forecast on the evening of July 14, expecting its H1 2026 net profit attributable to shareholders to be 200 million yuan to 240 million yuan, up 347.48%-436.98% YoY; recurring net profit is expected to be 80 million yuan to 116 million yuan, up 490.44%-756.14% YoY. [Shandong Humon Smelting: Expects H1 2026 Net Profit to Increase by 81.06%-122.36% YoY] Shandong Humon Smelting disclosed an earnings forecast on the evening of July 14, expecting its H1 2026 net profit attributable to shareholders to be 570 million yuan to 700 million yuan, up 81.06%-122.36% YoY; recurring net profit is expected to be 272 million yuan to 402 million yuan, down 2.03%-33.73% YoY. [Western Gold: H1 2026 Net Profit Expected to Rise 280.16%-333.39% YoY] Western Gold disclosed on the evening of July 13 that it expects its H1 2026 net profit attributable to the parent company to be 500 million to 570 million yuan, up 280.16%-333.39% YoY; and adjusted net profit to be 490 million to 580 million yuan, up 172.96%-223.09% YoY. [Zhongjin Gold: H1 2026 Net Profit Expected at 4.1-4.6 Billion Yuan, up 52.15%-70.7% YoY] Zhongjin Gold disclosed on the evening of July 13 that it expects its H1 2026 net profit attributable to the parent company to be 4.1 billion to 4.6 billion yuan, up 52.15%-70.7% YoY; and adjusted net profit to be 4.05 billion to 4.55 billion yuan, up 36.96%-53.87% YoY. Spot Market Silver On August 5, the morning ex-factory reference average price of SMM #1 silver was 14,556 yuan/kg, up 2.38% from the previous trading day. In the spot market, downstream demand remained sluggish this month, with limited new orders overall. The strengthening silver price further weakened downstream purchase willingness; market transactions mainly relied on support from banking institutions, with deals concentrated around parity, and traders were reluctant to quote. Morning quotations in Shanghai were mostly at parity to a premium of up to 10 yuan/kg against TD; in Shenzhen, some national standard goods were quoted around parity. Although low-priced goods existed, they did not significantly disturb spot trade. Today, the market quoted a discount of 60 to 50 yuan/kg against the most-traded SHFE contract 2610. Overall, expectations for a Strait of Hormuz agreement heated up, inflation concerns eased briefly, and precious metals recovered slightly. In the spot market, the rise in silver prices further suppressed demand, with orders remaining sluggish and trading staying thin. Voices Regarding the future trend of precious metals, some institutions' views are as follows: CITIC Securities research report stated that this year gold prices shot up and then fell rapidly, but we believe gold is still in a major bull market, with reasons including the accelerating expansion of the US fiscal deficit, irreconcilable geopolitical rifts under deglobalization, and continued gold purchases by global central banks providing a floor. Therefore, we think this round of decline in gold prices is merely a temporary correction within the bull market. The current pullback has approached historical extremes, and the $4,000/oz area is highly likely to be the bottom zone for this round. Looking ahead, the impact of the Strait of Hormuz situation on gold prices is expected to shift from a drag to a boost, the Fed's monetary policy may be more optimistic than market expectations, and coupled with surging US military spending driving up the deficit, gold prices are expected to return to an uptrend within the year. Deutsche Bank precious metals strategist Hsueh Michael stated that the "explosive rally phase" for gold prices that began in August 2024 is not yet over, and maintains the forecast of gold at $4,600/oz in Q4 2026. This assessment rests on a triple framework of fair value models, statistical tests, and official demand data, discounting the significant downside risk implied by commodity price ratios. (Zhitong Finance) A research report from CICC Wealth Futures shows: oil prices pulled back, gold rebounded, and currently, the yen's disruption causing moves in the US dollar index is a new disturbance factor, which is expected to have a relatively limited impact on gold price trends. The biggest pressure on gold currently still comes from oil prices. CICC Wealth Futures believes that if oil prices are not excessively strong, the probability of gold maintaining a fluctuating trend or drifting higher is relatively high. Everbright Futures' outlook for August suggests that the short-term gold price trend depends on the evolving US-Iran situation. If the conflict persists or its spillover expands, market sentiment may weaken again, and under liquidity risk expectations, gold prices may continue to underperform. However, if a substantive breakthrough in negotiations occurs, gold prices could stabilize in the short term and undergo a recovery and rebound. At that point, if domestic and overseas financial markets show a synchronized recovery, it can be further confirmed. Nevertheless, it can be expected that with support from rigid central bank purchases and allocation demand, even if a pullback occurs again, the downside should be relatively limited. Additionally, at the Jackson Hole Economic Symposium at the end of August, Warsh may outline a medium-term policy framework. Before that, the US CPI data on the 12th will be a key verification indicator. Overall, gold is likely in a stage of bottom consolidation and sentiment repair, and we hold a cautiously optimistic view. The core risk is that the US-Iran conflict once again pushes oil prices above $90/oz, a significant rebound in US inflation data far exceeding expectations, and the evolving probability of a September rate hike continuing to suppress market sentiment. However, judging from the performance of overseas financial markets and oil prices, a full-scale escalation of the US-Iran conflict is largely unsupported. A Reuters survey showed that after gold prices pulled back significantly from their record highs in January, analysts cut their gold price forecasts for the first time since the end of 2023, though most still expect support from central bank buying and concerns over fiscal sustainability. In the survey of 29 analysts and traders conducted over the past three weeks, the median forecast for gold prices in 2026 was $4,509/oz. That figure is down from $4,916 three months ago and marks the first downgrade in 11 quarters. The average forecast for 2027 is $4,610, compared to a forecast of $5,100 in the previous poll. Gold prices hit an all-time high of $5,595/oz in January, but suffered a sharp pullback in Q2 as the Iran war exacerbated energy inflation and boosted rate hike expectations, marking the worst quarterly performance since 2013. Since the outbreak of the war, spot gold has fallen about 22%. (Jinshi Data APP) Analysts Warren Patterson and Ewa Manthey from ING noted that gold prices rose on Monday, as a sharp decline in oil prices eased inflation concerns and pressured the US dollar and US bond yields. The large drop in oil prices on Monday alleviated inflation worries and the prospect of further monetary tightening. The move came after a pause in US-Iran hostilities. Lower oil prices also weighed on the US dollar and bond yields, improving the outlook for non-yielding assets ahead of this week’s Fed meeting. Markets are now focused on the Fed and the upcoming US inflation data for further guidance on the interest rate outlook. If yields remain subdued, gold prices should continue to be supported near current levels. However, any hawkish surprise from the Fed could limit further upside room in the near term. Commerzbank has lowered its year-end gold price forecast to $4,500 per troy ounce, and now expects platinum to reach $2,000 per troy ounce by year-end, down from a previous forecast of $2,100. Citi said its base case shows that India’s gold imports will remain subdued in the third quarter, despite historically being a seasonal peak for stockpiling. The reasons include ample scrap supply, cautious consumer sentiment and local price discounts curbing demand for fresh imports. However, Citi maintains its short-term gold price target of $4,500 for 0–3 months. This target, the bank said, assumes an easing of tensions in the Strait of Hormuz and a less hawkish turn by the Fed; in the short term there remain many risks that could push gold prices lower again, including a major re-escalation, AI-driven de-risking, and a persistently hawkish stance by the Fed. UBS gold strategist Joni Teves remains optimistic on the medium to long-term outlook for gold. She noted in her comments that gold prices have been rising since the start of this week, with gold stocks in mainland China and Hong Kong surging around 20% over three days – a positive signal. “We believe confidence in gold is starting to improve and continue to expect that prices will rebound from current levels by year-end,” she said. UBS’s global team remains upbeat on gold’s medium-term outlook and forecasts prices will reach $4,675 per ounce by end-2026 and $4,800 per ounce by end-2027. She indicated that the key events to watch going forward are the Fed’s policy tone at the FOMC meeting at the end of July and further developments in the Middle East. (Jinshi Data APP) Analysts at ANZ Research said in a report that physical demand for the metal and central bank purchases are supporting the gold market. These analysts added that while gold prices face short-term headwinds from the US Fed's tightening expectations and a strong US dollar, after months of outflows from exchange-traded funds, gold investment positions look thin, suggesting limited room for further declines. A high-interest-rate environment typically weighs on non-yielding assets like gold. (Zhitong Finance) Goldman Sachs stated that despite pressure from the US Fed's tightening expectations, central bank purchases are expected to provide a floor for gold. Demand remains robust, with the bank estimating that central banks bought 81 mt of gold in May and the three-month average of monthly purchases at 67 mt, far above the pre-2022 average of 17 mt. Goldman Sachs analysts said, "We believe the trend of central banks increasing their gold holdings will continue for many years as they diversify reserves to hedge geopolitical and financial risks." The bank forecasts average monthly purchases will be 50 mt this year and 40 mt next year. (Jin10 Data) Kim Soojin, analyst at Mitsubishi UFJ Financial Group, said, "Recent price action suggests that the market is placing more weight on the likelihood that US interest rates will stay high for longer rather than on gold's traditional safe-haven demand. This leaves gold vulnerable to pressure unless geopolitical risks further translate into a broad deterioration in financial market sentiment." (Jin10 Data) Fidelity International, an asset manager, said it plans to add to its gold positions again at an appropriate time after reducing them earlier this year, believing gold's long-term momentum remains strong. Ian Samson, multi-asset portfolio manager at Fidelity International, said recently, "We plan to add to our gold positions again; the question is just the timing." He said he reduced his gold allocation to a neutral level from January to February this year, when gold's multi-year bull market abruptly ended. Samson expects the gold market to re-enter a bull market sometime in 2027. The logic for a return to a bull market would only be undermined if "governments re-embrace fiscal discipline and central banks are truly committed to bringing inflation back down," "but I don't think we're in that world right now." Samson also noted that continued central bank gold purchases, a key driver of the previous bull market, will continue to support gold prices. A research report from Guoxin Securities shows that after a deep correction in H1, gold prices near $4,000 are gradually showing signs of bottoming out, with further upside only awaiting event catalysts. It recommends building positions in batches near $4,000 on dips and avoiding chasing rallies. Key allocation logic: First, valuations are at historically low levels, providing a notable margin of safety. After a deep pullback in H1, current valuations of gold mining companies have retreated sharply from the beginning of the year to low levels, offering high odds. Going forward, aside from a valuation repair rally, they are expected to further benefit from the price elasticity driven by rising gold prices. Second, earnings elasticity advantage is significant. Gold stocks act as an "amplifier" for gold prices—the cost of gold mining is rigid, so rising gold prices directly translate into profit growth, making earnings elasticity far exceed the gold price increase itself. A research report from Huayuan Securities points out: from a medium-term perspective, the market’s core trading logic has anchored on the pricing chain of "inflation stickiness and resilience exceeding expectations → extended period of high rates by the US Fed → repeated intensification of rate hike expectations within the year," and gold's price center remains dominated by US real bond yields and the US dollar index, with the overall market likely to consolidate on a subdued note. Ceasefire consultations in the Middle East are currently mired in back-and-forth maneuvering, with the two sides significantly diverging on core demands such as troop withdrawal arrangements, nuclear facility inspection mechanisms, and control rights and toll rules for navigation in the Strait of Hormuz. The recurring geopolitical conflicts continue to disrupt global crude oil supply expectations, and the upside risk of energy prices may further entrench inflation stickiness, in turn supporting the US Fed's tightening policy stance. Meanwhile, the simultaneous rise in the US dollar index and US bond yields is creating a dual suppression effect; coupled with gold's safe-haven attributes temporarily yielding to interest rate pricing logic, the upside room for gold prices may continue to be constrained. Key events to watch over the next two weeks include: 1) developments in the Middle East conflict and navigation conditions in the Strait of Hormuz; 2) the US Fed’s interest rate decision to be announced on July 30; 3) the US June PCE to be released on July 30. In the long term, gold’s bullish logic has not weakened but has been further strengthened amid changes in the global macro and geopolitical landscape. 1) The constraints of US fiscal deficits, debt expansion, rising trade protectionism, and intensifying major-country competition are weakening the stability of the US dollar credit anchor, driving a reallocation of global reserve assets toward diversification. Gold is gradually evolving into an important asset for hedging sovereign credit risks, geopolitical fragmentation risks, and risks of restructuring the global monetary system. 2) Continued gold purchases by global central banks still provide solid bottom support for gold prices, and the PBOC’s continued increase in holdings further confirms the official sector’s long-term allocation demand. 3) The late-cycle US economy faces multiple constraints of high interest rates, credit contraction, and a growth slowdown. In the future, whether the US Fed cuts interest rates due to an economic slowdown or is forced to maintain higher rates for longer due to sticky inflation, gold possesses strong long-term allocation value: the former is favorable for declining real interest rates, while the latter strengthens demand for safe-haven and credit-risk protection. Overall, gold remains in a favorable window in the medium and long term, and its price center is expected to continue shifting upward amid the reshaping of the global macro and geopolitical landscape. Recommended Reading:

Aug 5, 2026 17:17 - Deutsche Bank sees gold's correction as largely done, holds US$4600 Q4 target

Deutsche Bank says gold's current rally, running since August 2024, is one of only five such episodes since 1975. Analysts at the bank see the recent pullback as largely complete and reiterates its $4,600/oz Q4 2026 forecast.

Aug 5, 2026 10:43 - Gold Price Forecast & Predictions 2026, 2027: RBC Sees Bullion Reaching $5,321

Published: 3 Aug 2026, 17:30 BST RBC’s high scenario keeps gold near $5,300 through 2027 as central-bank buying and stronger Asian investment demand cushion bullion on the downside. The Gold price in US Dollars slipped back towards $4,037 on Monday after ending last week near $4,072, but analysts at RBC Capital Markets still see a route towards $5,300 under its bullish scenario. The bank’s latest forecast puts gold at an average $5,132 in the third quarter, rising to $5,203 in the fourth quarter. Its 2027 high case averages $5,296, with quarterly forecasts between $5,249 and $5,321. RBC’s central scenario is more restrained, forecasting $4,558 this quarter, $4,370 in the fourth quarter and an average of $4,225 in 2027. The bullish case rests partly on demand holding up better than the headline data suggest. “In a YTD period that has seen a nearly $1,500/oz range for gold prices, Q2 ended with some notable dynamics,” RBC said. Central banks bought 289 tonnes during the second quarter after a slower opening quarter, outpacing both jewellery demand and bar-and-coin purchases. RBC said the official sector remained a “consistent positive undercurrent”, adding that Poland, Uzbekistan, China and Kazakhstan were the largest reported buyers this year. Gold traded between roughly $3,963 and $4,202 over the past month before returning towards $4,070. Investor demand in Asia is another important support. RBC highlighted “underlying shifts in Asia towards investor products, at the detriment of consumer products like jewellery”, arguing that the move still “nets out positive for total demand”. The bank added that Asian markets continue to dominate global bar-and-coin demand. Gold Outlook: Official Buying Cushions the Downside Exchange-traded fund demand weakened during the second quarter, but RBC noted that “Q3 has started off with inflows and YTD flows are positive”. That helps explain why the bank’s high scenario remains well above current prices despite gold’s difficult year. XAU/USD is down around 5.7% in 2026 and continues to trade below its 20-day and 50-day moving averages. The price of Gold remains lower for the year after falling sharply from January’s peak above $5,500. RBC’s low scenario still warns of substantial downside, with gold averaging $3,729 in the third quarter and $3,661 during 2027. Its high case, however, keeps the prospect of $5,300 gold firmly alive if central-bank purchases remain strong and investment demand continues shifting towards bullion. Source: https://www.exchangerates.org.uk/news/46716/2026-08-03-gold-price-forecast-predictions-2026-2027-rbc-sees-bullion-reaching-5-321.html

Aug 5, 2026 10:29 - Lead Prices Briefly Stop Falling; Focus on Support from Improving Consumption for Rebound [SMM Lead Morning Meeting Minutes]

Futures: Overnight, LME lead opened at a low of $1,869/mt and then rose along with a broad rally in nonferrous metals, reaching a high of $1,898/mt in the European session before finally closing at $1,890/mt, a gain of 1.23%. Overnight, the most-traded SHFE lead 2609 contract opened higher with a gap at 15,520 yuan/mt, briefly touched a low of 15,490 yuan/mt after the open, drifted higher, and with bears reducing positions, rose to a high of 15,630 yuan/mt late in the session, finally closing at 15,605 yuan/mt, a gain of 1.04%. Macro: The US government solicited comments in the Federal Register on expanding the scope of metal tariff products, proposing tariffs on items such as welding machines and cranes. US Treasury Secretary Bessent: (On writing “buy yen” in a notepad) the aim was to ensure that reporters saw it. Bessent: It is possible to reach an agreement with Iran tomorrow (Wednesday, US Eastern Time) to open the Strait of Hormuz. China News Service reported that foreign media said the US plans to ban imports of Chinese optical modules. The central bank: It will conduct a 500-billion-yuan outright reverse repo operation on August 5, with a term of 3 months. The State Administration for Market Regulation held a meeting to advance a special campaign to thoroughly implement the fair competition review system. The central bank released data on liquidity provision through various tools in July 2026, with a net injection of 249.5 billion yuan via 7-day reverse repos and a net injection of 50 billion yuan through open market purchases of government bonds. Spot Fundamentals: SHFE lead rebounded after hitting a low, with suppliers selling along with the market and holding prices firm. Quotations from mainstream production areas were at premiums of 0-50 yuan/mt against the SMM #1 lead average price for ex-works delivery. In secondary lead, smelters were more frequently reducing or halting production, and some enterprises held prices firm to sell. Secondary refined lead quotations were at parity against the SMM #1 lead average price for ex-works delivery, with a few at a premium of 200 yuan/mt. Downstream enterprises were intending to buy the dip, with improving inquiry activity, among which EXW cargoes from smelters saw better transaction. Inventory: On August 4, LME lead inventory decreased by 3,575 mt to 434,875 mt. As of August 3, total social inventory of SMM lead ingots in five regions reached 72,100 mt, up 3,700 mt from July 27 and up 3,600 mt from July 30. Today's Lead Price Forecast: Currently, risks from overseas geopolitical conflicts persist, with no expectations for lead consumption recovery in the Middle East. However, lead consumption in Southeast Asia is steady with a slight uptick, and spot premiums are widening, which will support the center of lead prices to shift upward to some extent. In the domestic spot market, downstream enterprise inquiry activity improved, and spot order trading volume increased. Combined with expectations for maintenance and production cuts at some smelters, bullish sentiment emerged, and lead prices briefly stopped falling.

Aug 5, 2026 08:04 - Downstream Lead-Acid Battery Enterprises Showed Strong Risk-Aversion Sentiment, Lead Ingot Transaction Performance Was Poor [SMM Lead Morning Meeting Minutes]

Futures: Overnight, LME lead opened at $1,878.5/mt, briefly touching a high of $1,885.5/mt in Asian trading before drifting lower. As the US dollar index rebounded, LME lead came under pressure and hit a low of $1,858.5/mt during European trading, eventually settling at $1,867/mt, down 0.72%. Overnight, the most-traded SHFE lead 2609 contract opened at a high of 15,385 yuan/mt, then drifted lower as bears added positions. It touched an intraday low of 15,205 yuan/mt before moving sideways, ultimately settling at 15,255 yuan/mt, down 1.13%. On the macro front: The US Treasury raised its Q3 borrowing estimate to $739 billion. Twenty-five US states filed a lawsuit against the latest tariff measures by the US government. The Bank of Korea planned to purchase domestic refined gold bars for the first time in 13 years. Fed's Williams: was optimistic that inflationary pressures will gradually ease. If inflation does not return to the 2% path as expected, the Fed will act to achieve price stability. China's Ministry of Commerce: Foreign enterprises have filed a Section 337 investigation application concerning certain secondary cylindrical batteries, battery components, and products containing the same. The China Securities Regulatory Commission and the Securities and Futures Commission of Hong Kong jointly announced new measures to deepen practical cooperation and close coordinated development between the two markets. Spot fundamentals: SHFE lead extended its decline, initially falling to a more than three-year low. Suppliers diverged significantly on shipments, with some planning to deliver to warehouses and others selling at prevailing prices. Quotations in mainstream producing areas were at discounts of 30 yuan/mt to premiums of 20 yuan/mt against the SMM #1 lead average price, ex-works. For secondary lead, smelters held back from selling at low prices, with few offering material; some secondary refined lead was quoted at parity against the SMM #1 lead average price ex-works, and a few at a premium of 200 yuan/mt. Meanwhile, downstream enterprises maintained a strong wait-and-see sentiment, though some showed intentions to buy the dip; trading activity in the spot market improved slightly. Inventory: On August 3, LME lead inventory decreased by 2,825 mt to 438,450 mt. As of August 3, total social inventory of SMM lead ingot in five regions was 72,100 mt, up 3,700 mt from July 27 and up 3,600 mt from July 30. Today's Lead Price Forecast: Recently, lead prices have fallen successively, hitting a new low for nearly three years. Downstream lead-acid battery enterprises have maintained a strong risk-off sentiment and stayed cautious in procurement. Against a backdrop of sluggish consumption, in-factory inventory at lead smelters has been rising steadily since late July. Primary lead suppliers gradually shifted lead ingots to delivery warehouses, pushing social inventory higher. Before delivery, suppliers are expected to continue such transfers, and social inventory of lead ingots will extend its upward trend. Due to expectations of additional maintenance at primary and secondary lead smelters, the slowdown in lead ingot supply will curb the increase in inventory. Overall, bearish factors for lead prices remain strong, and the support from supply-side slowdown on lead prices should be monitored.

Aug 4, 2026 08:58

Events

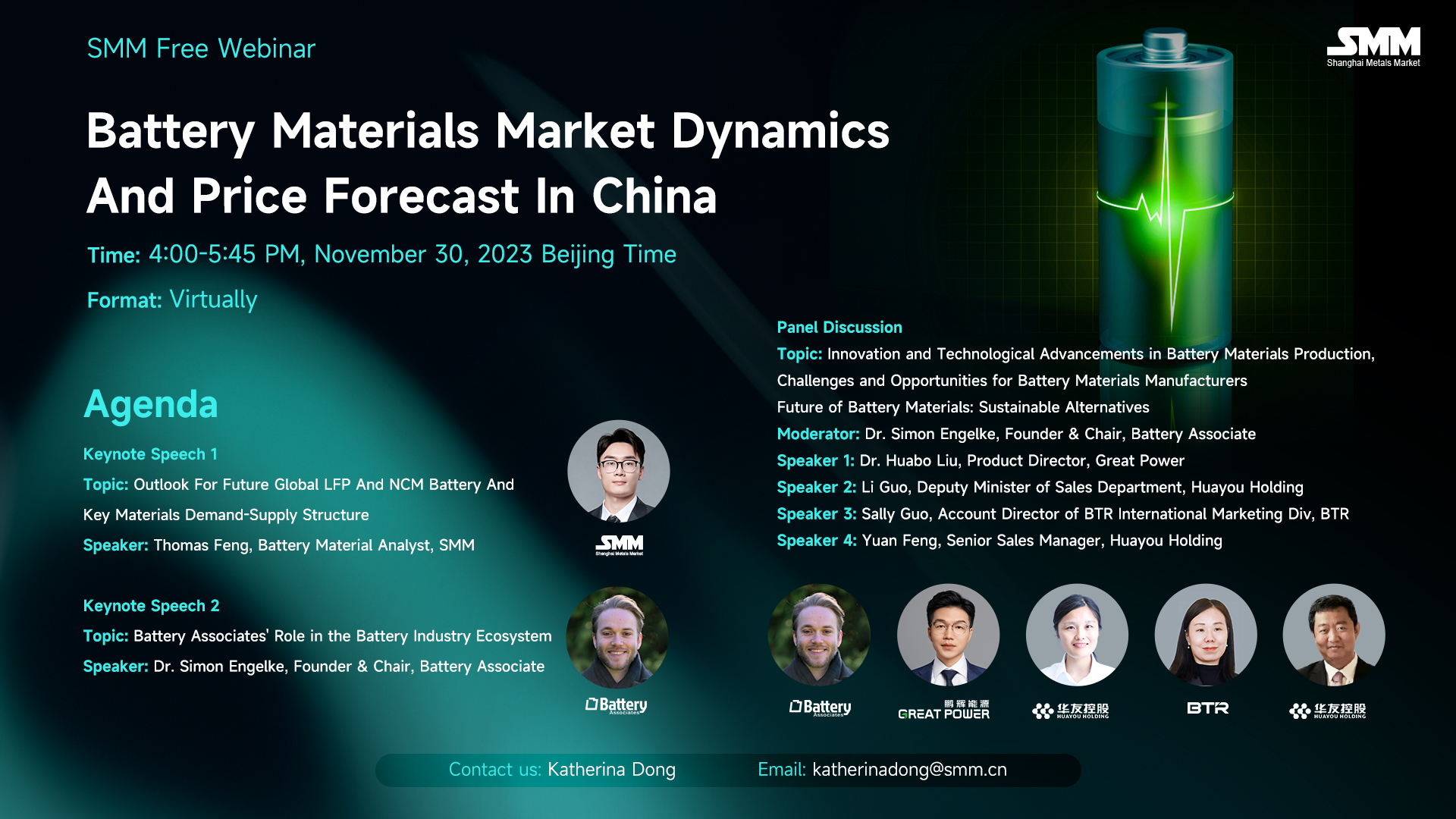

WebinarNov 30, 16:00 - 23:59 (GMT+8)

WebinarNov 30, 16:00 - 23:59 (GMT+8) WebinarAug 22, 16:00 - 23:59 (GMT+8)

WebinarAug 22, 16:00 - 23:59 (GMT+8)