Price

News

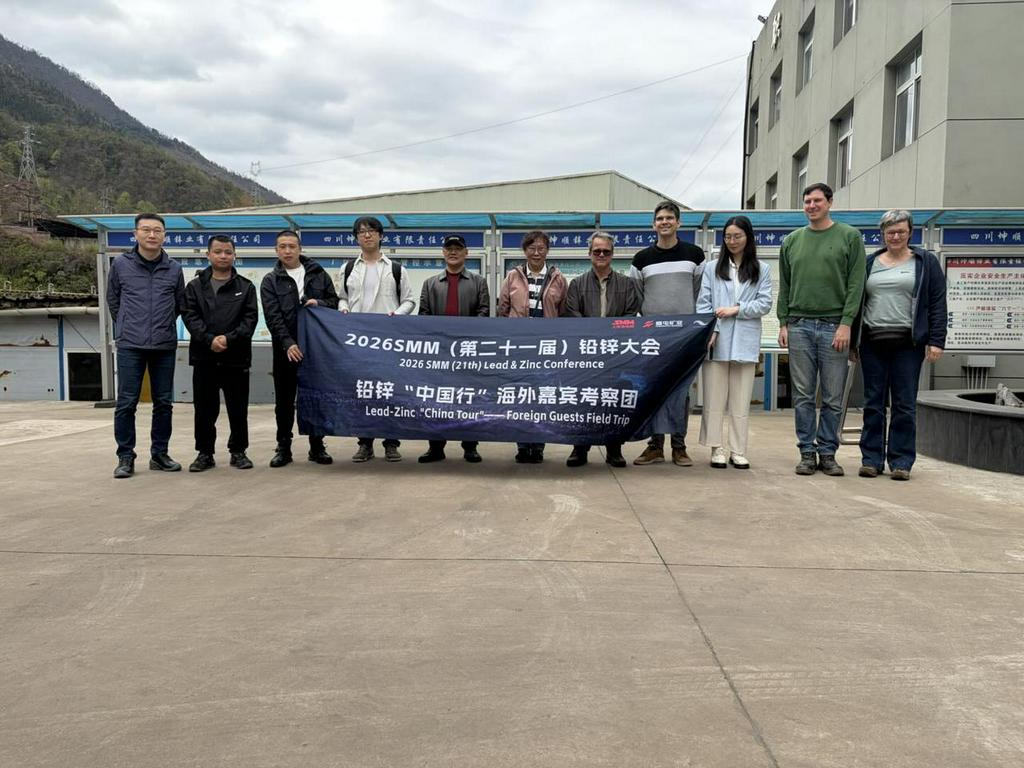

Post-Conference Tour: Connecting Global Lead-Zinc Giants with Key Chinese Players

Post-Conference Tour: Connecting Global Lead-Zinc Giants with Key Chinese PlayersThe 2026 SMM (21st) Lead & Zinc Conference and Industry Expo opened grandly at Howard Johnson Agile Plaza in Chengdu, Sichuan during March 25–27 2026. Organized by SMM, the event brought together global enterprises, professional experts and industry peers from across the entire lead and zinc supply chain. Participants focused on industry hot topics, analyzed market trends and explored development strategies, establishing a highly efficient platform for communication and collaboration to support high-quality growth of the sector. To further strengthen the overseas delegation’s comprehensive understanding of China’s lead and zinc industrial chain and build closer connections between international industry peers and key producers in China, SMM led a high-level overseas delegation on a multi-day industrial tour starting on the afternoon of March 27. The delegation included representatives from global giants, such as Nyrstar, a top European lead and zinc smelting firm, Nexa Resources, a South American giant in lead-zinc mining and smelting, and Befesa, a pioneer in zinc recycling. During the tour, the delegation visited 8 Chinese enterprises. including: COSCO Shipping Sichuan Chengtun Zinc & Germanium Technology Sichuan Kunshun Zinc Industry Yunnan Luoping Zinc & Electricity Hongzhou Hongqian Nonferrous Chemical Yunnan Zhenxing Industrial Group Mengzi Mining & Metallurgy Danxia Smelter of Shenzhen Zhongjin Lingnan Nonfemet The delegation members went deep into production sites, held in-depth discussions and exchanges, and gained a full picture of China’s lead and zinc industry in terms of production operations, technological innovation, capacity scale and market layout, greatly enhancing their insight into and understanding of the entire industrial chain. SMM has systematically compiled detailed information of all enterprises that were visited during this tour, with details below: COSCO Shipping On the afternoon of March 27, the delegation visited COSCO Shipping for an exchange, where they received a warm welcome from the company's leadership. Both sides engaged in discussions on topics such as equipment transportation and technological upgrades. Sichuan COSCO Shipping Logistics Supply Chain Management Co., Ltd. is a wholly-owned subsidiary of COSCO Shipping Logistics Supply Chain Co., Ltd., registered and established in Chengdu, Sichuan Province, with an investment of 30 million yuan. COSCO Shipping Logistics Supply Chain Co., Ltd. is affiliated with China COSCO Shipping Corporation Limited and serves as a core member of the "shipping, ports, and logistics" segment of COSCO Shipping Group, as well as an important component of its global digital supply chain system. The company operates warehouse space exceeding 6 million m², including 19 futures delivery warehouses. China COSCO Shipping Corporation Limited is a globally leading shipping enterprise group, with a combined fleet capacity of 130 million DWT across 1,535 vessels, ranking first in the world. Sichuan COSCO Shipping Logistics Supply Chain Management Co., Ltd. holds business qualifications and an operational scope covering multiple transportation modes including sea, land, air, and rail, providing comprehensive logistics services spanning both international and Chinese markets. Since entering the non-ferrous metals delivery warehouse business in 2016, the company has adhered to the principle of "client-centered and market-oriented," continuously enhancing its service capabilities and achieving steady business growth. Currently, at key logistics periods such as Shanghai Baoshan, Shanghai Yangshan, and Yixing in Jiangsu, the company successfully operates delivery warehouses designated by the Shanghai Futures Exchange for copper, nickel, zinc, and other products. It has become one of the three major non-ferrous metals warehouses of SHFE and was honored with the title of "Top Ten Designated Non-Ferrous Metals Delivery Warehouses" by the Shanghai Futures Exchange for two consecutive years. Sichuan Chengtun Zinc & Germanium Technology Co., Ltd. On March 28, the delegation visited Sichuan Chengtun Zinc & Germanium Technology Co., Ltd. (Shimian City). Both sides engaged in in-depth exchanges on the development of the zinc smelting industry, with a focus on thorough discussions regarding product processing, production techniques, capacity scale, market trends, and the current challenges facing the industry. Sichuan Chengtun Zinc & Germanium Technology Co., Ltd. was established on December 6, 2015, with a registered capital of 1.6 billion yuan. The company has an annual capacity of 300,000 mt of electrolytic zinc, 150,000 mt of sulphuric acid, 400,000 mt of electrolytic zinc waste residue processing, and 40 mt of high-purity germanium dioxide. On January 16, 2019, the company was approved by the China Securities Regulatory Commission and merged into the publicly listed firm Chengtun Mining Group Co., Ltd. The company's main business includes smelting and R&D of zinc-germanium series products, as well as comprehensive recovery of multiple metals. It has formed a complete industry chain from zinc concentrates entering the plant to finished products leaving the plant. Its production lines include zinc calcine, electrolytic zinc, electrolytic zinc waste residue processing, and comprehensive recovery of rare and precious metals. Sichuan Kunshun Zinc Industry Co., Ltd. (Shimian City) On March 28, the delegation headed to Sichuan Kunshun Zinc Industry Co., Ltd. (Shimian City) for a visit and exchange, where they received a warm reception from the enterprise. Both parties held in-depth discussions and exchanges on zinc smelting, covering topics such as production costs, production and market landscape, raw material procurement and processing, industry chain competitive advantages, and distinctive process technologies. Sichuan Kunshun Zinc Industry Co., Ltd. is a specialized and green environmental protection enterprise jointly invested and established by Sichuan Metallurgical Holding Group Co., Ltd. and Shimian Dongshun Zinc Industry Co., Ltd. to implement the national green production philosophy, actively develop the circular economy, and promote the comprehensive utilization of solid waste resources. It integrates solid waste treatment, recycling, and resource regeneration. The company primarily uses high-tech methods to carry out clean utilization and harmless treatment of heavy metal-containing waste generated by industries such as metallurgy and chemicals, eliminating the environmental impact of heavy metal solid waste at the source. The company was established in 2021 and is located in Zhuma Industrial Park, Shimian County, Ya'an City, Sichuan Province, covering an area of 65 mu with a total investment of 180 million yuan. The company has built a 3.5m × 50m Waelz rotary kiln production line, equipped with advanced and well-established low-grade zinc oxide production technology, achieving a resource recovery utilization rate of over 95% and effectively managing waste gas, noise, solid waste, and groundwater risks. It is also equipped with supporting facilities including desulphurization, denitrification, and flue gas defogging towers, as well as a wastewater treatment station, raw material warehouse, raw material pre-washing workshop, water slag processing workshop, biomass semi-gasification furnace, zinc crystallized salt workshop, production safety and environmental protection center, and laboratory for detection and testing. The company holds qualifications for treating hazardous waste categories including HW12, HW17, HW23, HW48, and HW49, with an annual capacity to process 100,000 mt of zinc-containing waste. Its main products include low-grade zinc oxide and zinc crystallized salt. The company has always upheld the green and environmentally friendly development philosophy, adhering to the fundamentals of "being responsible for the environment, for clients, and for employees," guided by technological innovation, and targeting the "reduction, recycling, and detoxification" of solid waste pollution prevention and control. The company is committed to building a modern "solid waste" management and disposal service provider, actively carrying out emergency environmental protection disposal, proactively assuming social service functions, and making positive contributions to promoting the circular economy development in Sichuan and strengthening the ecological civilization construction of lucid waters and lush mountains! Yunnan Luoping Zinc & Electricity Co., Ltd. (Qujing City) On March 30, the delegation visited Yunnan Luoping Zinc & Electricity Co., Ltd. (Qujing City) for exchanges. During the meeting, both sides conducted in-depth discussions on key topics including magnesium removal process optimization, production management organization, and raw material substitution plans, and put forward constructive suggestions on improving the plant environment. Yunnan Luoping Zinc & Electricity Co., Ltd. was established to fully leverage Luoping's local hydropower and lead-zinc mineral resource advantages. In accordance with the "ore, electricity, and smelting integration" development strategy proposed by the Luoping County Party Committee and County Government, and the overall requirements of the Municipal Party Committee and Municipal Government for the reform of industrial enterprises across the city, the company was registered and established at the Yunnan Provincial Administration for Industry and Commerce on December 21, 2000. It was listed on the Shenzhen Stock Exchange A-share market in 2007 and is a state-controlled enterprise under Luoping County. The company's assets are an optimized combination of three components: hydropower, lead-zinc mines, and zinc smelting. In terms of company assets, they are primarily composed of three advantageous resources of Luoping: mineral, hydropower, and zinc smelting. These mainly include six production units: Luoping County Fule Lead-Zinc Mine with an annual processing capacity of 100,000 mt of raw ore, Lazhuang Power Plant with annual power generation of 250 million kWh (installed capacity of 60,000 kW), a zinc smelter with an annual output of 120,000 mt of electrolytic zinc, a zinc powder plant with an annual output of 12,000 mt of ultra-fine zinc powder, a comprehensive utilization plant with an annual processing capacity of 129,500 mt of zinc slag, and a sulphuric acid plant with an annual output of 140,000 mt of sulphuric acid, achieving a total annual industrial output value exceeding 2 billion yuan. The company has six wholly-owned subsidiaries. The company's main businesses include hydropower generation, mining of lead, zinc, and other non-ferrous metals, as well as the production and sales of zinc smelting and its extended products. It is currently the only publicly listed firm in China's zinc smelting industry that integrates mining, power generation, chemical processing, and smelting. Its products include zinc sulphide concentrates, lead concentrates, zinc ingots, industrial sulphuric acid, ultra-fine zinc powder, cadmium, germanium concentrates, silver concentrates, copper concentrates, zinc alloys, industrial and residential electricity, edible oils and fats, among others. Its main product, "Jiulong" brand zinc ingots, is popular in non-ferrous product markets in and outside China thanks to its superior product quality and corporate reputation. Honghe Prefecture Hongqian Non-ferrous Chemical Joint-Stock Co., Ltd. On March 31, the delegation visited Honghe Prefecture Hongqian Non-ferrous Chemical Joint-Stock Co., Ltd. for exchanges. The two sides held in-depth discussions on topics including the economic benefits of smelting by-products, energy utilization efficiency, the current status of enterprise development, and future cooperation intentions. Honghe Prefecture Hongqian Non-ferrous Chemical Joint-Stock Co., Ltd. was established on August 1, 2007, with a registered capital of 50 million yuan. The total investment in project construction was 475.5543 million yuan. The company currently has over 600 employees and covers an area of 443 mu. The plant is located in the Heishenmiaobo Industrial Zone, situated in the central area of the Gejiu-Kaiyuan-Mengzi urban cluster. The company is a new-type joint-stock enterprise centered on crude lead smelting, integrating sulphur dioxide acid production, waste heat power generation, lead electrolysis, and recovery of precious and rare metals such as gold, silver, antimony, and bismuth, with further extension into deep processing of lead-series products including red lead, massicot, electrode plates, and storage batteries. It is a benchmark enterprise among private lead smelters in the city, featuring a relatively large scale, advanced technology, compliance with environmental protection standards, comprehensive utilization of resources, and a complete industry chain. The company pioneered the application of new technologies to upgrade and transform the traditional crude lead smelting model among private enterprises in the city. The company has formulated the working philosophy of "prioritizing environmental protection, ensuring safety, attracting talent, enforcing strict management, and enhancing efficiency," and continues to drive high-quality development. In April 2007, the company commissioned China ENFI Engineering Technology Co., Ltd. to conduct a feasibility study on the lead smelting technological transformation project, and determined a comprehensive industrial facility technological transformation project with a total investment of 490 million yuan and an annual capacity of 60,000 mt of crude lead. On December 21, 2009, the "Demonstration Project of Oxygen-Enriched Bottom-Blowing Lead Smelting Technology with Annual Output of 60,000 mt of Crude Lead" was designated by the Provincial Department of Science and Technology as a 2009 Yunnan Provincial Science and Technology Innovation Project. In 2010, it was further designated as a key industrial project by the provincial, prefectural, and municipal governments. On November 14, 2011, the company obtained ISO9001:2008 quality management system certification. On March 7, 2012, "HSPb99.94PCT" was successfully registered on the London Metal Exchange. In 2019, the company successively passed the safety completion acceptance and environmental impact assessment completion acceptance, fully achieving compliant operations and sustainable development. Yunnan Zhenxing Industrial Group Co., Ltd. On March 31, the delegation headed to Yunnan Zhenxing Industrial Group Co., Ltd. for a visit and exchange. Both parties conducted in-depth discussions on topics including Yunnan Province's mineral resource endowment, smelting industry development trends, corporate business strategies, and technological innovation applications, jointly assessing the current status and prospects of the industry and analyzing the challenges and opportunities ahead. Yunnan Zhenxing Industrial Group Co., Ltd. (hereinafter referred to as "the Group") was founded in 1996 and is located in the Chongposhao New Materials Industrial Park, Shadian Sub-district Office, Gejiu City. The Group currently has 7 subsidiaries, 2 holding companies, and 1 equity-participation company, with approximately 3,000 employees. Its capacity reaches annual output of crude lead (100,000 mt), electrolytic lead (60,000 mt), zinc ingot (20,000 mt), lead-acid battery plates (9 million sets), lead-acid batteries (6 million units), superphosphate (350,000 mt), sulphuric acid (200,000 mt), and monoammonium phosphate (MAP) (60,000 mt). The Group has established five major production sites and five major product brands covering crude lead raw material, lead-zinc smelting, power supply manufacturing, fertilizer and chemical production, and resource recovery. It has formed an internal industrial cycle spanning lead ore mining—lead-zinc smelting—lead-based alloy melting—battery manufacturing—waste battery recycling—precious metals production, making it one of the few private non-ferrous enterprises in China with a complete lead industry chain. Since 2013, the Group has been consecutively recognized as one of the Top 100 Non-Public Enterprises in Yunnan Province. In 2025, it ranked 41st among the "Top 100 Non-Public Enterprises in Yunnan Province" and was selected for the first time into the "Top 20 Private Enterprises in Innovation Capability," ranking 7th. Yunnan Shadian Lead Industry Co., Ltd., a subsidiary controlled by the Group, ranked 71st. The Group has received nearly 100 honors at various levels, including "High-tech Enterprise," "Outstanding Private Technology Enterprise," "Enterprise with Harmonious Labor Relations," "Provincial Model Collective for Ethnic Unity and Progress," and "Key Enterprise for Industrial Development in Honghe Prefecture" in Yunnan Province. The Group's Yunsha brand lead ingot was successfully registered on the London Metal Exchange in 2007 and on the Shanghai Futures Exchange in 2020. In 2021, the Group was rated AAA in enterprise credit rating in the national non-ferrous metals industry. In August 2024, it was designated as a "Qiangyuan Zhuqi" Industry-Finance Service Base by the Shanghai Futures Exchange. Looking ahead, the Group will pursue the philosophy of "seeking survival, pursuing development, and accelerating enterprise transformation and upgrading," adhering to the working approach of "rooting in Honghe, basing in Yunnan, radiating to surrounding regions, and expanding across China." It will thoroughly implement strategies of enterprise management transformation, technology-driven development, talent empowerment, and sustainable development, striving to achieve significant increases in capacity and production of major products by 2035, with gross industrial output value up YoY, and to build itself into a 10 billion green lead-zinc comprehensive recycling technology enterprise. Mengzi Mining and Metallurgy Co., Ltd. On March 31, SMM and the field trip delegation headed to Mengzi Mining and Metallurgy Co., Ltd. for a visit and exchange. Both parties engaged in in-depth discussions on the entire zinc smelting process, covering topics including production technology, raw material supply, product sales, environmental protection governance, and future development plans, aiming to share experience, address industry pain points, and jointly clarify the direction of development. Mengzi Mining and Metallurgy Co., Ltd. was established in 1996. It is a resource-based mining and metallurgy enterprise integrating R&D, exploration, mining, mineral processing, smelting, and trading, with a focus on comprehensive utilization of resources. The company is one of the few comprehensive private enterprises in the non-ferrous metal industry that possesses an entire industry chain and operates independent trading and supply chain business platforms. It is among the top 100 enterprises in Yunnan Province and a key enterprise in Honghe Prefecture. Shenzhen Zhongjin Lingnan Nonfemet Co., Ltd. — Danxia Smelter On April 2, the SMM delegation visited Zhongjin Lingnan's Danxia Smelter for a survey and field trip to the core plant area. In-depth discussions were held on production operations, technological R&D, and raw material procurement, covering key topics such as production capacity, technical cooperation, and raw material procurement strategies. Shenzhen Zhongjin Lingnan Nonfemet Co., Ltd. (hereinafter referred to as "Zhongjin Lingnan") was established in September 1984 and listed on the Shenzhen Stock Exchange in January 1997 (stock code: 000060). It is an internationalized entire industry chain resource company primarily engaged in lead, zinc, and copper mining, mineral processing, and smelting, as well as comprehensive recovery of rare, scattered, and precious metals. It is a publicly listed firm controlled by Guangsheng Holdings Group, a key wholly state-owned enterprise under Guangdong Province. Zhongjin Lingnan's business covers segments including mines, smelting, new materials, and supply chains. It has 23 directly affiliated enterprises, wholly-owned and controlled subsidiaries. Major operating entities include Fankou Lead-Zinc Mine, Shaoguan Smelter, Danxia Smelter, Zhongjin Copper Co., Guangxi Mining Co., Perilya Limited in Australia, Zhongjin Technology Co., and Huajiari Co. The company has an annual output of 300,000 mt of lead and zinc metal content in concentrates, 450,000 mt of smelted lead and zinc products, 450,000 mt of copper cathode, 21,000 mt of aluminum extrusion, 20,000 mt of battery zinc powder, and 5,400 mt of composite metal materials. Among these, its battery zinc powder ranked first in Chinese market share, nickel-metal hydride and nickel-cadmium battery electrode sheets & plates materials ranked first in Chinese market share, and thermal bimetal ranked first in Chinese market share. The 2026 field trip brought together some global lead and zinc industry leaders for an inspiring and highly productive journey across China’s leading smelters and enterprises. The warm welcome, operational excellence, and innovative technologies on display made this event a resounding success — and we extend our deepest gratitude to all the companies and participants who made it happen. Looking ahead – Save the date for 2027: We are excited to announce that the 2027 SMM (22nd) Lead & Zinc Conference and Industry EXPO will take place from March 17–19, 2027 in Kunming, Yunnan, China . This premier event will once again bring together the global lead-zinc community for high-level networking, insight sharing, and industrial exploration. Interactive call – We want to hear from you: As we plan the field trip for the 2027 conference, we’d love your input. Which smelters or companies would you most like to visit for technical exchange and on-site learning? Please share your suggestions in the comments below — your feedback will help shape the 2027 experience. Let us know where the industry should go next!

Apr 7, 2026 14:32- Is Support for SHFE Tin Hard to Find Amid Expected Improvement in Tin Ore Supply? [Wenhua Observation]

At the beginning of April, SHFE tin prices fell sharply under pressure due to the escalation of trade conflicts. However, as tariffs were suspended, tin prices rebounded, recovering previous losses and returning to levels before the supply disruptions of tin ore in the DRC. Nevertheless, the market reacted strongly to rumors last week about production resumptions and fee payments in the Wa region, causing tin prices to break through support levels and continue to weaken at the beginning of this week, with the most-traded contract falling below the 250,000 mt threshold. Currently, these market rumors remain unverified. According to SMM, few enterprises are paying fees to obtain mining licenses, with many adopting a wait-and-see attitude, and most major mining traders have not paid management fees. Moreover, the current inspections at the China-Myanmar border are stringent, and the entry procedures for most large-scale equipment and relevant mining personnel are complex. Therefore, the current pace of production resumptions in the Wa region may fall short of market expectations. So, does the current tin price still have the momentum to continue declining? Tight Actual Supply of Tin Ore, with Increasing Expectations for Future Increases In recent years, speculation on SHFE tin has mainly revolved around supply, as tin is a relatively scarce metal with limited content in the Earth's crust and a high degree of supply concentration, primarily distributed in China, Indonesia, Myanmar, Australia, and other regions. After Myanmar suspended tin ore mining on August 1, 2023, global tin resources have been in a relatively tight supply situation. Consequently, the market is highly sensitive to supply-side information, with any slight changes triggering significant market fluctuations. In the early stages of Myanmar's mining ban, China's tin ore imports remained at a relatively high level due to the availability of ore inventory for export. However, as inventory was depleted, China's tin ore imports plummeted from Q2 last year, and the issue of tight domestic tin ore supply has become increasingly prominent. During this period, Chinese enterprises actively sought alternative resources from other countries. However, due to limited global new tin ore discoveries in recent years, the tight resource situation has not been alleviated. Among them, the Bisie mine, owned by Alphamin in the DRC, is the largest mine in Africa and the third largest globally. The mine has two projects: the Mpama North project operates steadily, while the Mpama South project commenced production on May 17 last year, making it the largest among the newly commissioned projects last year. Tin ore from the DRC has also become an important source of tin ore imports for China, currently accounting for about 30%. Production at the Alphamin mine was suspended for over a month in March due to local armed conflicts but gradually resumed in early April. The production interruption at the Alphamin mine, which only recovered about 1,290 mt of tin metal, may result in a supply gap of approximately 2,000-3,000 mt. Currently, Alphamin has revised its tin production guidance for the 2025 fiscal year downward from 20,000 mt to 17,500 mt. Since the beginning of this year, the resumption of tin ore production in Myanmar has gradually been put on the agenda. On February 26, the Wa State Industrial and Mineral Resources Administration issued the document "Procedures for Applying for Mining, Beneficiation Plant, and Prospecting Licenses," which explicitly stipulated the process for applying for licenses in mining areas. On the morning of April 23, 2025, the Wa State Industrial and Mineral Resources Administration held a special symposium on the resumption of production at the Mansang mine. The meeting announced relevant documents and clarified the work procedures. However, after the symposium, the authorities had not yet issued a clear signal for a full resumption of production. On May 27, market news emerged that the first batch of tin ore from Myanmar's Wa State had reportedly obtained export licenses, but the authenticity of the rumors was questionable. Even if production resumption were confirmed, the first batch of tin ore would not enter the market until at least the end of June. Currently, tin ore supply is tight, and domestic tin concentrate treatment charges (TCs) remain at historically low levels. As of May 30, the tin concentrate TC for 40% grade ore in Yunnan was 11,000 yuan/mt, and for 60% grade ore in Jiangxi, Guangxi, and Hunan was also 11,000 yuan/mt, approaching the cost line of smelters and severely squeezing profit margins. The shortage of raw material supply has affected the production of smelters. According to SMM data based on market-adjusted processing figures, in May 2025, China's refined tin production decreased by 2.37% MoM and 11.24% YoY. The continuous tightening of the tin concentrate and scrap tin supply chains has imposed rigid constraints on capacity, leading to a slight decline in the overall operating rate of domestic smelters. As of May 30, the operating rates of refined tin smelters in Yunnan and Jiangxi, two major tin-producing provinces, remained at low levels, with a combined operating rate of 54.58%. Regionally, in Yunnan, the shortage of raw materials and cost pressures are intertwined. Raw material inventories at Yunnan smelters are generally below 30 days, with some enterprises facing inventory backlogs due to high-priced stockpiling in the early period. However, weak downstream demand has made it difficult to sell goods, resulting in sluggish spot premium transactions. Some smelters in core production areas such as Gejiu have entered seasonal maintenance or production cuts due to raw material shortages and cost pressures. In Jiangxi, since the beginning of the year, the local scrap tin recycling volume has consistently been below 70% of the annual average, mainly due to the US imposing high tariffs on Chinese electronics, leading to a contraction in solder export orders and a reduction in scrap sources. Some enterprises have been forced to implement long-term production cuts due to insufficient scrap, with some capacity potentially exiting the market permanently. In Inner Mongolia, production slightly rebounded in May due to production issues at captive mines, but it has not yet returned to previous levels. Production areas such as Anhui have continued to experience operating rates below expectations due to shortages of scrap and tin concentrates. Based on SMM estimates, refined tin production is expected to decrease by 4.58% MoM in June, with some smelters in Yunnan and Jiangxi planning to halt production for maintenance. Overall, tin ore supply in June is unlikely to see significant recovery. However, the period of the tightest global tin supply is about to pass, and the market will enter a verification phase for the improvement of the supply-demand gap. Close attention should be paid to the return of tin ore from Africa and the resumption progress of tin ore production in Myanmar. There is a lack of significant incremental demand in the downstream sector. Global semiconductor sales exhibit cyclical changes. The current semiconductor cycle bottomed out in February 2023, with YoY growth in sales turning positive in November 2023. Since then, the growth rate has been climbing, but it gradually slowed down after October 2024. Currently, the absolute amount of global semiconductor sales remains at a high level. Sales began to pull back slightly from December 2024 and saw a slight MoM rebound in March 2025. This global semiconductor cycle is driven by AI computing power construction, primarily in advanced manufacturing processes. Therefore, the core beneficiaries are concentrated overseas, while domestic capacity is mainly in mature manufacturing processes, offering limited impetus. The downstream semiconductor industries in China are more concentrated in areas such as consumer electronics and automotive. From January to April 2025, domestic mobile phone shipments reached 94.708 million units, up 3.5% YoY. Overall, China's policy subsidies have further boosted market consumption, and the Chinese smartphone industry has shown steady growth from January to April 2025. The recent 618 shopping festival has already kicked off and is expected to support stable end-use consumption electronics. However, the market is expected to gradually enter the off-season for demand in July and August. Enterprises may slow down their stockpiling pace, and it is anticipated that downstream demand for raw materials such as tin will also drop back slightly. Whether there will be an outperformance in demand this year remains to be seen, depending on whether AI blockbuster products emerge in the consumer electronics sector. In recent years, the new demand for tin solder has mainly been reflected in PV solder, currently accounting for over 10%. According to data released by the National Energy Administration, the installed power generation capacity for solar energy from January to April 2025 was 990 million kW, up 47.7% YoY. The significant growth in new PV installed capacity is primarily driven by the installation rush driven by policy timelines. In January 2025, the National Energy Administration issued the "Administrative Measures for the Development and Construction of Distributed PV Power Generation," clarifying that April 30, 2025, is the demarcation point for the implementation of new and old policies. Existing projects that completed their filings before this date will still enjoy the original subsidy and grid connection policies, while new projects will fully implement market-based rules thereafter. On February 9, 2025, the National Development and Reform Commission (NDRC) and the National Energy Administration jointly issued the "Notice on Deepening the Market-Oriented Reform of New Energy On-Grid Tariffs to Promote High-Quality Development of New Energy." Starting from May 31, 2025, incremental distributed PV projects will fully enter the market. All new projects will, in principle, have their entire electricity output traded in the power market, with electricity prices formed through market bidding, and subsidies will completely exit the historical stage. Meanwhile, a "price settlement mechanism for the sustainable development of new energy," namely, a "refund for excess, supplement for shortfall" differential settlement mechanism, has been established to stabilize revenue expectations. To capitalize on the two major policy periods of "430" and "531," downstream enterprises initiated an installation rush, driving a significant YoY increase in domestic newly installed PV capacity in April. However, projects connected to the grid after May 31, 2025, are required to fully comply with the new regulations. It is expected that the growth rate of PV installation capacity will subsequently slow down, which will also drag down the demand for tin. Meanwhile, market consumption in traditional sectors such as tinplate and PVC heat stabilizers remains stable. Downstream enterprises are highly sensitive to price changes. Recently, with the decline in tin prices, market sentiment for stockpiling has improved, and downstream procurement demand has rebounded. However, finished product inventories in some markets remain at relatively high levels, ultimately limiting the boost to raw material procurement by downstream enterprises driven by growth in end-user market demand. Overall, the increase in tin concentrates in June is expected to be relatively limited, so the supply will remain slightly tight in the short term. However, the supply of raw materials is expected to gradually improve, and the market will subsequently enter a verification period for the improvement of the supply-demand gap. Close attention should be paid to the return of tin ore from Africa and the production resumption progress of tin mines in Myanmar. On the demand side, the market is about to enter the off-season, with weak expectations for demand growth, making it difficult to effectively boost tin prices. Therefore, in the short term, under the expectation of increased supply, there may be downward pressure on the central tendency of the market, but constrained by the current situation where the shortage of tin ore has not significantly eased, market trends may fluctuate. However, from a long-term perspective, the AI industry cycle has not yet ended. If there is a surge in demand from AI end-users, it is expected to significantly drive up tin demand. At that time, the growth rate of supply may lag behind the resilience of demand, and the downside room for tin prices in the medium and long term will be limited. Nevertheless, there is still uncertainty in current trade policies, and caution should be exercised against significant disruptions to tin prices caused by macro factors. (Wenhua Comprehensive)

Jun 4, 2025 09:43 - LME tin and SHFE tin prices fall for two consecutive months on monthly chart [SMM Monthly Outlook]

Weak supply and demand in fundamentals, short-term fluctuations in tin prices, "waiting for the wind" - macro factors may become the key to breaking the deadlock!

May 31, 2025 19:20 - LME and SHFE tin prices have declined for two consecutive months. Amid intensifying macroeconomic competition, the pace of production resumptions in major producing regions has become the core variable influencing tin price trends [Monthly Outlook]

[SMM Monthly Outlook: LME and SHFE Tin Prices Decline for Two Consecutive Months; With Intensified Macroeconomic Game, the Pace of Production Resumptions in Major Producing Regions Becomes the Core Variable Affecting Tin Price Trends] Unlike the sharp decline in tin prices in April, tin prices in May generally fluctuated rangebound. As May month-end approached, despite the short-term tight supply situation of tin ore not yet improving, market expectations for supply recovery due to the gradual resumption of production at tin mines in Myanmar's Wa region and the DRC increased. Additionally, uncertainties surrounding the US tariff policy led to a cooling of market risk appetite, resulting in a significant correction in tin prices. As of around 18:10 on May 30, LME tin fell by 1.56% to $30,750/mt, with a temporary monthly decline of 1.91% in May; SHFE tin dropped by 2.87% to 250,300 yuan/mt, with a monthly decline of 4.39% in May.

May 30, 2025 20:09 - [SMM Analysis] Some refined tin smelters in Yunnan gradually resumed production, while production in Jiangxi held stable

According to the SMM survey, the combined operating rate of refined tin smelters in Yunnan and Jiangxi in the week ending May 31 was 64.39%, a slight rebound WoW.

Jun 4, 2024 14:06 - [SMM analysis] Some refined tin smelters in Yunnan suspended production for maintenance, while production in Jiangxi remained stable

According to SMM, the combined operating rate of refined tin smelters in Yunnan and Jiangxi last week decreased to 63.77%.

May 28, 2024 10:58