171results found for 'Capacity and Production'

Price

News

- When Nickel from "Resource Surplus" Meets "Policy Tightening"—2026 H1 Nickel Price In-depth Review and H2 Outlook

I. Key Points In H1 2026, nickel prices exhibited wide fluctuations characterized by a “rebound from lows—consolidation at highs—pullback and consolidation” pattern. The most-traded LME nickel contract surged from $14,000/mt at the beginning of the year to near $20,000 in May, before pulling back to $16,000-17,000 in July; the most-traded SHFE nickel contract climbed from 110,000 yuan/mt to above 150,000 yuan/mt, and then retreated to 125,000-130,000 yuan/mt. The driving logic of this market move was the intertwined resonance of three main themes: a shift in Indonesia’s resource policies, repeated fluctuations in global macro liquidity expectations, and the impact of geopolitical conflicts on raw material costs. The center of nickel prices did rise compared to 2025, but the “shadow of surplus” has not dissipated. In H2 2026, the key variables for tracking nickel prices are as follows: First, the approval results of Indonesia’s RKAB quota revision in July. A significant increase in the quota would substantially narrow the supply deficit and weigh on nickel prices. Second, the Fed’s policy path — whether the hawkish signal from the June dot plot will persist — which affects the US dollar index and the valuation center of commodities. Third, sulphur supply and the situation in the Strait of Hormuz, which determines the cost support strength along the MHP–nickel sulphate–refined nickel chain. Fourth, demand from stainless steel and NEV ternary power batteries. Fifth, the pace of global visible inventory destocking. Sustained destocking would serve as a real support signal, while high inventories would limit price elasticity. Under a neutral scenario, LME nickel prices are expected to trade in the range of $15,500-17,500/mt in H2. II. Macro Environment – Reversal of Liquidity Expectations, Substantial Impact of Geopolitical Costs, and the ‘Dual Strength’ Pattern of the RMB 1. Fed Policy Path: ‘From Dovish to Hawkish’ At the beginning of the year, the market widely expected 50-100 bp of rate cuts in H1 2026, and the US dollar index fell below 97 at one point, creating a relatively loose liquidity environment. However, mid-year, new Fed Chair Kevin Warsh’s hawkish stance surprised the market. The June meeting kept rates unchanged and the dot plot signaled a bias toward rate hikes, leading to a systematic revision of the previously priced “dovish delivery” logic. This directly weighed on the valuation of industrial metals such as nickel, serving as a key macro trigger for the nickel price decline in June. 2. Geopolitical Conflicts Expanded from ‘Safe-Haven Trades’ to ‘Real Cost Shocks’ The Middle East situation (tensions among the US, Israel and Iran, and disturbances in the Strait of Hormuz) not only pushed up energy and safe-haven premiums, but also, through the critical link of sulphur supply, directly raised the production cost of Indonesia’s MHP (each mt of MHP in metal content consumes about 10 mt of sulphur), forming the core driver of the pulse-like surge in nickel prices in May. After a ceasefire agreement was reached between the US and Iran in mid-June, energy and safe-haven premiums receded, leading to a peak and subsequent pullback in commodities, confirming the dual impact of geopolitical variables on nickel prices. 3. China’s Macroeconomy and RMB ‘Dual Strength’ Provide a Unique Offset Against a generally stronger US dollar, the onshore RMB bucked the trend, appreciating from 6.98 to 6.79 (a gain of about 2.9%). The relative strength of the RMB, with the exchange rate declining (USD/CNY fell), caused import costs to drop sharply, opening the import window and generating arbitrage profits. However, as large volumes of imported nickel flowed into the domestic market, the spot supply of nickel plates in China increased, accelerating the pace of inventory buildup and weighing on domestic prices. At the same time, LME nickel inventories decreased, leading to a repair of the SHFE/LME nickel price ratio, and the import window closed again in May. III. Indonesia's Industrial Policy—Systemic Transformation from "Expanding Capacity" to "Controlling the Chain to Raise Prices" In H1 2026, Indonesia's nickel industry policy completed a strategic shift, systematically deploying a policy package centered on "controlling supply, stabilizing prices, and enhancing resource added value," which became the core fundamental variable driving wide fluctuations in nickel prices. 1. Significant tightening of total RKAB quotas and tilted allocation structure At the beginning of the year, Indonesia's ESDM announced that the 2026 nickel ore quota would be drastically cut from 379 million wmt in 2025 to 270 million wmt. The world's largest single nickel mine project, WBN, saw its 2026 quota suffer a "cliff-like" reduction; its quota was exhausted in May, leading to full-scale production cuts and shutdowns, stoking persistent concerns over tight supply in H1. The Indonesian authorities have clarified that July 1 to 31, 2026 will be the mid-year application period for supplementary RKAB quotas, prioritizing compliant miners with integrated domestic downstream smelting capacity (such as supporting NPI or HPAL projects). The mid-year policy game over RKAB quotas is intensifying. 2. HPM pricing formula reform shifts from single nickel pricing to multi-element comprehensive pricing The new formula effective April 15 incorporates associated elements such as iron, cobalt, and chromium into the value component for the first time. Indonesia sought to recapture the undervalued value of associated resources into the pricing system, raising benchmark prices for nickel ore and intermediate products across the cost side. However, this reform met strong opposition from the domestic smelting industry, which argued that it would further squeeze smelting profits amid already surging sulfur and energy costs. 3. Indonesian government officially releases new export control regulations for ferronickel (FeNi) and NPI In July, Indonesia further strengthened export supervision of high-value-added nickel products under Finance Minister Regulation (KMK) No.32/MK/BC/2026 (implementing Trade Minister Regulation No.17/2026). The new regulation targets products under HS Code Ex.7202.60.00, including ferronickel (FeNi) ingots and lumps with nickel content ≥8%, sponge ferronickel (Sponge FeNi) and granular ferronickel (Nugget FeNi) with nickel content ≥4%, as well as low-grade ferronickel products with 2% ≤ Ni <4% and iron content ≥75% (covering some NPI products). Export requires a surveyor's report (LS) and relevant export licenses; from January 1, 2027, export will generally only be allowed through state-owned export enterprises (BUMN Ekspor), with exemptions under specific circumstances. Overall, Indonesia is currently tightening quotas, raising taxes and fees, and imposing export controls to elevate resource value, seeking to keep nickel prices within its officially recognized desired range ($19,000-20,000/mt) over the long term. On the other hand, it must balance stability of the industry chain and foreign investor confidence in actual implementation, thus exhibiting a game-like characteristic of "tight first then loose, adjusting while implementing."The extreme policy uncertainty was one of the core reasons behind the wide fluctuations in nickel prices in H1. IV. Changes in Nickel Intermediate Product Raw Materials: Restructuring of the Cost Transmission Chain 1. MHP and High-Grade Nickel Matte: A Dynamic Game Dominated by "Auxiliary Material Costs" There are three main production routes for nickel sulphate raw materials: MHP (hydrometallurgy): the dominant route with the largest long-term growth, but highly dependent on sulphur; high-grade nickel matte (pyrometallurgy RKEF conversion / oxygen-enriched side-blowing route): an alternative route with low dependence on sulphur and relatively stable cost elasticity; nickel briquette dissolution: the least economical, feasible only within specific price spread windows. The sharp fluctuations in sulphur prices in H1 reshaped the cost structure of the entire nickel industry chain. Producing one mt in metal content of MHP requires approximately 10 mt of sulphur, while tensions in the Strait of Hormuz disrupted Indonesia’s sulphur import channels, forcing Huayou Cobalt’s Huafei Nickel-Cobalt to cut production on some lines starting in May. Sulphur prices surged, with the SMM sulphur CIF Indonesia price peaking at $1,300/mt, and the cost shock was transmitted step by step along the “sulphur—MHP—nickel sulphate—electrodeposited nickel” chain, becoming one of the core drivers behind the rapid nickel price rise in May. The high-grade nickel matte route, relying on pyrometallurgy, is far less dependent on sulphur than MHP. Consequently, during the sulphur price spike, high-grade nickel matte’s cost advantage over MHP widened significantly, creating direct substitution pressure on MHP’s market share. In terms of production trends, Indonesia’s MHP production edged up about 0.02% YoY to 206,000 mt in metal content in January-June 2026. Over the same period, high-grade nickel matte posted the most impressive growth, with production up about 123% YoY to 185,000 mt in metal content, strengthening its position in the competition for nickel sulphate raw materials. In the medium and long term, however, once sulphur supply normalizes and MHP costs pull back, the MHP route, with its scale effects and relatively mature cost curve, will reclaim its dominant share of the nickel sulphate raw material market; after all, MHP projects’ capacity base is far larger than that of high-grade nickel matte, and its cobalt by-product also provides a substantial marginal revenue contribution (about $4,500/mt Ni). 2. Production Capacity Switching Game Between High-Grade Nickel Matte and NPI High-grade nickel matte and NPI share the same RKEF production lines and laterite nickel ore resources, differing only in whether a sulphidation conversion stage is added at the end. The conversion decision is essentially a profit-maximization problem: when the marginal revenue of high-grade nickel matte relative to NPI covers the additional equipment and process losses of sulphidation conversion, lines switch to high-grade nickel matte; otherwise, they tend toward NPI. The conversion profit chart shows that profit for NPI-to-high-grade-nickel-matte conversion appeared only in April-May. After MHP production cuts in May, the monthly nickel sulphate raw material deficit was about 8,000 mt Ni, theoretically requiring increased high-grade nickel matte production to fill. However, due to RKAB quota constraints and the continued decline in NPI feed grade, integrated enterprises prioritized supplying stainless steel, making it difficult for high-grade nickel matte to offset the MHP raw material shortfall. This was a key reason why nickel sulphate prices remained firm even after refined nickel prices fell sharply in May. 5. Refined Nickel Supply-Demand Pattern: High Inventory vs. Structural Tightness Expectations 1. Supply Side: Electrodeposited Nickel Capacity Continues to Expand, Production Hits Repeated Records The most certain trend on the supply side is the sustained release of electrodeposited nickel capacity and production in China and Indonesia. According to SMM data, from January to June 2026, China’s refined nickel production was 215,000 mt, a YoY growth rate of 9%; Indonesia’s refined nickel production was 56,000 mt, a YoY growth rate of 97%. Meanwhile, at the beginning of 2026, China’s refined nickel trade pattern underwent a temporary reversal. Previously, benefiting from the explosion in electrodeposited nickel capacity, China had once been expanding its net exports of refined nickel. However, entering Q1 2026, as the price spread between Chinese and overseas markets opened up and the import arbitrage window was activated, China turned back into a net importer of refined nickel, with net imports exceeding 80,000 mt in January-April. 2. Demand Side: New Energy Recovery, Stainless Steel Support, and Steady Alloy & Special Steel In H1 2026, stainless steel, the largest downstream application of nickel, maintained mild growth. Total stainless steel production in China and Indonesia from January to June was approximately 23 million mt, up about 2% YoY. Steel mills maintained relatively high operating rates throughout H1, with stable apparent consumption. In the new energy (ternary battery) sector, nickel demand saw a strong recovery. From January to June, China’s ternary cathode precursor production was 528,000 mt, up 32% YoY; ternary cathode material production was 493,000 mt, up 40% YoY. Alloy & special steel and electroplating, although accounting for a relatively low share of total primary nickel consumption, played a critical role in refined nickel demand in H1 due to their irreplaceability. From January to June, China’s total refined nickel demand was approximately 140,000 mt, up 9% YoY. Military and aerospace demand strengthened, while high-end manufacturing demand remained steady with moderate growth. 3. Inventory Side: Global Visible Inventory Remains at Historical Highs Despite wild swings in nickel prices in H1, global visible nickel inventory remained at relatively high historical levels. LME nickel inventory fluctuated in the range of 270,000-280,000 mt for an extended period. China’s social inventory and exchange warrants experienced significant buildup. As of July, SMM refined nickel social inventory reached 130,000 mt, with total global inventory hitting a high of 497,000 mt. High visible inventory posed a significant constraint on nickel price rises. In June, after digesting supply disruption narratives, the market refocused on the fundamental reality of “high inventory and lackluster demand,” and nickel prices pulled back from a temporary high to around $16,100/mt. 6. H2 2026 Risk Alerts and Nickel Price Forecasts Based on the logic of H1, nickel price trends in H2 are expected to maintain a fundamental pattern dominated by policy gaming, with macro factors amplifying volatility. The following variables merit close monitoring: 1. The final outcome of the RKAB quota revision approval in Indonesia in July; 2. whether the US Fed's policy path in H2 will continue its hawkish stance; 3. whether sulfur supply can substantially return to normal, and whether there is a risk of repeated disruptions in the Strait of Hormuz situation; 4. whether end-use demand from stainless steel and new energy sectors can show a substantial improvement; 5. the destocking pace of global visible inventory. Based on the above price influencing factors, a scenario analysis for nickel prices is conducted: Bearish scenario (quotas being more accommodative than expected): quota increase ≥30% + sulfur pullback + high inventory pressure → LME nickel $14,000—$16,000/mt. Neutral scenario (highest probability): quota slightly increased but still tight + sulfur consolidates at highs → LME nickel $15,500—$17,500/mt. Bullish scenario (tight quotas + secondary cost surge): quotas continue to tighten + export controls + repeated geopolitical tensions push up sulfur → LME nickel $17,000—$19,000/mt.

Jul 10, 2026 15:56 - Dispute over Strait Management Rights Continues; Short-term Bearish Factors Dominate Aluminum Price [SMM Aluminum Morning Brief]

[Strait of Hormuz Control Dispute Continues; Bearish Factors Dominate Short-Term Aluminum Prices] The Strait of Hormuz control dispute continues, and the resumption of navigation in the strait remains uncertain. The US Fed’s hawkish pivot boosted the US dollar index, and non-ferrous metal prices were suppressed. Under macro headwinds, aluminum prices in and outside China fell. In the short term, bearish factors dominate, and aluminum prices are expected to remain in the doldrums.

Jun 30, 2026 09:30 - 【SMM Analysis】China's May Ferrochrome Production Surges; Steel Mill Tender Prices Stabilize Short-Term Market Sentiment

According to statistics from SMM, China's output of high-carbon ferrochrome in May 2026 rose by 5.09% month-on-month and 23.85% year-on-year.

May 29, 2026 18:21 - The Sierra Leone New Tonkolili 30 Million mt Magnetic Beneficiation Plant (Phase II) Project Completed and Commenced Production!

On April 29 local time, as hundreds of metric tons of magnetite ore were steadily conveyed to the feed inlet of the primary crushing station, equipment across all workshops of the beneficiation plant operated in synchronized coordination and started up smoothly. The New Tonkolili 30 Million mt Magnetic Beneficiation Plant (Phase II) project, constructed by China Railway No. 1 Group under China Railway Group Limited, was completed and put into operation in Sierra Leone. The New Tonkolili mining area is located in the Northern Province of Sierra Leone, covering an area of 408 square kilometers. It is one of the world's largest single magnetite mining areas by proven reserves, with currently proven reserves of 13.7 billion mt. In April 2025, the Phase I project was completed and put into operation; on January 22 this year, the Phase III project broke ground and is currently under construction. The Phase II project broke ground in April 2025 and was completed in 11 months. With this phase now in operation, the raw ore processing capacity of the beneficiation plant will reach 20 million mt per year, significantly enhancing overall beneficiation processing capacity and production efficiency, and laying the foundation for large-scale and intensive operations. During construction, the project team established a "sea-rail-road" multimodal logistics support system, effectively overcoming the challenges of cross-border transportation of equipment and materials for projects outside China. The team also scientifically optimized construction organization plans, making full use of the prime dry-season construction window to maximize construction efficiency. The completion and commissioning of the New Tonkolili 30 Million mt Magnetic Beneficiation Plant (Phase II) project represented a concrete embodiment of pragmatic cooperation in the mining sector between China and Sierra Leone. It promoted the upgrading of the local mining industry, cultivated local professional talent, and facilitated local industrialization.

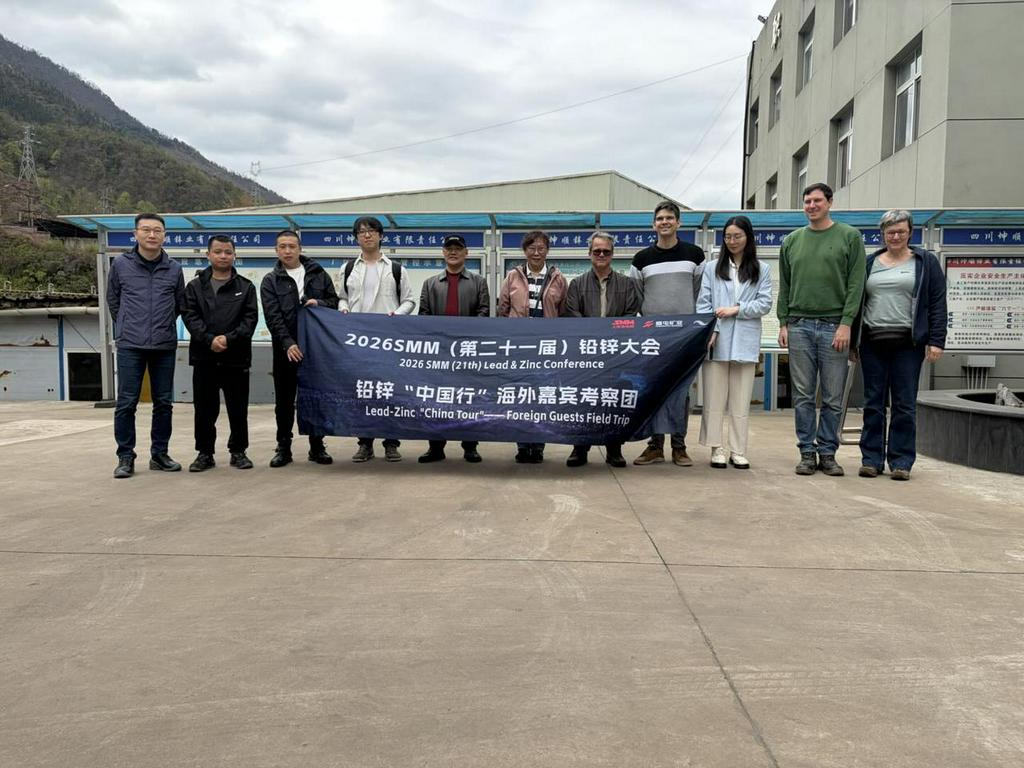

May 11, 2026 13:09  Post-Conference Tour: Connecting Global Lead-Zinc Giants with Key Chinese Players

Post-Conference Tour: Connecting Global Lead-Zinc Giants with Key Chinese PlayersThe 2026 SMM (21st) Lead & Zinc Conference and Industry Expo opened grandly at Howard Johnson Agile Plaza in Chengdu, Sichuan during March 25–27 2026. Organized by SMM, the event brought together global enterprises, professional experts and industry peers from across the entire lead and zinc supply chain. Participants focused on industry hot topics, analyzed market trends and explored development strategies, establishing a highly efficient platform for communication and collaboration to support high-quality growth of the sector. To further strengthen the overseas delegation’s comprehensive understanding of China’s lead and zinc industrial chain and build closer connections between international industry peers and key producers in China, SMM led a high-level overseas delegation on a multi-day industrial tour starting on the afternoon of March 27. The delegation included representatives from global giants, such as Nyrstar, a top European lead and zinc smelting firm, Nexa Resources, a South American giant in lead-zinc mining and smelting, and Befesa, a pioneer in zinc recycling. During the tour, the delegation visited 8 Chinese enterprises. including: COSCO Shipping Sichuan Chengtun Zinc & Germanium Technology Sichuan Kunshun Zinc Industry Yunnan Luoping Zinc & Electricity Hongzhou Hongqian Nonferrous Chemical Yunnan Zhenxing Industrial Group Mengzi Mining & Metallurgy Danxia Smelter of Shenzhen Zhongjin Lingnan Nonfemet The delegation members went deep into production sites, held in-depth discussions and exchanges, and gained a full picture of China’s lead and zinc industry in terms of production operations, technological innovation, capacity scale and market layout, greatly enhancing their insight into and understanding of the entire industrial chain. SMM has systematically compiled detailed information of all enterprises that were visited during this tour, with details below: COSCO Shipping On the afternoon of March 27, the delegation visited COSCO Shipping for an exchange, where they received a warm welcome from the company's leadership. Both sides engaged in discussions on topics such as equipment transportation and technological upgrades. Sichuan COSCO Shipping Logistics Supply Chain Management Co., Ltd. is a wholly-owned subsidiary of COSCO Shipping Logistics Supply Chain Co., Ltd., registered and established in Chengdu, Sichuan Province, with an investment of 30 million yuan. COSCO Shipping Logistics Supply Chain Co., Ltd. is affiliated with China COSCO Shipping Corporation Limited and serves as a core member of the "shipping, ports, and logistics" segment of COSCO Shipping Group, as well as an important component of its global digital supply chain system. The company operates warehouse space exceeding 6 million m², including 19 futures delivery warehouses. China COSCO Shipping Corporation Limited is a globally leading shipping enterprise group, with a combined fleet capacity of 130 million DWT across 1,535 vessels, ranking first in the world. Sichuan COSCO Shipping Logistics Supply Chain Management Co., Ltd. holds business qualifications and an operational scope covering multiple transportation modes including sea, land, air, and rail, providing comprehensive logistics services spanning both international and Chinese markets. Since entering the non-ferrous metals delivery warehouse business in 2016, the company has adhered to the principle of "client-centered and market-oriented," continuously enhancing its service capabilities and achieving steady business growth. Currently, at key logistics periods such as Shanghai Baoshan, Shanghai Yangshan, and Yixing in Jiangsu, the company successfully operates delivery warehouses designated by the Shanghai Futures Exchange for copper, nickel, zinc, and other products. It has become one of the three major non-ferrous metals warehouses of SHFE and was honored with the title of "Top Ten Designated Non-Ferrous Metals Delivery Warehouses" by the Shanghai Futures Exchange for two consecutive years. Sichuan Chengtun Zinc & Germanium Technology Co., Ltd. On March 28, the delegation visited Sichuan Chengtun Zinc & Germanium Technology Co., Ltd. (Shimian City). Both sides engaged in in-depth exchanges on the development of the zinc smelting industry, with a focus on thorough discussions regarding product processing, production techniques, capacity scale, market trends, and the current challenges facing the industry. Sichuan Chengtun Zinc & Germanium Technology Co., Ltd. was established on December 6, 2015, with a registered capital of 1.6 billion yuan. The company has an annual capacity of 300,000 mt of electrolytic zinc, 150,000 mt of sulphuric acid, 400,000 mt of electrolytic zinc waste residue processing, and 40 mt of high-purity germanium dioxide. On January 16, 2019, the company was approved by the China Securities Regulatory Commission and merged into the publicly listed firm Chengtun Mining Group Co., Ltd. The company's main business includes smelting and R&D of zinc-germanium series products, as well as comprehensive recovery of multiple metals. It has formed a complete industry chain from zinc concentrates entering the plant to finished products leaving the plant. Its production lines include zinc calcine, electrolytic zinc, electrolytic zinc waste residue processing, and comprehensive recovery of rare and precious metals. Sichuan Kunshun Zinc Industry Co., Ltd. (Shimian City) On March 28, the delegation headed to Sichuan Kunshun Zinc Industry Co., Ltd. (Shimian City) for a visit and exchange, where they received a warm reception from the enterprise. Both parties held in-depth discussions and exchanges on zinc smelting, covering topics such as production costs, production and market landscape, raw material procurement and processing, industry chain competitive advantages, and distinctive process technologies. Sichuan Kunshun Zinc Industry Co., Ltd. is a specialized and green environmental protection enterprise jointly invested and established by Sichuan Metallurgical Holding Group Co., Ltd. and Shimian Dongshun Zinc Industry Co., Ltd. to implement the national green production philosophy, actively develop the circular economy, and promote the comprehensive utilization of solid waste resources. It integrates solid waste treatment, recycling, and resource regeneration. The company primarily uses high-tech methods to carry out clean utilization and harmless treatment of heavy metal-containing waste generated by industries such as metallurgy and chemicals, eliminating the environmental impact of heavy metal solid waste at the source. The company was established in 2021 and is located in Zhuma Industrial Park, Shimian County, Ya'an City, Sichuan Province, covering an area of 65 mu with a total investment of 180 million yuan. The company has built a 3.5m × 50m Waelz rotary kiln production line, equipped with advanced and well-established low-grade zinc oxide production technology, achieving a resource recovery utilization rate of over 95% and effectively managing waste gas, noise, solid waste, and groundwater risks. It is also equipped with supporting facilities including desulphurization, denitrification, and flue gas defogging towers, as well as a wastewater treatment station, raw material warehouse, raw material pre-washing workshop, water slag processing workshop, biomass semi-gasification furnace, zinc crystallized salt workshop, production safety and environmental protection center, and laboratory for detection and testing. The company holds qualifications for treating hazardous waste categories including HW12, HW17, HW23, HW48, and HW49, with an annual capacity to process 100,000 mt of zinc-containing waste. Its main products include low-grade zinc oxide and zinc crystallized salt. The company has always upheld the green and environmentally friendly development philosophy, adhering to the fundamentals of "being responsible for the environment, for clients, and for employees," guided by technological innovation, and targeting the "reduction, recycling, and detoxification" of solid waste pollution prevention and control. The company is committed to building a modern "solid waste" management and disposal service provider, actively carrying out emergency environmental protection disposal, proactively assuming social service functions, and making positive contributions to promoting the circular economy development in Sichuan and strengthening the ecological civilization construction of lucid waters and lush mountains! Yunnan Luoping Zinc & Electricity Co., Ltd. (Qujing City) On March 30, the delegation visited Yunnan Luoping Zinc & Electricity Co., Ltd. (Qujing City) for exchanges. During the meeting, both sides conducted in-depth discussions on key topics including magnesium removal process optimization, production management organization, and raw material substitution plans, and put forward constructive suggestions on improving the plant environment. Yunnan Luoping Zinc & Electricity Co., Ltd. was established to fully leverage Luoping's local hydropower and lead-zinc mineral resource advantages. In accordance with the "ore, electricity, and smelting integration" development strategy proposed by the Luoping County Party Committee and County Government, and the overall requirements of the Municipal Party Committee and Municipal Government for the reform of industrial enterprises across the city, the company was registered and established at the Yunnan Provincial Administration for Industry and Commerce on December 21, 2000. It was listed on the Shenzhen Stock Exchange A-share market in 2007 and is a state-controlled enterprise under Luoping County. The company's assets are an optimized combination of three components: hydropower, lead-zinc mines, and zinc smelting. In terms of company assets, they are primarily composed of three advantageous resources of Luoping: mineral, hydropower, and zinc smelting. These mainly include six production units: Luoping County Fule Lead-Zinc Mine with an annual processing capacity of 100,000 mt of raw ore, Lazhuang Power Plant with annual power generation of 250 million kWh (installed capacity of 60,000 kW), a zinc smelter with an annual output of 120,000 mt of electrolytic zinc, a zinc powder plant with an annual output of 12,000 mt of ultra-fine zinc powder, a comprehensive utilization plant with an annual processing capacity of 129,500 mt of zinc slag, and a sulphuric acid plant with an annual output of 140,000 mt of sulphuric acid, achieving a total annual industrial output value exceeding 2 billion yuan. The company has six wholly-owned subsidiaries. The company's main businesses include hydropower generation, mining of lead, zinc, and other non-ferrous metals, as well as the production and sales of zinc smelting and its extended products. It is currently the only publicly listed firm in China's zinc smelting industry that integrates mining, power generation, chemical processing, and smelting. Its products include zinc sulphide concentrates, lead concentrates, zinc ingots, industrial sulphuric acid, ultra-fine zinc powder, cadmium, germanium concentrates, silver concentrates, copper concentrates, zinc alloys, industrial and residential electricity, edible oils and fats, among others. Its main product, "Jiulong" brand zinc ingots, is popular in non-ferrous product markets in and outside China thanks to its superior product quality and corporate reputation. Honghe Prefecture Hongqian Non-ferrous Chemical Joint-Stock Co., Ltd. On March 31, the delegation visited Honghe Prefecture Hongqian Non-ferrous Chemical Joint-Stock Co., Ltd. for exchanges. The two sides held in-depth discussions on topics including the economic benefits of smelting by-products, energy utilization efficiency, the current status of enterprise development, and future cooperation intentions. Honghe Prefecture Hongqian Non-ferrous Chemical Joint-Stock Co., Ltd. was established on August 1, 2007, with a registered capital of 50 million yuan. The total investment in project construction was 475.5543 million yuan. The company currently has over 600 employees and covers an area of 443 mu. The plant is located in the Heishenmiaobo Industrial Zone, situated in the central area of the Gejiu-Kaiyuan-Mengzi urban cluster. The company is a new-type joint-stock enterprise centered on crude lead smelting, integrating sulphur dioxide acid production, waste heat power generation, lead electrolysis, and recovery of precious and rare metals such as gold, silver, antimony, and bismuth, with further extension into deep processing of lead-series products including red lead, massicot, electrode plates, and storage batteries. It is a benchmark enterprise among private lead smelters in the city, featuring a relatively large scale, advanced technology, compliance with environmental protection standards, comprehensive utilization of resources, and a complete industry chain. The company pioneered the application of new technologies to upgrade and transform the traditional crude lead smelting model among private enterprises in the city. The company has formulated the working philosophy of "prioritizing environmental protection, ensuring safety, attracting talent, enforcing strict management, and enhancing efficiency," and continues to drive high-quality development. In April 2007, the company commissioned China ENFI Engineering Technology Co., Ltd. to conduct a feasibility study on the lead smelting technological transformation project, and determined a comprehensive industrial facility technological transformation project with a total investment of 490 million yuan and an annual capacity of 60,000 mt of crude lead. On December 21, 2009, the "Demonstration Project of Oxygen-Enriched Bottom-Blowing Lead Smelting Technology with Annual Output of 60,000 mt of Crude Lead" was designated by the Provincial Department of Science and Technology as a 2009 Yunnan Provincial Science and Technology Innovation Project. In 2010, it was further designated as a key industrial project by the provincial, prefectural, and municipal governments. On November 14, 2011, the company obtained ISO9001:2008 quality management system certification. On March 7, 2012, "HSPb99.94PCT" was successfully registered on the London Metal Exchange. In 2019, the company successively passed the safety completion acceptance and environmental impact assessment completion acceptance, fully achieving compliant operations and sustainable development. Yunnan Zhenxing Industrial Group Co., Ltd. On March 31, the delegation headed to Yunnan Zhenxing Industrial Group Co., Ltd. for a visit and exchange. Both parties conducted in-depth discussions on topics including Yunnan Province's mineral resource endowment, smelting industry development trends, corporate business strategies, and technological innovation applications, jointly assessing the current status and prospects of the industry and analyzing the challenges and opportunities ahead. Yunnan Zhenxing Industrial Group Co., Ltd. (hereinafter referred to as "the Group") was founded in 1996 and is located in the Chongposhao New Materials Industrial Park, Shadian Sub-district Office, Gejiu City. The Group currently has 7 subsidiaries, 2 holding companies, and 1 equity-participation company, with approximately 3,000 employees. Its capacity reaches annual output of crude lead (100,000 mt), electrolytic lead (60,000 mt), zinc ingot (20,000 mt), lead-acid battery plates (9 million sets), lead-acid batteries (6 million units), superphosphate (350,000 mt), sulphuric acid (200,000 mt), and monoammonium phosphate (MAP) (60,000 mt). The Group has established five major production sites and five major product brands covering crude lead raw material, lead-zinc smelting, power supply manufacturing, fertilizer and chemical production, and resource recovery. It has formed an internal industrial cycle spanning lead ore mining—lead-zinc smelting—lead-based alloy melting—battery manufacturing—waste battery recycling—precious metals production, making it one of the few private non-ferrous enterprises in China with a complete lead industry chain. Since 2013, the Group has been consecutively recognized as one of the Top 100 Non-Public Enterprises in Yunnan Province. In 2025, it ranked 41st among the "Top 100 Non-Public Enterprises in Yunnan Province" and was selected for the first time into the "Top 20 Private Enterprises in Innovation Capability," ranking 7th. Yunnan Shadian Lead Industry Co., Ltd., a subsidiary controlled by the Group, ranked 71st. The Group has received nearly 100 honors at various levels, including "High-tech Enterprise," "Outstanding Private Technology Enterprise," "Enterprise with Harmonious Labor Relations," "Provincial Model Collective for Ethnic Unity and Progress," and "Key Enterprise for Industrial Development in Honghe Prefecture" in Yunnan Province. The Group's Yunsha brand lead ingot was successfully registered on the London Metal Exchange in 2007 and on the Shanghai Futures Exchange in 2020. In 2021, the Group was rated AAA in enterprise credit rating in the national non-ferrous metals industry. In August 2024, it was designated as a "Qiangyuan Zhuqi" Industry-Finance Service Base by the Shanghai Futures Exchange. Looking ahead, the Group will pursue the philosophy of "seeking survival, pursuing development, and accelerating enterprise transformation and upgrading," adhering to the working approach of "rooting in Honghe, basing in Yunnan, radiating to surrounding regions, and expanding across China." It will thoroughly implement strategies of enterprise management transformation, technology-driven development, talent empowerment, and sustainable development, striving to achieve significant increases in capacity and production of major products by 2035, with gross industrial output value up YoY, and to build itself into a 10 billion green lead-zinc comprehensive recycling technology enterprise. Mengzi Mining and Metallurgy Co., Ltd. On March 31, SMM and the field trip delegation headed to Mengzi Mining and Metallurgy Co., Ltd. for a visit and exchange. Both parties engaged in in-depth discussions on the entire zinc smelting process, covering topics including production technology, raw material supply, product sales, environmental protection governance, and future development plans, aiming to share experience, address industry pain points, and jointly clarify the direction of development. Mengzi Mining and Metallurgy Co., Ltd. was established in 1996. It is a resource-based mining and metallurgy enterprise integrating R&D, exploration, mining, mineral processing, smelting, and trading, with a focus on comprehensive utilization of resources. The company is one of the few comprehensive private enterprises in the non-ferrous metal industry that possesses an entire industry chain and operates independent trading and supply chain business platforms. It is among the top 100 enterprises in Yunnan Province and a key enterprise in Honghe Prefecture. Shenzhen Zhongjin Lingnan Nonfemet Co., Ltd. — Danxia Smelter On April 2, the SMM delegation visited Zhongjin Lingnan's Danxia Smelter for a survey and field trip to the core plant area. In-depth discussions were held on production operations, technological R&D, and raw material procurement, covering key topics such as production capacity, technical cooperation, and raw material procurement strategies. Shenzhen Zhongjin Lingnan Nonfemet Co., Ltd. (hereinafter referred to as "Zhongjin Lingnan") was established in September 1984 and listed on the Shenzhen Stock Exchange in January 1997 (stock code: 000060). It is an internationalized entire industry chain resource company primarily engaged in lead, zinc, and copper mining, mineral processing, and smelting, as well as comprehensive recovery of rare, scattered, and precious metals. It is a publicly listed firm controlled by Guangsheng Holdings Group, a key wholly state-owned enterprise under Guangdong Province. Zhongjin Lingnan's business covers segments including mines, smelting, new materials, and supply chains. It has 23 directly affiliated enterprises, wholly-owned and controlled subsidiaries. Major operating entities include Fankou Lead-Zinc Mine, Shaoguan Smelter, Danxia Smelter, Zhongjin Copper Co., Guangxi Mining Co., Perilya Limited in Australia, Zhongjin Technology Co., and Huajiari Co. The company has an annual output of 300,000 mt of lead and zinc metal content in concentrates, 450,000 mt of smelted lead and zinc products, 450,000 mt of copper cathode, 21,000 mt of aluminum extrusion, 20,000 mt of battery zinc powder, and 5,400 mt of composite metal materials. Among these, its battery zinc powder ranked first in Chinese market share, nickel-metal hydride and nickel-cadmium battery electrode sheets & plates materials ranked first in Chinese market share, and thermal bimetal ranked first in Chinese market share. The 2026 field trip brought together some global lead and zinc industry leaders for an inspiring and highly productive journey across China’s leading smelters and enterprises. The warm welcome, operational excellence, and innovative technologies on display made this event a resounding success — and we extend our deepest gratitude to all the companies and participants who made it happen. Looking ahead – Save the date for 2027: We are excited to announce that the 2027 SMM (22nd) Lead & Zinc Conference and Industry EXPO will take place from March 17–19, 2027 in Kunming, Yunnan, China . This premier event will once again bring together the global lead-zinc community for high-level networking, insight sharing, and industrial exploration. Interactive call – We want to hear from you: As we plan the field trip for the 2027 conference, we’d love your input. Which smelters or companies would you most like to visit for technical exchange and on-site learning? Please share your suggestions in the comments below — your feedback will help shape the 2027 experience. Let us know where the industry should go next!

Apr 7, 2026 14:32- CMOC: 2025 Net Profit up 50.3% YoY, Copper Production at 741,100 mt; Niobium, Cobalt, Molybdenum, and Tungsten Output Exceeded Expectations

According to CMOC’s official WeChat account: On March 27, CMOC released its 2025 annual results report, which showed that the company’s operating revenue reached 206.684 billion yuan, standing firmly above the 200 billion yuan mark for the second consecutive year; net profit attributable to shareholders came in at 20.339 billion yuan, up 50.30% YoY and setting a new record for the fifth consecutive year; net operating cash flow reached the second-highest level in its history at 20.843 billion yuan; and total assets exceeded 200 billion yuan for the first time, reaching 200.932 billion yuan, up 18.03% YoY. In particular, in Q4, the company recorded operating revenue of 61.198 billion yuan, net profit attributable to shareholders of 6.059 billion yuan, and copper production of nearly 200,000 mt, all setting record highs for a single quarter. In 2025, with organisational upgrading as its main focus, the company built a “specialised, internationalised, and younger” team, refined its operations, and, together with rising prices for major products and strong production and sales, pushed its performance to a new peak. Specifically— Operating quality continued to improve. Revenue from the mining segment reached 77.713 billion yuan, accounting for 38% of total operating revenue, with the “mining” share up about 7 percentage points from 2024. Among this, revenue from copper products was 55.096 billion yuan, accounting for 27% of total operating revenue and 71% of mining-segment revenue. Both “copper” share indicators increased by about 7 percentage points YoY. This was attributable to the continued debottlenecking of two world-class copper mines, TFM and KFM, based on their existing six production lines. During the reporting period, the company’s copper production reached 741,100 mt, setting another record high and consolidating its position among the world’s top 10 copper producers. Based on the midpoint of production guidance, the completion rate was 118%, while maintaining double-digit growth of 13.99% YoY. Sales were 730,200 mt, up 5.90% YoY. Together with higher prices, copper revenue increased 31.63% YoY. Production of other products also exceeded expectations: niobium production hit a record high of 10,348 mt, with a completion rate of 103%; phosphate fertiliser production was 1.2135 million mt, with a completion rate of 106%; cobalt production was 117,500 mt, with a completion rate of 107%; molybdenum production was 13,906 mt, with a completion rate of 103%; and tungsten production was 7,114 mt, with a completion rate of 102%. In addition, the company recorded physical trading volume of 4.71 million mt, with a completion rate of 111%; IXM’s gross margin under IFRS was 2.11%, a recent high. The results of “cost reduction and efficiency improvement” became even more evident. Full-year operating costs were 157.229 billion yuan, down 11.56% YoY. In 2025, mining areas worldwide focused on key words such as innovation, technological transformation, and process optimisation, putting the concept of “refined operations” into practice. In Q4, TFM’s overall copper beneficiation and smelting recovery rate, equipment operating rate, and raw ore throughput all exceeded the calendar schedule; KFM established an ore characteristics database and ore blending model, lifting grinding efficiency by more than 30% YoY; at CMOC Brazil’s niobium segment, the recovery rates of two beneficiation plants rose by about 2 percentage points from the previous year, setting record highs; in China, recovery rates at Shangfanggou molybdenum and Sandaozhuang molybdenum and tungsten increased by 3.24 and 2.65, and 3.17 percentage points YoY, respectively, also reaching record highs. Centered on “multiple products, multiple countries, and multiple stages,” the company built a “copper + gold” dual-pole structure in 2025, adding gold resources last year. Together with the greenfield gold mine in Ecuador and four operating gold mines in Brazil, the company will have gold production capacity of 20 mt in South America by 2029. The Ecuador gold mine is expected to start production in 2029, with land acquisition and power supply assurance advancing rapidly; the Brazil gold mines achieved output above target in the first two months, and are expected to produce 6-8 mt of gold this year. Targeting copper production of 800,000-1 million mt in 2028, the company is building Phase II of the KFM project, which is expected to add annual copper capacity of 100,000 mt after coming into operation in 2027; TFM identified resource potential in relevant deposits, and preliminary preparations for Phase III construction are accelerating. In addition, the company completed the issuance of a $1.2 billion one-year zero-coupon convertible bond, broadening financing channels to support the implementation of its strategy. Alongside earnings growth, the company consistently practiced high-standard ESG principles. During the reporting period, ESG governance was further improved and digitalisation advanced; environmental performance led globally: the carbon emission intensity of its copper products was lower than that of 70% of mining companies worldwide, while the shares of renewable energy and water recycling increased further from 2024 to 38% and 89%, respectively; total global economic contribution reached 182.42 billion yuan, and global community investment was 488 million yuan. 2026 is a critical year for the company to fully implement its new development strategy and deepen platform-based operations and refined management. The company will further build a platform-based organisation: with the global supply chain centre as the pioneer, it will enhance synergies and cost competitiveness; relying on the “622” model, supplemented by multinational mine management experience and standardised business processes, it will improve its global control system. Centered on the “copper-gold dual poles,” the company will further transform its resource advantages into capacity and production advantages, while continuing to seek high-quality targets. With the goal of becoming a “globally leading, distinctive world-class mining company,” the company will continue to forge ahead in the mining industry.

Mar 28, 2026 11:05