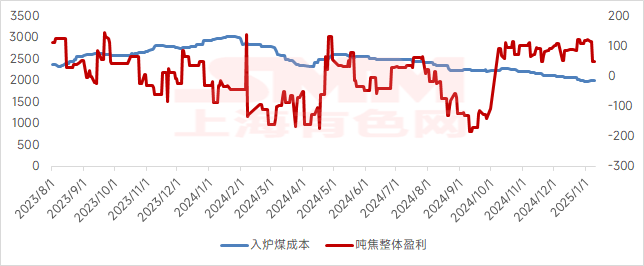

1. According to the SMM survey, coke profit per mt was 118.2 yuan/mt this week, and coke enterprises' profitability weakened.

From a price perspective, coke prices continued to decline, exerting significant negative pressure on coke profit per mt. From a cost perspective, coking coal prices also saw a substantial drop. For instance, the price of low-sulfur primary coking coal fell from 1,580 yuan/mt to 1,450 yuan/mt, a decrease of 130 yuan/mt, while other coal types experienced price drops of 100-200 yuan/mt. This led to a significant reduction in coking costs, providing considerable relief to coke enterprises' losses per mt.

Coke prices are expected to decline further, but coking coal prices are also anticipated to drop. Lower coking costs may help mitigate coke enterprises' losses. Most coke enterprises are likely to maintain profitability next week, staying around the break-even point.

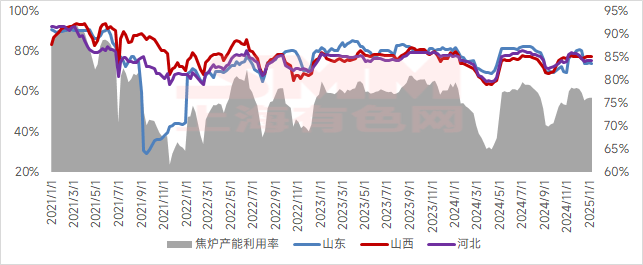

2. According to the SMM survey, the coke oven capacity utilisation rate was 76.1% this week, up 0.0 percentage points WoW. In Shanxi, the coke oven capacity utilisation rate was 77.4%, up 0.1 percentage points WoW.

From a profitability perspective, most coke enterprises maintained relatively good profits, around 100 yuan/mt, which positively impacted production. From an inventory perspective, coke enterprises' inventories showed some buildup as downstream steel mills exhibited low willingness for winter stockpiling, weighing on coke production. From an environmental protection perspective, only Shandong faced strict winter environmental protection inspections, leading to increased production restrictions for some coke enterprises, while other regions were relatively unaffected.

Moving forward, coke enterprises are expected to maintain profitability, with moderate production willingness. Coke supply may increase slightly before the Chinese New Year. However, the finished steel market has cooled, downstream steel mill profits continue to decline, and their outlook remains pessimistic, resulting in low restocking willingness, which may lead to inventory buildup for coke enterprises. In summary, the coke oven capacity utilisation rate of coke enterprises is expected to remain stable next week.

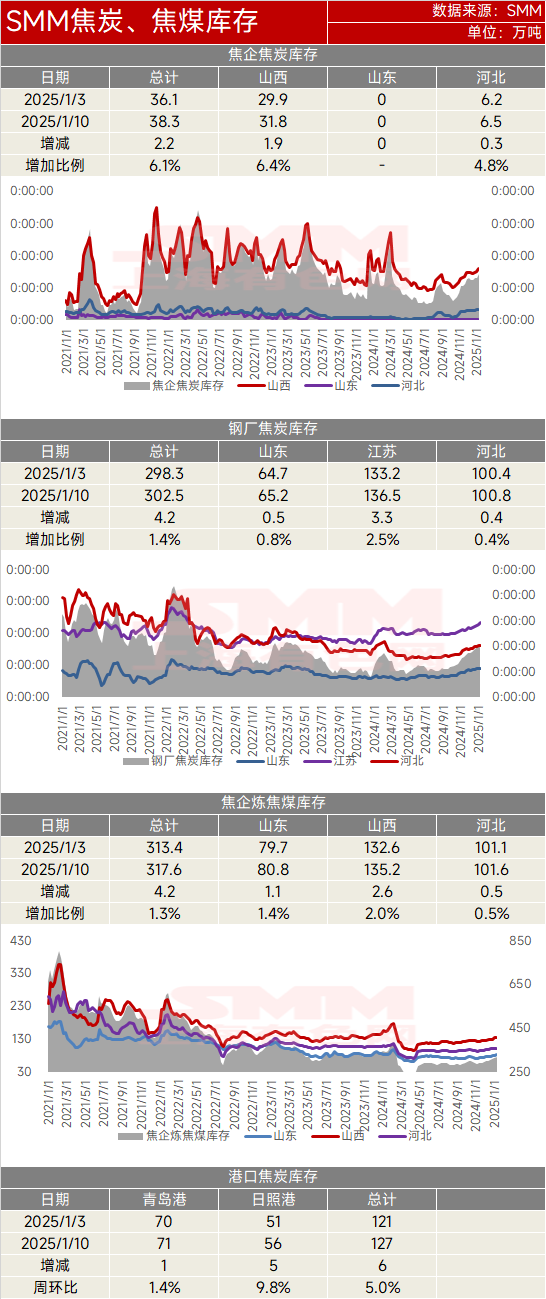

3. This week, coke enterprises' coke inventory stood at 383,000 mt, up 22,000 mt (+6.1%) WoW. Steel mills' coke inventory was 3.025 million mt, up 42,000 mt (+1.4%) WoW. Coke enterprises' coking coal inventory was 3.176 million mt, up 42,000 mt (+1.3%) WoW. Port coke inventory was 1.27 million mt, up 60,000 mt (+5.0%) WoW.

This week, coke enterprises' coke inventory showed an accumulation, while steel mills' coke inventory increased. Coke enterprises' profits remained around 100 yuan/mt, supporting high production enthusiasm and maintaining coke supply at elevated levels. Some steel mills had winter stockpiling needs, and most steel mills' profitability was moderate, boosting their enthusiasm for coke procurement.

Moving forward, coke enterprises' profitability is expected to remain relatively good, sustaining high production enthusiasm. However, as the market enters the Chinese New Year period, trading activity is likely to cool. Coupled with the fact that most downstream steel mills have completed restocking, coke procurement demand is expected to be moderate, with some steel mills even beginning to control coke arrivals. Therefore, coke enterprises are expected to continue inventory buildup next week, while steel mills' coke inventory may fluctuate rangebound.

This week, coal mines continued to prioritize safe production, leading to a decline in coking coal production. Meanwhile, coke enterprises' profits shrank, resulting in cautious procurement. Online auctions for coking coal saw over half of the lots unsold, and most coke enterprises showed moderate willingness to restock coking coal. Therefore, coke enterprises' coking coal inventory is expected to fluctuate rangebound next week.

This week, coke supply remained ample, and coke prices are expected to decline. Speculative enthusiasm among traders has significantly decreased, and port coke inventory is expected to decline next week.